4. Tax Progression

550 likes | 713 Views

4. Tax Progression. 4.1 Measures of Tax Progression According to Tax Schedules 4.2 Aggregate Measures of Tax Progression 4.3 Single Crossing Conditions 4.4 Measurement of Tax Progression with Nonconstant Income Distributions 4.5 Literature.

4. Tax Progression

E N D

Presentation Transcript

4. Tax Progression 4.1 Measures of Tax Progression According to Tax Schedules 4.2 Aggregate Measures of Tax Progression 4.3 Single Crossing Conditions 4.4 Measurement of Tax Progression with Nonconstant Income Distributions 4.5 Literature

4.1 Measures of Tax Progression According to Tax Schedules The primordeal measures of tax progression consider the tax schedule only. The basic relation is the development of the average tax rate if the tax base rises. If the average tax rate rises, too, then the tax schedule is progressive: d[T(y)/y]dy>0. If it decreases, then the tax schedule is degressive, and if it is constant, the tax schedule is proportional. The tax schedules may be further characterized according to the second derivative. If the first derivative is positive [negative] and the second derivative of the average tax rate is negative (positive; zero), the tax schedule is called delayed progressive (accelerated; linear progressive) [accelerated degressive (delayed; linear degressive)]. T/y T/y y y

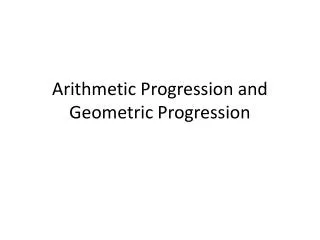

Notice that no tax schedule must be accelerated or linear progressive throughout because it would eventually exceed the tax base. Similarly, no tax schedule must be accelerated or linear degressive throughout because taxation would eventually result in subsidies (negative taxes). Starting from the average tax rate, other measure of tax progression can easily be devised, e.g., the difference between marginal and average tax rate, the revenue elasticity ε[ratio of the relative change in tax and the relative change in the tax base], and the residual income elasticity η[ratio of the relative change in net income and the relative change in the tax base]. When the relative change in tax exceeds the relative change in the tax base, then the tax schedule is progressive: ε>1. When the relative change in net income falls short of the relative change of the tax base, then the tax schedule is progressive: 0<η<1. The extension to degressive tax schedules is immediate. The next slide shows these measures in formal terms. As they seem to convey the same message, we may ask why this multitude of measures is really necessary. This is actually warranted as long as we just want to categorize tax schedules. When it comes to determining whether one tax schedule is more or less progressive (degressive) than another one, these measures may convey different judgments. The second slide shows the situation of the German income tax reform 1986 to 1990, which shows indeed that ε and ηdisagree on some intervals as to which tax schedule is more progressive.

The left-hand diagram displays the revenue elasticity of the German tax schedules 1986 and 1990 [Seidl and Kaletha (1987)]. The 1986 schedule is more progressive in the interval from 22,397 to 69,678 Deutschmarks. The right-hand side displays the residual income elasticity of the German tax schedules 1986 and 1990. The 1986 schedule is more progressive in the interval from 20,535 to 97,289 Deutschmarks. This interval is greater than the interval of being more progressive according to revenue elasticity.

The measures of tax progression according to tax schedules suffer from a big disadvantage, viz. they neglect the income distribution in the respective economy. Suppose an income tax schedule reaches marginal tax rates (say, 60%) for incomes beyond € 1 million, but hardly anybody has an income beyond € 100,000. For € 100,000 the marginal tax rate is, say 25%. Then this tax schedule can be perceived as less progressive than another one which reaches a marginal tax rate of 35% at an income of € 100,000 and does not increase any further for higher incomes. Hence, we have to look for measures of tax progression which take the income distribution into account.

4.2 Aggregate Measures of Tax Progression Global measures of tax progression associate a real number with each income tax schedule and the income distribution appertaining to it. Global measures of tax progression which rely on the taxes and their distribution are denoted by π, measures which rely on post-tax incomes and their distributions are denoted by ρ. There are two groups of global measures of tax progression: the first group is based on concentration indices, the second group is based on the concept of the equally distributed equivalent income [Atkinson-type measures]. Although work has been done on the second type of measures [Blackorby and Donaldson (1984a,b), Kiefer (1985)], we shall, for practical reasons, concentrate on the first group of measures of tax progression.

Taxation Economics: Short Account of Eigth Lecture • We discussed evasion- and corruption-proof tax regimes: the maximum penalties come up to the whole income earned. • Proposition 2 showed necessary and sufficient conditions for revenue maximizing and evasion-proof tax schedules. • Proposition 3 considers also corruption-proofness: the expected gain in commission should be smaller than the expected penalty for the inspector for income over-reporting. • If no commission is paid, these requirements are satified if no commission is paid [Proposition 4]. • If we want to use a progressive tax schedule, then a two-tier tax schedule is required [Proposition 5]. • Then we started dealing with the measurement of tax progression and considered local measures of tax progression. Moreover, we considered measurement of comparative tax progression for local measures. • Finally we started consideration of global measures of tax progression.

Before proceeding further we present a graphical illustration: 1 1 1 1

Before proceeding further we present a graphical illustration: 1 1 1 1

Let us now turn to global measures of tax progression. They were first proposed by Dalton (1922/1954) and Musgrave and Thin (1948). Dalton proposed the mean deviation of average tax rates as a global measure of tax progression:

Alas, all global measures of tax progression suffer from the disadvantage that they aggregate too much. One can easily conceive of tax schedules which are degressive on some income interval and turn out to be more progressive than tax schedules which are progressive throughout, because of overcompensating effects on some other income interval. This does not mean that we should neglect the income distribution, but it means that we have to consider dominance relationships. This will be done in the next two sections.

Suppose the net income schedules (and, hence, the tax schedules) have more than one crossing, say, two crossings: y-T2 y-T1 0 y′ y* In such cases there exist income distributions of pre-tax incomes such that the tax schedules T1 and T2 raise equal revenue on the part of the income distribution confined to [0,y′] and raise equal revenue on the part of the income distribution confined to [y′,y*]. But then T1 is more progressive than T2 for the former part of the income distribution and less progressive for the latter part. [For a more thorough investigation see Dardanoni and Lambert (1988).]

Hemming and Keen (1983) also show that the single-crossing conditions for greater tax progression are equivalent to the elasticity criteria of Jakobsson (1976) and Kakwani (1977). We will deal with these criteria in the next section. Hemming and Keen (1983) also tried to generalize their analysis for income tax schedules with generate different revenues. They normalized the tax schedules by their respective s, so that the tax revenues of both tax schedules are normalized to 1. The single crossing conditions present a major advance on the other measures of tax progression discussed so far. However, their problem lies in the assumption that the income distributions remain the same for the tax schedules to be compared. However, different tax schedules may well exert allocation effects, may influence subjects’ behavior etc., that is, give rise to different pre-tax income distributions, which invalidates the applicability of single crossing conditions. Moreover, intertemporal and international comparisons of tax progression are ruled out because such comparisons typically involve different income distributions. We shall address such cases in the next section.

4.4 Measurement of Tax Progression with Nonconstant Income Distributions The single crossing conditions as well as the (equivalent) elasticity criteria developed by Jakobsson (1976) and Kakwani (1977) apply only for comparisons of tax schedules on condition that the associated income distributions are the same. However, the question whether the American income tax, given the American income distribution is more or less progressive than the German income tax given the German income distribution is a provoking problem which cannot be answered by these criteria. In this section we shall develop instruments to deal with this problem.

Before proceeding further we present a graphical illustration: 1 1 1 1

In addition, we may not be interested how tax progression compares for the same levels of income, but how it compares for the same fraction q of the lowest income earners or for the same fraction p of compound pre-tax income. The next two theorems provide the respective sufficient conditions which avoid the requirement of the same support of the income distributions.

Exam Taxation Economics • Date of exam: December 9th, 2:15 p.m., SR 506 • Time: 1 hour + 20 minutes for reading problems • Registration: Oct. 26th to Nov. 22nd klausuronline • Evaluation: 100 points maximum, at least 40 points to pass [grade transform in exam office] • Repetition: only for students who did not pass the first time and got at least 20 points; problems will consider that there was more time for learning • Date of repetition: February 12th, 12:00-2:00 p.m., SR 506 [Registration: Dec. 30th to Jan. 27th klausuronline] • Erasmus students who need more than 6 ECTS?

Taxation Economics: Short Account of Ninth Lecture • First moment distribution functions • Expression of first moment distribution functions as functions of q by means of the transformation and its graphical illustration • Gini and concentration coefficients • Construction of concentration curves by the transformation plugged into the first moment distribution function and graphical illustration • Global measures of tax progression in terms of taxes and in terms of net incomes as well as the generalization by Pfähler • Single crossing conditions • Measurement of tax progression in case of nonconstant income distributions • Theorem 1: influence of the income distributions on the measurement of tax progression; Corollaries 1A and 1B for special cases

represents the relative increase in tax revenue collected from the fraction q of the lowest income earners when q is slightly increased. Note that for a given q it is evaluated for different income distributions at different income values. This expression is nothing but a complicated elasticity involving the tax schedule and the income distribution. It transforms the q-values into y-values. Analogously for the post-tax incomes.

Figure 1: Construction of a relative concentration curve from Lorenz curves for taxes 1 1 q q 1 1 1 1

The interpretation of these expressions is not straightforward. We se that we have an elasticity representing the relative increase in tax revenue collected from the fraction p of the aggregate income of the lowest income earners when p is slightly increased. Whenever the income distributions are identical, Theorems 1-3 coincide.

Let us again present a graphical illustration for this transformation: 1 1 1 1 1 1

These instruments allow us to answer questions like that whether the income tax schedule jointly with the American income distribution is more or less progressive than the German income tax schedule given the German income distribution. However, the trick to answer this question is that the hub of making such comparisons is to focus either on the fraction of the poorest income earners q, or on the fraction of the lowest aggregate income p. These are the focal points of comparisons of tax progression among different countries or among different time periods. There is also another way to make comparisons of tax progression, namely by way of differences of concentration curves. A detailed analysis in continuous terms can be gathered from Seidl (1994). We shall now turn to preliminary empirical computations using LIS data for 13 countries (out of 15 for which data on gross and net incomes were available). Unfortunately, the data are not separated into taxes and social security contributions. Hence, the more appropriate term would be impost progression rather than tax progression, but we used the term tax progression because this terminology was also used by the Luxembourg Income Study Project. We start with formulating the discrete counterparts of the respective concentration curves [different notation] and continue with definitions of higher progression in discrete terms, where we used differences of concentration curves rather than using them in their shapes as relative concentration curves.

for for

Are these conditions also necessary conditions? It depends. If these conditions should hold for all possible income distributions for two given tax schedules which are to be compared, then they are sufficient and necessary conditions because if they are violated, then one can always find an income distribution applying to both tax schedules such that the associated relative concentration curve crosses the diagonal of the unit square. This method was chosen in related contexts by Jakobsson (1976) and Hemming and Keen (1983). Both approaches can be shown to be equivalent. Hence, only the tax schedule matters, for instance, single crossing of tax schedules. However, these conditions fail if they should hold for all income-distribution-cum-tax-schedules because for any pair of income distributions one can find a pair of tax schedules, e.g., multiple-crossing tax schedules, such that the associated relative concentration curve crosses the diagonal.

Summary statistic of 78 international and 21 intertemporal comparisons of tax progression for six concepts of tax progression