Download

1 / 15

150 likes | 265 Views

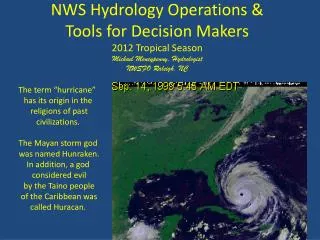

The Challenges of the Hungarian Tax Authority in View of its Middle Term Strategy and its Responses to those. . János Szikora. Washington D.C. 9 June 2009. SERVICE PROVIDING TAX AUTHORITY. Renewal of our Strategy. Formulation of strategic management

E N D

The Challenges of the Hungarian Tax Authority in View of its Middle Term Strategy and its Responses to those. János Szikora Washington D.C. 9 June 2009. SERVICE PROVIDING TAX AUTHORITY

Renewal of our Strategy • Formulation of strategic management • Under the supervision of the Project Council • Bottom to top building (wide scale and public) • Involvement of external experts (universities, IMF) • Not only a document, but a vivid, operational process! SERVICE PROVIDING TAX AUTHORITY

Forming the Base of our Strategy • Evaluation of professional publications, recommendations • Studying internationally accepted methods (partner tax authorities, OECD, EU Fiscal Blueprints, IMF) • SWOT and PEST analysis Through this analysis we got a picture of our values, external environment, opportunities and threats as well as of our strengths and weaknesses. SERVICE PROVIDING TAX AUTHORITY

Milestones in Creating APEH Strategy for 2008-2012. 3 January 2008 Kickoff Vision, mission, values, timescale, SWOT analysis, PEST analysis, IMF advisors, wide scale internal brainstorming 13 May 2008 Project Council accepts the first version of the strategy Proposal requests (sub-objectives, indicators), ADOK (internal brainstorming), IMF, Multi round opinions 1 October 2008 Reducing strategic objectives from 4 to 3 Multi round opinions, Project Council decisions, IMF 27 November 2008 TheProject Council approves the strategy Printed publication, countrywide and local press conferences, internet publication (in Hungarian and English) 16 December 2008. Launching the Strategy SERVICE PROVIDING TAX AUTHORITY

Mission • Vision: • „ To become an organisation operating on the standards of the leading tax administrations of the world… „ • Our Values: • Legality • Professionalism • Probity • Fairness and Equity • Efficiency • Effectiveness • Integrity • Transparency • Reliability Strategy 2008 – 2012. SERVICE PROVIDING TAX AUTHORITY

Strategic Objectives and Related Tasks 1. STRATEGIC OBJECTIVE:Improve voluntary compliance of taxpayers by developing tax services promoting compliance, by making taxation simpler and more comfortable and by raising tax awareness. 2. STRATEGIC OBJECTIVE:Use consequently all lawful and fair administrative means with those taxpayers, who fail to meet their liabilities and thus cutting grounds for those who are willing to take similar risks. 3. STRATEGIC OBJECTIVE:In order to reach the professional objectives of the organisation we need effective organisational solutions, committed and impeccable colleagues with the widest professional competence, and the most up to date technical and financial conditions. SERVICEPROVIDING TAX AUTHORITY

1. Strategic objective 1.1.: SUB-OBJECTIVE : Help voluntary tax compliance. • Segmented information services by types of different taxpayers(personal tax diary from 1 September 2008) • Development of Customer Services from 2008 (payment of taxes by bank cards) • Taxpayer’s and the tax authority’s rights and liabilities, formulated and published in an apprehensible manner(in progress) 1.2. SUB-OBJECTIVE: Significantly reduce administrative burden. • Modernization of tax returns (instead of 59 types of returns in 2007 only 23 returns and 10 other data submission in 2008). • Electronic administration (from 1 July 2009 under the law) • Simplified tax return (operational since 2009) SERVICE PROVIDING TAX AUTHORITY

1. Strategic objective 1.3. SUB-OBJECTIVE: Contribute to the increasing of tax awareness. • Rang-Adó quiz series among secondary schools (final transmitted by public TV) • Tax Bogy • Advertisement campaigns, participation in various public events • Measuring taxpayer satisfaction SERVICE PROVIDING TAX AUTHORITY

2. Strategic objective • 2.1. SUB-OBJECTIVE: Combat tax avoidance more effectively. • Preventive audits under the law (in 2008 at 27 % of starting businesses) • VAT cheaters • Invoicing round schemes (including multilateral audits as well) • Transfer pricing audits SERVICE PROVIDING TAX AUTHORITY

2. Strategic objective 2.2. SUB-OBJECTIVE : Strengthen risk management activities. (in progress) 2.3. SUB-OBJECTIVE : Renewal of audit methods. • audit teams (in progress) • Manual on Imposing Fines( from January 2009. accessible on our website) • Audit Manual (in progress) 2.4. SUB-OBJECTIVE: Improve our enforcement activity • E-auctions for real estates from 2009 • new project SERVICE PROVIDING TAX AUTHORITY

3. Strategic objective 3.1. SUB-OBJECTIVE: Modernisation of the organisation and of the administration processes. • Project Bureau established • Knowledge base created(Call Center uses, accessible for other colleagues) 3.2. SUB-OBJECTIVE: Effective human resource management • Started familiarization with competence values of job types • Intranet website operational • Young Tax Administration Workers Association (FADE) established SERVICE PROVIDING TAX AUTHORITY

3. Strategic objective 3.3. SUB-OBJECTIVE: Development of the IT systems. • Smooth transformation to Oracle platform, introduction of a new document registration system from June 2009 • 3.4. SUB-OBJECTIVE:Investment Necessary for the Implementation of the Strategy. • Widening bandwidth at 86 customer service offices (in progress) • 3.5. SUB-OBJECTIVE: Introduction of process (operative) controlling approach in the field of finance and logistics. • The economic crises delays the start of resource consuming tasks. • 3.6. SUB-OBJECTIVE: Ongoing extension of the organisation’s international relations

Tasks related to the introduction of the strategy • Interlink the strategy, the yearly business plan and the evaluation system (started in 2009) • Continuous evaluation of the implementation status, definition of new tasks • Operation of the related Transformation Plan SERVICE PROVIDING TAX AUTHORITY

Implementation of the Strategy 1 2 3 4 5 6 7 8 Murphy Model Tool Development Murphy Model Calibration Project Identification STABILITY and FLEXIBILITY Transformation Plan: Objectives (3), sub-objectives (13) and tasks deriving from them (117) Result indicators Timeframe of implementation Responsible organisational units Acceptance of the strategy by colleagues Project Definition Project Delivery Definition Project “Murphy” Remediation Final Murphy Model Analysis Build & Confirm Recommended Portfolio Transfer Selected Projects to PM Process SERVICE PROVIDING TAX AUTHORITY

Thank you for your attention! SERVICE PROVIDING TAX AUTHORITY