Download

1 / 29

290 likes | 471 Views

Economic and Market Outlook. October 20, 2011. Presented by: Paul Teten, CFA Senior Director, Fixed Income Portfolio Management Capital One Asset Management, LLC. U.S. rate outlook dependent on economic growth trajectory AND

E N D

Economic and Market Outlook October 20, 2011 Presented by: Paul Teten, CFA Senior Director, Fixed Income Portfolio Management Capital One Asset Management, LLC

U.S. rate outlook dependent on economic growth trajectory AND Resolution of several uncertainties suppressing growth and risk-taking: Is the deleveraging cycle over? Is the banking system functioning again? When will consumers begin to spend more normally? When will the housing sector recover? Is there a fiscal policy train wreck coming? Where are the drivers of global growth? Will Greece default and if so does that mean there will be a Lehman-style financial system melt-down in Europe? U.S. Interest Rate Outlook

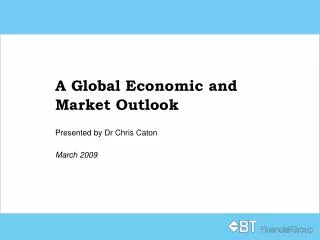

Banks and governments in these five shaky economies owe each other many billions of euros – converted here to dollars – and have even larger debts to Britain, France and Germany. Arrow widths are proportional to debt amounts. Italy owes France $511 billion, or nearly 20 percent of the French gross domestic product. With unemployment at 20 percent, Spain has an economy among the weakest in Europe. Nearly one-third of Portugal’s debt is held by Spain, and both countries’ credit ratings have been dropping. Source: New York Times, 5/1/10

Will U.S. Economic Growth Accelerate in 2012? Signals indicating YES: • Banking system functioning, credit and money supply growing Signals indicating MAYBE: • Consumer spending COULD accelerate IF confidence improves and the unemployment rate declines • China may resume a stronger growth track Signals indicating NO: • The housing sector is likely to remain stagnant for 2-3 years • Consumers likely to remain cautious and continue deleveraging • Business investment and hiring likely to remain risk averse due to worrisome fiscal and regulatory uncertainties • Global growth is slowing • Greek default inevitable, contagion risk high, Europe sliding into recession

What Can The Fed Do? The Fed is about out of weapons to fight sluggish growth • The Fed’s dual mandate presents contradictory challenges • QE1 and QE2 were successful in preventing deflation • But neither has been successful in igniting strong economic growth • The linkage between low interest rates and economic growth has been broken by deleveraging and housing dysfunction The Fed is aggressively manipulating long-term interest rates to historically low levels… what are the costs? • Savers are penalized to the benefit of debtors • A large cross-section of consumers are dependent on savings income • Corporate profits are being bled by growing unfunded pension liabilities, accelerating the trend to 401Ks and transfer of retirement risk to consumers • Asset bubble risks are high