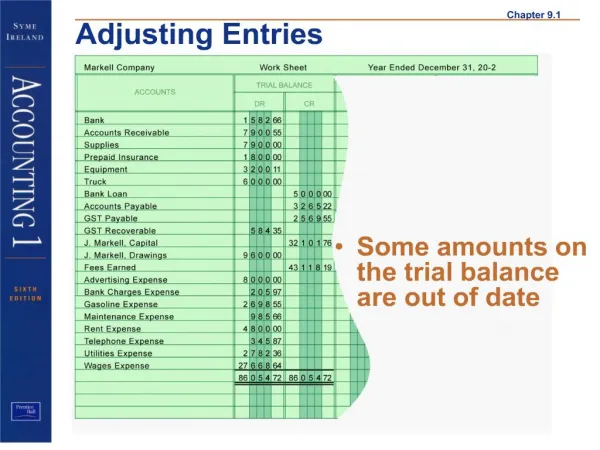

The trial balance

This guide covers the concept of trial balances, a crucial step in ensuring that every credit entry has a matching debit. The process involves recording all debit entries in one column and credit entries in another, ensuring both columns balance. If they don't, there may be errors in the T-accounts. This resource also includes a trial balance preparation exercise using your initial accounts and answers to review questions. Mastering these principles is vital for accurate financial reporting and understanding the relationships between different account types.

The trial balance

E N D

Presentation Transcript

The trial balance PART 1

Trial Balance In order to check that there is a matching debit for every credit entry, we do a trial balance. We enter all the debits in one column and all the credits in another column. The total in each column should balance. If it does not, then there is an error somewhere in your t-accounts (you may have missed a credit or debit entry)

Trial Balance Using your starter (Balancing-off accounts), prepare a trial balance

Review questions worksheet PEARLS Purchase Expenses Assets Revenue Liabilities Sales This may help you to remember which accounts to debit or credit when the increase in value DEBIT CREDIT