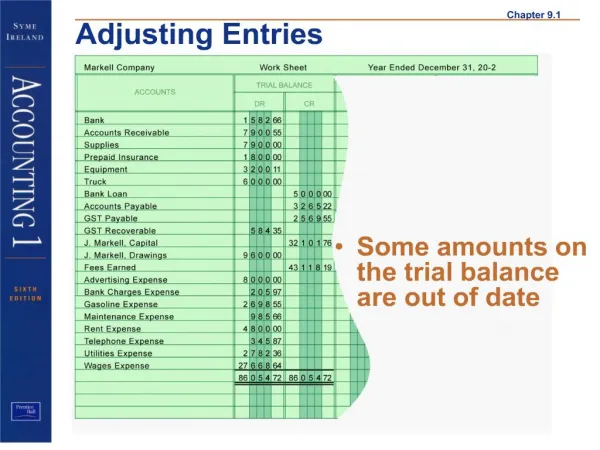

Trial Balance

Trial Balance. Accounting I. Key Vocabulary. Proving the Ledger Trial Balance Transposition Error Slide Error Correcting Entry. Definitions:. Adding all the debit balances and adding all the credit balances and then comparing the two totals to see whether they are equal.

Trial Balance

E N D

Presentation Transcript

Trial Balance Accounting I

Key Vocabulary • Proving the Ledger • Trial Balance • Transposition Error • Slide Error • Correcting Entry

Definitions: • Adding all the debit balances and adding all the credit balances and then comparing the two totals to see whether they are equal. • A list of all the account names and the current balances. • When two digits within an amount are accidentally reversed. This error is divisible by 9. • When the decimal place is moved ( or add or subtract a zero) • An entry made to correct an error in a journal entry discovered AFTER posting.

The Accounting Cycle Taken from Glencoe Accounting, 5th ed.,2004

The Trial Balance • The purpose of the trial balance is to prove that the general ledger is in balance. • To prepare a trial balance: • List ALL accounts, even those with zero balances, in the order they appear in the ledger. • Copy all debit balances to the debit column and credit balances to the credit column. • Total each column and compare balances.

Trial Balance Debit Balances Credit Balances Compare Balances

Finding Errors • If the first addition of the columns gives unequal results, add them again, an addition error may have occurred. • If the balances are still uneven, check if the difference is divisible by 9. If so, a transposition error has occurred. • If the difference is an even amount with a “zero”, a slide error has occurred.

More on Errors 4. Most errors are either computational or incorrect postings. 5. Computational errors are easier to find, simply re-add.Incorrect postings take longer to find because it involves looking through all of the ledger accounts. 6. Occasionally a debit will be recorded as a credit and vice versa. These sometimes take a while to find.

Correcting Entries Anyone who works in accounting understands the saying “ To err is human…” When mistakes are made in accounting, however, one rule applies: NEVER erase an error. Three types of errors: • Error in journal entry that is not posted. • Error in posting to the ledger when the journal entry is correct. • Error in journal entry that is posted.

Example • If a utility bill was accidentally posted to the maintenance expense account, a new journal entry would have to be made to undo and correct the entry on the date the error was found, using the same source document:

Example • From the journal entry, the corrected posting to the ledger accounts would look like this, with the words “correcting entry” in the description box:

The Trial Balance • After errors have been found and corrected, run trial balance again. Debits and credits should be equal, if not, go through error finding process again.

References • Guerrieri, Haber, Hoyt, & Turner. (2004) Glencoe Accounting: Real-World Applications & Connections. (5th ed.) Woodland Hills, CA: Glencoe McGraw Hill.