Download

1 / 41

840 likes | 2.04k Views

Target Costing, Theory of Constraints, and Life Cycle Costing. 8. Tujuan Pembelajaran. Setelah mempelajari materi kuliah diharapkan anda mampu untuk:. Target Costing, Theory of Constraints, and Life Cycle Costing. Menjelaskan peggunaan Target Costing untuk tujuan stratejik

E N D

Target Costing, Theory of Constraints, and Life Cycle Costing 8

Tujuan Pembelajaran Setelah mempelajari materi kuliah diharapkan anda mampu untuk: Target Costing, Theory of Constraints, and Life Cycle Costing • Menjelaskan peggunaan Target Costing untuk tujuan stratejik • Menjelaskan aplikasi TOC untuk tujuan stratejik. • Menjelaskan aplikasi life cycle costing untuk tujuan stratejik. • Menjelaskan tujuan sales life cycle.

The Cost Life Cycle (Siklus Biaya) The Cost Life Cycle: Merupakan urutan aktivitas dalam perusahaan mulai dari R & D sampai Customer service. The Sales Life Cycle: Merupakan urutan atau fase hidup produk atau jasa mulai intro sampai decline

The Cost Life Cycle (Siklus Biaya) Slide 5-2 Target Costing, Theory of Constraints, and Life Cycle Costing R & D

The Cost Life Cycle (Siklus Biaya) Slide 5-2 Target Costing, Theory of Constraints, and Life Cycle Costing R & D Design

The Cost Life Cycle (Siklus Biaya) Slide 5-2 Target Costing, Theory of Constraints, and Life Cycle Costing Produc-tion R & D Design

The Cost Life Cycle (Siklus Biaya) Slide 5-2 Target Costing, Theory of Constraints, and Life Cycle Costing Mkt. & Distri- bution Produc-tion R & D Design

The Cost Life Cycle (Siklus Biaya) Slide 5-2 Target Costing, Theory of Constraints, and Life Cycle Costing Mkt. & Distri- bution Custo- mer Service Produc-tion R & D Design

The Cost Life Cycle (Siklus Biaya) Slide 5-2 Target Costing, Theory of Constraints, and Life Cycle Costing Mkt. & Distri- bution Custo- mer Service Produc-tion R & D Design Upstream Activities (Aktivitas Hulu) Downstream Activities Aktivitas Hilir

The Cost Life Cycle (Siklus Biaya) • Metode yang membantu dalam analisis cost life cycle adalah target costing, theory of constraint dan life cycle costing.

The Sales Life of a Product (Siklus Product) Slide 5-3 Target Costing, Theory of Constraints, and Life Cycle Costing Introduction

The Sales Life of a Product (Siklus Product) Slide 5-3 Target Costing, Theory of Constraints, and Life Cycle Costing Growth Introduction

The Sales Life of a Product (Siklus Product) Slide 5-3 Target Costing, Theory of Constraints, and Life Cycle Costing Growth Maturity Introduction

The Sales Life of a Product (Siklus Product) Slide 5-3 Target Costing, Theory of Constraints, and Life Cycle Costing Growth Maturity Decline Introduction

The Cost Life Cycle (Siklus Biaya) Slide 5-4 Target Costing, Theory of Constraints, and Life Cycle Costing Mkt. & Distri- bution Custo- mer Service Produc-tion R & D Design TARGET COSTING

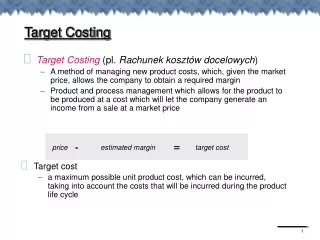

TARGET COSTING • Target costing digunakan untuk mengelola biaya, terutama dalam aktivitas desain. • Dalam Target costing perusahaan menentukan biaya yang harus dikeluarkan berdasar harga pasar kompetitif, dengan demikian maka perusahaan dapat memperoleh laba yang diharapkan.

Mengurangi biaya pada tingkat Target Cost Slide 5-5 Target Costing, Theory of Constraints, and Life Cycle Costing • Integrasi tekhnologi manufaktur baru, menggunakan teknik manajemen biaya maju, dan mengamati produktivitas yang lebih tinggi melalui improved hubungan organisasi dan pekerja. • Redesigning produk atau jasa.

Implementasi Target Costing Slide 5-6 Target Costing, Theory of Constraints, and Life Cycle Costing • Tentukan harga pasar. • Tentukan laba yang diinginkan. • Hitung target cost pada harga pasar dikurang laba yang diharapkan. • Gunakan rekayasa nilai untuk mengidentifikasi cara mengurangi biaya produk. • Gunakan Kaizen costing dan pengendalian operasional untuk mengurangi biaya produk.

Implementasi Target Costing • Rekayasa Nilai (value engeneering) digunakan dalam target costing untuk menurunkan biaya produk dengan cara menganalisis “trade off” antara : • 1. jenis dan level yang berbeda dalam fungsionalitas produk. • 2. Biaya produk total.

The Cost Life Cycle Slide 5-7 Target Costing, Theory of Constraints, and Life Cycle Costing Mkt. & Distri- bution Custo- mer Service Produc-tion R & D Design The Theory of Constraints

The Theory of Constraints • TOC memfokuskan perhatian manajer pada kendala atau pemborosan yang memperlambat proses produksi. • TOC mengarahakan perhatian manajer pada bagaimana kecepatan bahan baku dan komponen yang dibeli utk diproses menjadi produk akhir dan diserahkan kepada pelanggan.

The Theory of Constraints Slide 5-8 Target Costing, Theory of Constraints, and Life Cycle Costing • Identifikasi kendala pengikat (binding and non-binding constraints). • Menentukan pemanfaatan paling efisien untuk setiap kendala pengikat (binding constraint). • Mengelola aliran sepanjang binding constraint. • Menambah kapasitas pd kendala yang mengikat. • Desain ulang (Redesign) proses manufaktur kearah fleksibilitas dan throuput yang cepat.

Memaxiumkan aliran dalam kendala pengikat (Binding Constraint) Slide 5-9 Target Costing, Theory of Constraints, and Life Cycle Costing • Menyederhanakan bottleneck dalam operasi: *sederhanakan desain produk *sederhanakan proses manufaktur • Cari cacat kualitas dalam bahan baku yang menyebabkan keterlambatan (slowing things down). • Turunkan waktu set-up . • Turunkan kelambatan lainnya yang terkait dengan unscheduled dan non-value-added activities, seperti inspections, kerusakan mesin (machine break-downs). • Sederhanakan kendala pengikat dengan cara mengubah semua aktivitas dari kendala yang tidak mengurangi fungsi operasi.

The Drum-Buffer-Rope System • DBR System merupakan suatu sistem untuk menyeimbangkan aliran produksi melalui kendala yang mengikat sehingga mengurangi jumlah persediaan pada kendala dan meningkatkan produktivitas secara keseluruhan.

The Drum-Buffer-Rope System Slide 5-10 Target Costing, Theory of Constraints, and Life Cycle Costing Raw Materials Process One Process Two Process Three Rope Small amount of Work in Process Inventory Buffer Drum Process Four Process Five Finished Goods Lihat halaman blocher

Perbandingan Costing Methods Slide 5-11 Tujuan Utama TOCABC Fokus Jk Pendek; analisis through-put berdasar bahan dan biaya terkait. Fokus Kh Panjang; analisis semua biaya produk; materials, labor dan overhead Lihat hal 162 blocher

Perbandingan Costing Methods Slide 5-11 Batasan dan Kapasitas Resource TOCABC Termasuk; Fokus Pemilik TOC Tudak eksplisit Lihat hal 182 blocher

Perbandingan Costing Methods Slide 5-11 Cost Drivers TOCABC Utilisasi tdk langsung cost drivers. Utk mengembangkanpemahaman cost drivers pd level unit, batch, product dan facility Lihat hal blocher

Perbandingan Costing Methods Slide 5-11 Penggunaan Utama TOCABC Optimasi arus produksi dan product mix jk pendek Strategic pricing dan profit planning Lihat hal blocher

The Cost Life Cycle Slide 5-12 Mkt. & Distri- bution Custo- mer Service Produc-tion R & D Design Upstream Costs Downstream Costs LIFE CYCLE COSTING

The Cost Life Cycle Slide 5-13 Target Costing, Theory of Constraints, and Life Cycle Costing Upstream Costs: Research and develop- ment Design: prototyping, testing, concurrent engineering, quality development

The Cost Life Cycle Slide 5-13 Target Costing, Theory of Constraints, and Life Cycle Costing Upstream Costs: Research and develop- ment Design: prototyping, testing, concurrent engineering, quality development Manufacturing Costs: Purchasing Direct manufacturing costs Indirect manufac- turing costs

The Cost Life Cycle Slide 5-13 Target Costing, Theory of Constraints, and Life Cycle Costing Upstream Costs: Research and develop- ment Design: prototyping, testing, concurrent engineering, quality development Manufacturing Costs: Purchasing Direct manufacturing costs Indirect manufac- turing costs Downstream Costs: Marketing and distribution-- packaging, shipping, samples. promotion, advertising Service and warranty--recalls, service, product liability, customer support

Critical Success Factors pada Tahap Design Slide 5-14 • Menurunkan waktu ke pasar • Menurunkan biaya servis yang diekspektasi • Improve manufaktur yang mudah • Rencanakan Proses dan desain

Tahap Desain • 4 metode desain: • 1. Basic engineering, desainer bekerja terpisah dengan bagian lain dalam manufaktur • 2. Prototyping, pengembangan model dengan melakukan percobaan oleh tekhnisi dan pelanggan. • 3. Templating, desain produk yang ada di tambah atau dikurangi supaya sesuai dengan spesifikasi yg diharapkan • 4. Concurrent engineering, pengintegrasian dalam desain produk dengan pemasaran, produksi dalam siklus hidup. Lebih lanjut lihat hal 185 blocher

Life Cycle in a Software Firm Slide 5-16 Target Costing, Theory of Constraints, and Life Cycle Costing Product Line Income Statement Analytical Decisions, Inc. ADI-1ADI-2Total Sales $4,500,000 $2,500,000 $7,000,000 Cost of Sales 1,240,0001,005,0002,245,000 Gross Margin 3,260,000 1,495,000 4,755,000 Research and Development 2,150,000 Selling and Service 1,850,000 Income Before Tax $ 755,000 Incomplete Analysis

Life Cycle in a Software Firm Slide 5-16 Target Costing, Theory of Constraints, and Life Cycle Costing Product Line Income Statement Analytical Decisions, Inc. ADI-1ADI-2Total Sales $4,500,000 $2,500,000 $7,000,000 Cost of Sales 1,240,0001,005,0002,245,000 Gross Margin 3,260,000 1,495,000 4,755,000 Research and Development 2,150,000 Selling and Service 1,850,000 Income Before Tax $ 755,000 Is ADI-I the most profitable? Incomplete Analysis

Life Cycle in a Software Firm Slide 5-16 Target Costing, Theory of Constraints, and Life Cycle Costing Product Line Income Statement Analytical Decisions, Inc. ADI-1ADI-2Total Sales $4,500,000 $2,500,000 $7,000,000 Cost of Sales 1,240,0001,005,0002,245,000 Gross Margin 3,260,000 1,495,000 4,755,000 Research and Development 1,550,000 600,000 2,150,000 Selling and Service 1,450,000 400,0001,850,000 Income Before Tax $ 260,000 $ 495,000 $ 755,000 Complete Analysis

Life Cycle in a Software Firm Slide 5-16 Target Costing, Theory of Constraints, and Life Cycle Costing ADI-2 is most profitable! Product Line Income Statement Analytical Decisions, Inc. ADI-1ADI-2Total Sales $4,500,000 $2,500,000 $7,000,000 Cost of Sales 1,240,0001,005,0002,245,000 Gross Margin 3,260,000 1,495,000 4,755,000 Research and Development 1,550,000 600,000 2,150,000 Selling and Service 1,450,000 400,0001,850,000 Income Before Tax $ 260,000 $ 495,000 $ 755,000 Complete Analysis

Latihan Target Cost • Halaman 195 No 5-19……….660 No 10-23 • Halaman 198 No 5-26……….672 No 10-34

The End See you again