Budget Formulation Process Session Overview

Understand the Budget Formulation Process in the Union and State Governments, from estimating receipts and expenditures to revising budget documents and allocating funds for programs. Learn about significant changes in planning and classification.

Budget Formulation Process Session Overview

E N D

Presentation Transcript

BUDGET FORMULATION PROCESS

Session Overview • The financial year of India begin from 1st April to 31st March, the Union Budget is presented before Parliament on the last day of February, i.e. a month before the financial year begins. which has been changed to first day of February from 2017-18. • Similarly, the Railway Budget is presented before parliament one week earlier to Union Budget. From Financial year 2017-18 the Railway Budget have been merged with Union Budget.

Session Overview • The Union Budget, as presented in Parliament, is the result of a strenuous exercise of estimated, as correct as possible, receipts and expenditure for the next year. • In this session we will discuss the Budget Formulation Process in the Union Government. • The process is more or less similar in the case of Budget formulation Process of State Governments.

Learning Objective • At the end of the session, the trainees will be able to state all the steps in the Budget Formulation Process.

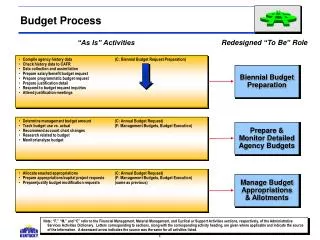

Budget Formulation Process • The budget formulation process for the ensuing financial year (April-March) starts in the month of September of the current year. • The Budget Division in the Department of Economic Affairs, Ministry of Finance, issues a 'Budget Circular' seeking statement of budget estimates from various Ministries on a specified proforma.

Budget Formulation Process • Currently the plan allocations for different Ministries are finalised after detailed discussion with the concerned departments. • Since, the Planning Commission has been replaced by NITI Aayog w.e.f 01/01/2015 and the allocative functions relating to scheme is being performed by the Ministry of Finance , there is a need for a revised framework of public expenditure budgeting.

While presenting budget for 2016-17, Hon’ble Union Finance Minister had announced that Plan-Non Plan classification will be done away with from the fiscal 2017-18 and after the 12th Plan period(2012-17). Governments focus will be on Revenue and Capital classification. • With the elimination of Plan-Non Plan distinction, there will also be need for revision of format of various budget documents to distinguish allocation in terms of Revenue and Capital expenditure and not in terms of Plan-Non Plan as is being shown currently in the expenditure related budget documents .

Magnitude of Central Assistance to be extended to the States which is an outgo from the Union Budget is finalised as per recommendation of Finance Commission. • Special attention is also given to the budgetary support to be given to Central Ministries and assistance to be given to the States for programmes/ projects which are financed through external assistance.

Preparation of Expenditure Estimates • The process for preparation of expenditure estimates for the budget starts with the issue of the 'Budget Circular' • The Financial Advisers forward this circular to the Ministry/Department and subordinate offices • The Ministries in turn collect the estimates from the organizations/ subordinate offices under their control and also prepare the same for their own activities • Theses estimates are scrutinized by the 'Budget Units' of the Ministries and submitted to their Financial Advisers.

Preparation of Expenditure Estimates • The Financial Advisers review and examine the estimates before consolidating them under different heads of expenditure, • Consolidated estimates are send by The Financial Advisers, to the 'Budget Division' of the Ministry of Finance. • These estimates are classified under separate 'Demands for Grants' in details up to the 'Object Head of Classification' and labelled as the 'Statement of Budget Estimates' • Then these are discussed by the Secretary Expenditure (Ministry of Finance) with each Financial Adviser in a series of meetings where Ministry's 'Budget Division' is also represented.

Preparation of Expenditure Estimates • 'Budget Division' in the Ministry of Finance conveys budget ceilings to each Financial Adviser for revising all the estimates within the ceilings and obtaining 'Statement of Budget Estimates' in the final form. • Meanwhile, the Controller Aid Accounts and Audit (CAA&A) also send the estimates on external debt, repayment of external loans and other payments.

Preparation of Expenditure Estimates • The final 'Statement of Budget Estimates' are to be sent to the 'Budget Division' in two stages. In the first stage, the 'Statement of Budget Estimates‘ includes:- • Revised non-plan expenditure for the current year and budget estimates for the next year; • Revised plan expenditure for the current year. • At the second stage of the 'Statement of Budget Estimates' Financial Advisers sent to the Budget Division of the Ministry of Finance, the budget estimates for plan expenditure for the next year.

Preparation of Revenue Estimates • The 'Budget Division' of the Ministry of Finance obtains revenue estimates for the next year from a large number of organizations as indicated in the figure above.These organizations and estimates collected are as under: • Central Board of Direct Taxes in the Department of Revenue of Ministry of Finance - Estimates of Direct Taxes; • Central Board of Excise and Customs in the Department of Revenue of Ministry of Finance - Estimates of Indirect Taxes; • Financial Advisers of Central Ministries - Estimates of various receipts including those of non-tax revenue, capital receipts and receipts of account of public account;

Preparation of Revenue Estimates • Reserve Bank of India - Estimates of Public Debt transactions; • Controller of Aid Accounts and Audit - Estimates of External Assistance; • State Accountants General - Estimates of recoveries from States on account of Loans and Advances from the Union Government; • Chief Controller of Accounts and Accounting Offices - Estimates of taxes and receipts of the Union Territories. • The estimates of direct taxes and indirect taxes received from the Central Board for Direct Taxes • Central Board for Excise and Customs furnishes revenue estimates for the current year and also budget estimates for the next year.

Preparation of Revenue Estimates • Chief Controller of Aid Accounts and Audit prepares the estimates for external assistance after obtaining information from the different credit units of the External Finance Division of the Department of Economic Affairs and sends the same to the 'Budget Division’ • Budget division obtains estimates on possibilities as well as sources of market borrowings from the Reserve Bank of India which may be required by the Government • This process continues till the finalisation of the budget as the various alternatives to fill the gap between receipts and disbursements are to be worked out till the end.

Budgetary Process-Flow of Estimates • Various receipts and expenditure estimates keep flowing in the Budget Division of the Ministry of Finance from October till finalisation of budget in the end of February. • From December onwards the estimates are reviewed, discussed and simulated under the overall guidance and supervisions of the Additional Secretary (Budget), who obtains guidance from Secretary (Expenditure), Secretary (Revenue) and the Finance Secretary. The group receives an overall guidance from the Finance Minister.

Budgetary Process-Flow of Estimates • Finance Minister invites the groups of leading economists, representatives of industry and trade, labour and trade unions, consumer organizations, small scale sector, science and technology sector, etc. for pre- budget discussions and receives their suggestions for the budget estimates. • Finance Minister also consults the members of the Consultative Committee of Parliament for the Ministry of Finance. • All these consultations lead to the Government firming up its expenditure policy, taxation policy and debt policy for the next year for giving a final shape to the budget.

Figure III-Overview of Budgetary Process BS: Budget support CA: Central Assistance (1) September, (2) October to December, (3) January to February, (4) March

Budget-Presentation in Parliamentand approval • The rules of procedure require that the budget is presented to Lok Sabha on such day as the President directs. • The budget is usually presented on the last day of February every year. • To enable discussion on the budget, a time table is drawn by the Business Advisory Committee of the Parliament.

Budget-Presentation in Parliamentand approval • The estimates of voted grants wherein vote of LokSabha is required are presented in the form of Demand for Grants. • Generally onedemand for Grant is presented in respect of each Ministry or Department. • Each Demand normally includes provisions required for a service, i.e. provisions on account of revenue & capital expenditure, grants-in-aids and Loans and Advances relating to the service.

Budget-Presentation in Parliamentand approval • Demand for Grants are presented to Parliament at two levels: • Main Demand for Grants along with AFS by the Budget Division, Ministry of Finance • Detailed Demands for Grants, by concerned Ministries a few days in advance of the discussion of the respective Ministry’s Demands in that House.

Budget-Presentation in Parliamentand approval • Vote on Account: Pending voting of the final demands for grants which take a longer time and may extend beyond the commencement of the new financial year, the Constitution empowers Lok Sabha to grant 'Vote on Account‘. so that necessary expenditure can be incurred. • By convention, therefore, 'Vote on Account' is treated as formality and passed by Lok Sabha without any discussion at this stage. • The 'Vote on Account' normally covers one month's expenditure requirements (or such longer period as may be considered necessary by the Finance Ministry), or till the Appropriation Bill is passed.

Budget-Presentation in Parliamentand approval • Parliamentary Standing Committees for considering demands for grants: • Standing Committees of Parliament consider the demands for grants of concerned Ministries /Departments and make a report to the Parliament to have a more satisfactory scrutiny of demands for grants • These committees hold several meetings for oral evidence and additional information for closer scrutiny of the demands.

Budget-Presentation in Parliamentand approval • The 'Guillotine': In the schedule for budget discussion made by the Business Advisory Committee, provision for 'Guillotine' is included by which if all the demands have not been considered by Parliament within the time frame prescribed, the speaker applies the 'Guillotine' and all outstanding Demands are put to the Vote of the House without further discussion.

Budget-Presentation in Parliamentand approval • The Appropriation Bill: After passing the Demands for Grants, the appropriation Bill is introduced • This is to authorize the Government to draw money from the Consolidated Fund. • After the Bill is passed, it becomes the Appropriation Act.

Budget-Presentation in Parliamentand approval • The Finance Bill: After voting on the Appropriation Bill, the Finance Bill is submitted to the Parliament containing: • proposals of the Government for levy of new taxes, • modification of existing taxes, • continuation of the existing tax structure beyond the period approved by Parliament.

Supporting and ExplanatoryDocuments • Apart from the documents prescribed by the Constitution like 'Annual Financial Statement', 'Demands for Grants', 'Appropriation Bill' and 'Finance Bill', several other documents are also presented with the budget as explained in the succeeding chart and slides.

Supporting and ExplanatoryDocuments List of supporting documents presented with Budget:- • Finance Minister's Budget Speech • Budget at a Glance • Receipt Budget • Expenditure Budget • Performance Budgets • Annual Reports • Economic Survey • Public Enterprises Survey

Principles Underlying thePreparation of Budgets • The budgets should be balanced • The estimates should be on cash basis; • There should be only one budget for all financial transactions. • Budgeting should be on gross basis and not on net basis. • Estimating, both for receipts and for expenditure should be accurate. • Budget should be on annual basis. • The rule of lapse should apply. • All appropriations expire at the close of the financial year. • The form of estimates should correspond to the form of accounts.

Budget Formulation-Guidelines • While the Central budget is presented to the Parliament by the Finance Minister, a separate statement of receipts and expenditure relating to Railways is similarly presented to the Parliament by the Ministry of railways in advance of the ‘Annual Financial Statement’ • The figures (receipts and expenditure) are also included in lump in the ‘Annual Financial Statement’.

Budget Formulation-Guidelines • The expenditure figures in the 'Annual Financial Statement' shall show separately the charged expenditure and expenditure on revenue account and expenditure under Plan. • Estimates should include suitable provision for liabilities of the previous years left unpaid during the relevant year.

Budget Formulation-Guidelines • The estimates (for both receipts and expenditure) will also include • actual expenditure for the past year, • estimates for the current year, • revised estimates for the current year and • budget estimates for the budget year.

Budget Formulation-Guidelines • The Demands for Grants will be presented to Parliament at two levels. • The main Demands for Grants are presented to parliament by the Ministry of Finance along with the Annual Financial Statement, • The Detailed Demands for Grants, after consideration by the 'Departmentally Related Standing Committee) of the Parliament, are laid on the Table of the Lok Sabha by the concerned Ministry/ Department, a few days in advance of the discussion of the respective Ministry's Demands.

Budget Formulation-Guidelines • The Form of Annual Financial Statement and for Demands for Grants is laid by the Finance Ministry . • no alteration of arrangement or classification will made without the formal approval by the Finance Ministry.

Budget Formulation-Guidelines • After the Appropriation Bill relating to Budget is passed, the Ministry of Finance communicates Budget Provisions to the Ministries/departments which, in turn, shall distribute the same to their subordinate formations. • The distribution so made shall also be communicated to the respective Pay and Accounts Officers who shall exercise checks against the allocation made to each subordinate authority.

The Fiscal Responsibility and Budget Management Act, 2003 (FRBMA) • FRBM is an Act of the Parliament of India to institutionalize financial discipline, reduce India's fiscal deficit, and improve macroeconomic management and the overall management of the public funds by moving towards a balanced budget. The main purpose was to eliminate revenue deficit of the country (building revenue surplus thereafter) and bring down the fiscal deficit to a manageable 3% of the GDP.

Main Objectives of FRBM Act • Reduce revenue deficit to nil within a period of five financial years beginning from 1st day of April 2004 and ending on 31st day of March 2009. • Reduce fiscal deficit to not more than three per cent of estimated GSDP • Ensure within a period of 14 financial years, beginning from 1st day of April 2004 and ending on 31 March 2018, that the total liabilities at the end of last financial year do not exceed 25 per cent of the estimated GSDP for that year. Contd..

Ensure not to give guarantee for any amount exceeding the limit stipulated under any rule or law of the State Government existing at the time of the coming into force of the Act or any rules or law to be made by the State Government subsequent to coming into force of this Act. • Further, the revenue deficit and fiscal deficit may not exceed the limits specified in the Act except on the ground(s) of unforeseen demands arising out of internal disturbances or natural calamities subject to the condition that the excess does not exceed the actual fiscal cost attributed to the calamities. Contd..

The State Government also responded (September 2011) to the recommendations of the Thirteenth Finance Commission by amending FRBM Act, 2004 and developed its own Fiscal Consolidation Path for 2011-15 with key aim to eliminate revenue deficits and to bring about gradual reductions in fiscal and debt levels by 2014-15.