Download

1 / 13

130 likes | 239 Views

Regulating Finance. Lots of bases to cover Cover one by regulation or deregulation Unintended Consequences Reactions to regulatory policies frustrate regulator intent Regulate bank balance sheets off-balance sheet activities Emplace a safety net bankers become skydivers

E N D

Regulating Finance • Lots of bases to cover Cover one by regulation or deregulation Unintended Consequences • Reactions to regulatory policies frustrate regulator intent Regulate bank balance sheets off-balance sheet activities Emplace a safety net bankers become skydivers • Regulation spreads to cover innovations complexity ineffectiveness Win by gaming the system

Regulation thru the decades… • Response to Crisis of 1907 • Federal Reserve Act, 1913 • Response to Great Depression • FDIC • Glass – Steagle: commercial bank/investment bank • SEC • Interest rate restraints • Tweaks during era of financial stability, 1956 • Holding companies under Fed • Douglas amendment: further limit interstate branching

Deregulation … Failures … Responses • 1980: Depository Institution Deregulation & Monetary Control Act • Response to disintermediation • Phased out interest rate ceilings • Loosened reins on thrifts • 1982: Garn – St. Germain: Unleashed thrifts • Also: Allowed depository institutions to offer Money Mkt Deposit Accts. • 1989: Financial Inst. Reform Recovery & Enforcement Act • Cleanup after S& L debacle • 1994: Riegel-Neal Interstate Banking & Branching Efficiency Act • 1999: Gramm-Leach-Biley Financial Services Modernization… • CITIGroup financial supermarket • 2002: Sarbanes-Oxley • Response to Enron, WorldCom,… • Tightened accounting standards • CEO/CFO signoff on financial statements

Regulatory Responses to Subprime-Triggered Crisis??? • Constraints on mortgage brokers??? • Ban exotic derivatives: Subprime MBS??? • Regulate compensation – clawbacks??? • Increase capital requirements • Deal with GSEs: fully privatize? nationalize?? downsize??? • Limit investment bank, insurance company risk-taking??? • Major investment banks now Fed regulated bank holding cos. • Restrict rating agency conflicts of interest??? • Increase regulation of derivatives? • Restrict over-the-counter trades • Require current bankruptcy plans • Make failure of “TBTFs” credible

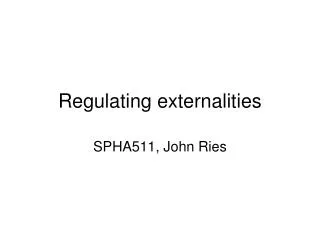

Primary Supervisory Responsibility of Bank Regulatory Agencies • Comptroller of the Currency—national banks chartered by Federal government since 1863 • Federal Reserve and state banking authorities—state banks that are members of the Federal Reserve System • Fed – also regulates bank holding companies • FDIC—insured state banks that are not Fed members • State banking authorities—state banks without FDIC insurance

The U.S. regulatory regime Sources: Financial Services Roundtable (2007), Milken Institute.

Innovations: Response to Interest Rate Volatility • Adjustable-rate mortgages teaser rates • Financial Derivatives hedging…and gambling Innovations: Response to Information Technology • Bank credit and debit cards • Electronic banking • ATM/Home banking/ABM/Virtual banking • Overrides branch restrictions • “Junk” bonds…High-yield bonds building our megaresorts • Commercial paper market – MMMF support • Securitization Innovations:Avoiding Regulation/Loophole Mining • Sweep accounts … reserve requirements • Money Market Mutual Funds … Regulation Q

Decline of Traditional Banking • Decline in cost advantages in acquiring funds (liabilities) • Rising inflation rise in interest rates and disintermediation • Low-cost source of funds, checkable deposits, declined in importance • Decline in income advantages on uses of funds (assets) • IT less need for banks to finance short-term credit and issue loans • IT lower transaction costs for other financial institutions • Bank Responses: • Riskier Lending … Commercial real estate, leveraged buyouts, takeovers • Off balance sheet activities

Size Distribution of Insured Commercial Banks, September 30, 2008 ???? 3,046 4,039 486 86 7,640 39.9 52.9 6.1 1.1 1.3 9.7 10.0 79.0

Bank Consolidation Interstate Banking and Branching Efficiency Act, 1994 • Skirting branch restrictions • ATMs, Bank Holding Cos. Geographic deregulation • Skirting branch restrictions • ATMs, Bank Holding Cos. • Pre-Crisis Findings: • Intrastate deregulation more positive for all but big banks • Raises ROA/ROE &reduces risks for banks under $15b • Non-interest expense down for banks under $1b • Increases big bank risks • NIM up for all but biggest • Interstate deregulation • Small bank risks down • Mid-sized risks up • Big bank risks mixed • ROA/ROE generally down • State of economy • Stronger impact on bank performance than branching deregulation • Benefits of bank consolidation • Increased competition close inefficient banks • Efficiencies from economies of scale and scope • Lower chance of failure -- diversified portfolios • Costs • Fewer community banks less lending to small business • Banks in new areas increased risks/failures

Attempted solutions: Constrain banks from taking too much risk • Promote diversification…but systemic crisis is systemic • Prohibit holdings of common stock • Set capital requirements … Capital as cushion • Minimum leverage ratio • Basel Accord: risk-based capital requirements … but there’s regulatory arbitrage Prompt corrective action: Close ‘em down when capital inadequate • Monitor … CAMELS • Capital adequacy • Asset quality • Management • Earnings • Liquidity • Sensitivity to market risk • Disclosure requirements … mark-to-market issue • Restrictions on competition … make banking boring

Failed Banks Update Year Number • 2000 2 • 2001 4 • 2002 11 • 2003 3 • 2004 4 • 2005/2006 0 • 2007 3 • 2008 QI+Q2 4 • 2008 Q3 10 • 2008 Q4 12 • 2009 Q1 21 • 2009 Q2 24 • 2009 Q3 50 • 2009 Q4 45 2009 Total = 140 • 2010 Q1 40 • 2010 Q2 48 • 2010 Q3 42 • 2010 thru 10/15 5 2010 Y-T-D = 135