Download

1 / 2

20 likes | 36 Views

It’s no secret that the back office of a car dealership is the wrong place to make important financial decisions. But until now, no one knew exactly how much arranging a car loan in the back office cost them. Visit: https://www.outsidefinancial.com/

E N D

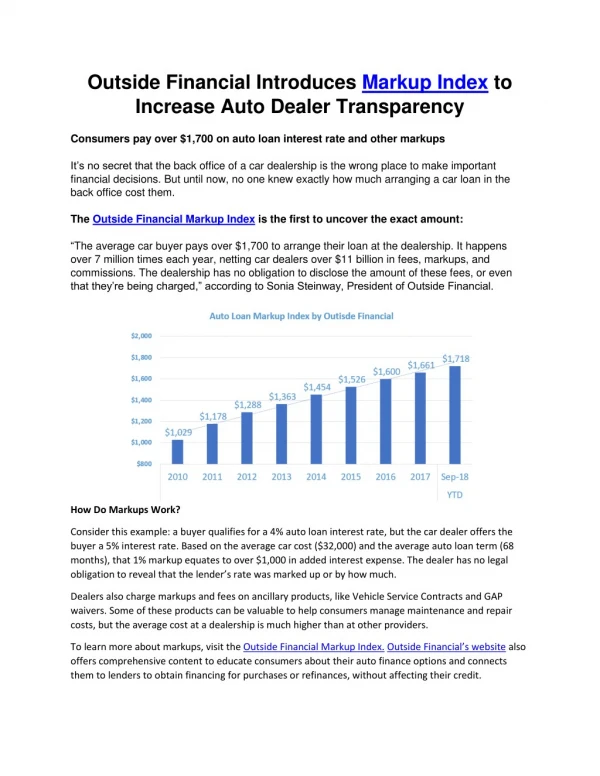

Outside Financial Introduces Markup Index to Increase Auto Dealer Transparency Consumers pay over $1,700 on auto loan interest rate and other markups It’s no secret that the back office of a car dealership is the wrong place to make important financial decisions. But until now, no one knew exactly how much arranging a car loan in the back office cost them. The Outside Financial Markup Index is the first to uncover the exact amount: “The average car buyer pays over $1,700 to arrange their loan at the dealership. It happens over 7 million times each year, netting car dealers over $11 billion in fees, markups, and commissions. The dealership has no obligation to disclose the amount of these fees, or even that they’re being charged,” according to Sonia Steinway, President of Outside Financial. How Do Markups Work? Consider this example: a buyer qualifies for a 4% auto loan interest rate, but the car dealer offers the buyer a 5% interest rate. Based on the average car cost ($32,000) and the average auto loan term (68 months), that 1% markup equates to over $1,000 in added interest expense. The dealer has no legal obligation to reveal that the lender’s rate was marked up or by how much. Dealers also charge markups and fees on ancillary products, like Vehicle Service Contracts and GAP waivers. Some of these products can be valuable to help consumers manage maintenance and repair costs, but the average cost at a dealership is much higher than at other providers. To learn more about markups, visit the Outside Financial Markup Index. Outside Financial’s website also offers comprehensive content to educate consumers about their auto finance options and connects them to lenders to obtain financing for purchases or refinances, without affecting their credit.

About the Outside Financial Markup Index The Outside Financial Auto Loan Markup Index analyzes public data from the Securities and Exchange Commission, the Federal Reserve and the Consumer Financial Protection Bureau, and industry sources, including the National Automobile Dealers Association, DealerStrong, and Auto Finance News. Coupled with qualitative interviews of current and former automobile finance executives, the Index details consumer costs from 2010 to 2018 on auto loans arranged by dealerships. The index is updated monthly and is available at www.outsidefinancial.com/markup-index.