Download

1 / 17

170 likes | 314 Views

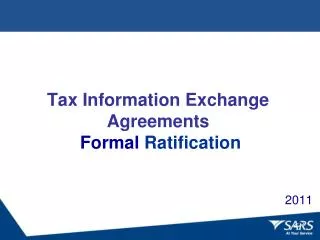

Tax Information Exchange: approach of the Member States of the BRICS. Pustovalov Evgeny Eurasian Research Centre for Comparative and International Tax Law , the Department of financial law of the Urals State Academy of Law. Network of agreements for exchange of tax information ( *).

E N D

Tax Information Exchange: approach of the Member States of the BRICS Pustovalov EvgenyEurasian Research Centre for Comparative and International Tax Law, the Department of financial law of the Urals State Academy of Law

Network of agreements for exchange of tax information (*) * according to the Global Forum

Convention on Mutual Administrative Assistance in Tax Matters

10 essential elements of the OECD standard: A. AVAILABILITY OF INFORMATION A.1. Jurisdictions should ensure that ownership and identity information for all relevant entities and arrangements is available to their competent authorities. A.2. Jurisdictions should ensure that reliable accounting records are kept for all relevant entities and arrangements. A.3. Banking information should be available for all account holders.

B. ACCESS TO INFORMATION B.1. Competent authorities should have the power to obtain and provide information that is the subject of a request under an EOI agreement from any person within their territorial jurisdiction who is in possession or control of such information. B.2. The rights and safeguards that apply to persons in the requested jurisdiction should be compatible with effective exchange of information.

C. EXCHANGING INFORMATION C.1. EOI mechanisms should provide for effective exchange of information. C.2. The jurisdictions’ network of information exchange mechanisms should cover all relevant partners. C.3. The jurisdictions’ mechanisms for exchange of information should have adequate provisions to ensure the confidentiality of information received. C.4. The exchange of information mechanisms should respect the rights and safeguards of taxpayers and third parties C.5. The jurisdiction should provide information under its network of agreements in a timely manner.

Brazil’s significant deviations from the OECD standard: • There are no explicit exceptions to the prior summoning procedure for accessing detailed bank account information. To require in all cases that the taxpayer be first approached, and thus notified, may unduly prevent or delay the effective exchange of information in urgent cases. • Although Brazil has made significant progress in response times over the three-year period, in many instances the competent authority has been unable to answer incoming requests in a timely manner. The current EOI structure and processes for handling EOI requests, in particular the lack of an appropriate level of resources and the lack of clear monitoring of timeframes for obtaining and providing information, has inhibited expedient responses to EOI requests. • Brazil does not always provide an update or status report to its EOI partners within 90 days in the event that it was unable to provide a substantive response within that time.

Russia’s significant deviations from the OECD standard: • ThescopeofinformationprotectedbyRussia’sdomesticlawconfidentialitydutyfor “auditsecrets” isbroad, andthereisnoexceptionwhichwouldpermitaccesstosuchinformationfor EOI purposes. • Thereis a dutyofconfidentialityestablishedbyRussia’s EOI agreements. HoweveritisnotclearthatenforcementmeasuresareinplacetosupportthedutywheretheinformationexchangedrelatestopersonswhoarenotRussiantaxpayers. • Russiainterpretsthe EOI provisionsin 25 ofitsDTCstolimitinformationexchangetoinstanceswheretheinformationrelatesto a personresidentinoneoftheContractingStates. UnderDTCswithtwopartners, informationexchangeislimitedtoinformationnecessaryforthecarryingouttheprovisionsoftheConvention.

India’s significant deviations from the OECD standard: India’sprocessesledin a smallnumberofcasestodelays, butthesituationgreatlyimprovedduring 2011 and 2012 withthecreationofthededicated EOI cellandtheintroductionofmeasurestostreamlinetheprocessandreduceinternaldelays. Duringthethreeyearsunderreview, Indiadidnotalwaysprovideanupdateorstatusreporttoits EOI partnerswithin 90 dayswhenitwasunabletoprovide a substantiveresponsewithinthattime. Themonitoringofrequestshasnonethelessimprovedmorerecently, withtheintroductionof a newmonitoringsystem.

China’s significant deviations from the OECD standard: NotalloftheregionsinChinahaveimplementedlegalprovisionsthatensureownershipinformationinrelationtobearersharesisavailable. China’s EOI programis, inpractice, managedbythreeofficialsinthe GCCD whofacepersonnelresourcechallengesposedbythegradualincreaseinthenumberofinboundrequestsreceivedbyChina.

SU’s significant deviations from the OECD standard: Ownershipinformationonpartnershipsisonlycomprehensivelyavailablefromthefiscalyear 2011-2012 onwards, andwhereoneofthepartnersis a trustinformationonthepartnership’snameisonlyavailableafteranautomatic, systemgeneratedquerybythetaxauthorities.

FATCA IGA 1: FFIs will be able to report information on U.S. account holders directly to their national tax authorities, who in turn will report to the IRS.

FATCA Financial Institutions in approved status as of May 23, 2014 * Total amount of registered FFI (77 500)

Main steps toward common BRICS’ tax policy (common policy in tax information exchange) • BRICS Finance Ministers’ Meeting in Washington D.C., April, 2012. • BRICS Heads of Revenue Meeting in New Delhi, January, 2013. • BRICS Heads of Revenue Meeting in Moscow, May, 2013

Communiqué of BRICS Heads of Revenue Meeting Issued in New Delhi on 18th January, 2013 “We agree to extend the cooperation on … iv. promotion of effective exchange of information” “We also agree to establish a central point of contact in each of the BRICS Countries for coordination of issues relating to taxation. The central points of contacts will identify issues of common interest in areas of International Taxation and Transfer Pricing and will develop a common response, interact and meet regularly…”