Download

1 / 1

10 likes | 117 Views

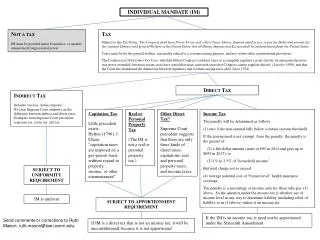

The Individual Mandate (IM) is not classified as a tax and must be justified under specific Congressional powers. While Congress can impose taxes for general welfare, they cannot use taxes to achieve regulatory goals outside these powers. Relevant Supreme Court precedents suggest a distinction between direct and indirect taxes, like income and property taxes. The IM must adhere to uniformity and apportionment requirements, as non-compliance could render it unconstitutional. This article explores these intricate legal dimensions.

E N D

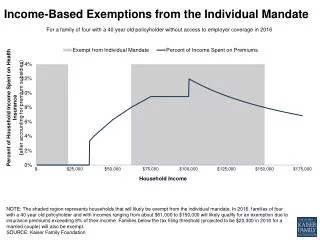

Individual Mandate (IM) Not a tax IM must be justified under Commerce, or another enumerated Congressional power Tax Subject to the Tax Power: The Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises, to pay the Debts and provide for the common Defence and general Welfare of the United States; but all Duties, Imposts and Excises shall be uniform throughout the United States. Taxes must be for the general welfare, reasonably related to a revenue-raising purpose, and not violate other constitutional provisions. The Lochner-era Child Labor Tax Case, which held that Congress could not taxes to accomplish regulatory goals outside its enumerated powers was never overruled, but more recent cases have stated that taxes can touch areas that Congress cannot regulate directly (Sanchez 1950), and that the Court has abandoned the distinction between regulatory and revenue-raising taxes (Bob Jones 1974) Direct Tax Indirect Tax Includes "excises, duties, imposts.” No clear Supreme Court authority on the difference between indirect and direct taxes Examples from Supreme Court precedent: corporate tax, estate tax, gift tax. Capitation Tax Little precedent exists. Hylton (1796), J. Chase, "capitation taxes are imposed on a per-person basis without regard to property, income, or other circumstances” Real or Personal Property Tax (The IM is not a real or personal property tax.) Other Direct Tax? Supreme Court precedent suggests that there are only three kinds of direct taxes: capitations, real and personal property taxes, and income taxes. Income Tax The penalty will be determined as follows: (1) zero if the non-insured falls below a certain income threshold If the non-insured is not exempt from the penalty, the penalty is the greater of: (2) a flat dollar amount (starts at $95 in 2014 and goes up to $695 in 2017), or (3) 1% to 2.5% of "household income" But total charge not to exceed: (4) average national cost of "bronze level" health insurance coverage The penalty is a percentage of income only for those who pay (3) above. So the question under the income tax is whether use of income level in any way to determine liability (including relief of liability as in (1) above) makes it an income tax. Subject to uniformity requirement IM is uniform Subject to apportionment requirement If the IM is an income tax, it need not be apportioned under the Sixteenth Amendment Send comments or corrections to Ruth Mason, ruth.mason@law.uconn.edu. If IM is a direct tax that is not an income tax, it will be unconstitutional because it is not apportioned