Download

1 / 14

140 likes | 149 Views

Learn about calculating taxable net profit, donations deduction, carrying forward losses per Law 91 of 2005. Examples provided.

E N D

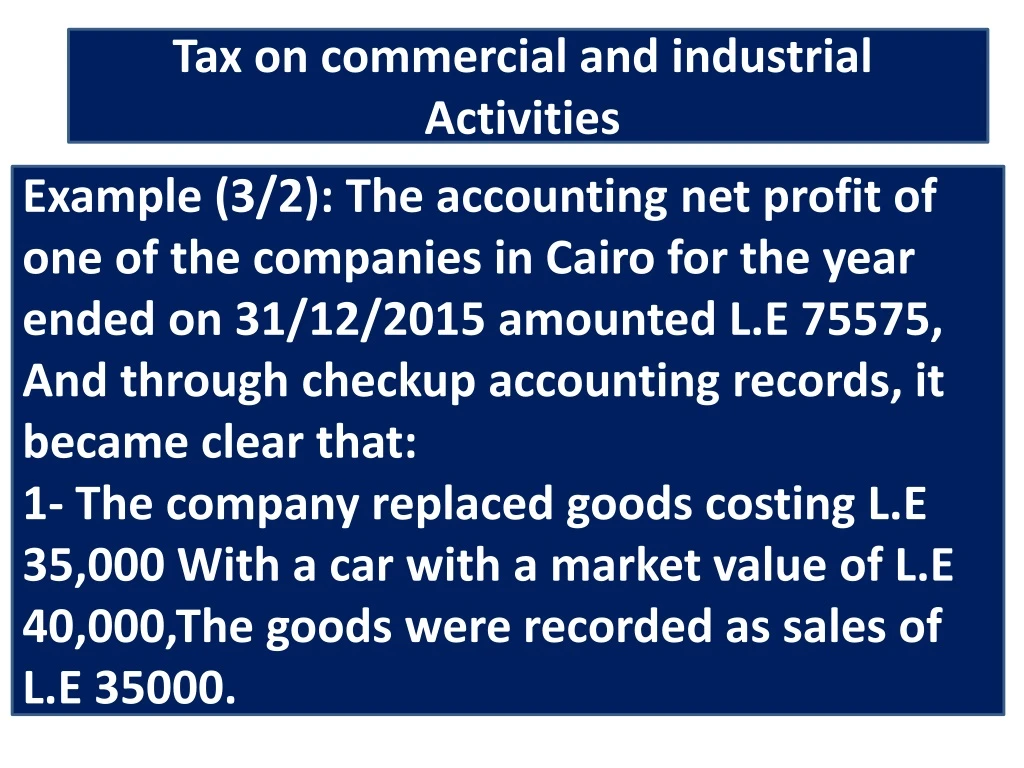

Tax on commercial and industrial Activities Example (3/2): The accounting net profit of one of the companies in Cairo for the year ended on 31/12/2015 amounted L.E 75575, And through checkup accounting records, it became clear that: 1- The company replaced goods costing L.E 35,000 With a car with a market value of L.E 40,000,The goods were recorded as sales of L.E 35000.

2- The owner of the company withdrew the goods at a cost of L.E 4500 market value L.E 5000 and the withdrawals of the goods were recognized at the market price. 3- There is a purchase bill of L.E 15,000 which appears to belong to the company owner. 4- in 1/10, Purchases of goods included amount of L.E 5000 furniture cost, Depreciated at a rate of 6% Straight line. Required: Measurement of taxable net profit.

Donations (contributions)and subsidies to government units and charities Article (23) of the law states that donations are considered costs to be deducted, as follows: 1-Donations Paid to governmental units, Local administration units, and public bodies, are considered costs to be deducted, Without a maximum, Whatever its amount.

2-Donations and subsidies paid to Egyptian NGOs provided that the said bodies and institutions are registered in accordance with the provisions of the laws governing them. As well as donations and subsidies paid to scientific bodies and hospitals subject to government supervision and scientific research institutions of Egypt, the legislator stipulated that the amount of donations and subsidies mentioned in the second, Do not exceed 10% of the net annual profit of the Taxpayer. (non governmental organizations)

Example: If the accounting net profit of sole proprietorship is LE 100,000 for the year ended 31/12/2016, and by examination of income statement, the expenses shown in the income statementinclude the following items: 1-L.E 50000, Donations to the General Authority for Health Insurance. 2-L.E 15000, Donations to the Egyptian Red Crescent Society. 3-L.E 8000, Contribution to repair and maintenance of the central hospital in the city, and the hospital subject to government supervision

4- L.E 12000, Donations and subsidies to some of the poor living. Required: Determine taxable net profit

With regard to the contributions of the General Authority for Health Insurance, it is tax deductible without a limit because it is a government agency and its deduction in the income statement is a correct procedure in terms of tax.

Carrying Forward of Losses in Law 91 of 2005 Article 29 of Law No. 91 of 2005 states that "If one of the years has ended (taxable, not accounting, net profit) with a loss, the losses is deducted from the profits of the following year until the fifth year, and after the fifth year, Nothing Of the remaining transferred from loss to account for another year. "

** If the taxpayer suffers multiple losses, the oldest loss is first carried forward, followed by the later loss. ** The loss that may be deducted from profits for the following years is the tax loss, the loss that the tax authorities adopt. In other words, the accounting loss after its adjustment as provided for in the Tax Law and Regulations.

Example: (Carrying Forward of Losses ) If it is assumed that the profits (losses) of sole proprietorshipfrom the point of view of tax authorities in the years from 2005 to 2011 were as follows: - L.E 30,000 ,Tax losses in 2005. - L.E 11000 Tax net Profit for year 2006. - L.E 5000 Tax net Profit for year 2007 -L.E 3000 Tax net Profitfor year 2008 - L.E 2000 Tax net Profit for year 2009 - L.E 6000 Tax net Profit for year 2010 -L.E 20000 Tax net Profitfor year 2011

Required: Determination of tax treatment for 2005 losses