Merger Control in the EU: Key Regulatory Insights

260 likes | 282 Views

Explore the legal basis and vast majority of non-anticompetitive concentrations. Learn about merger control's evolution, notification procedures, and market implications. Gain insights into the types of concentrations and notifications required for compliance. Understand the exclusive EU jurisdiction and referral systems for efficient merger evaluations. Delve into the Dutch and German clauses under the Merger Regulation for cross-border effects on competition.

Merger Control in the EU: Key Regulatory Insights

E N D

Presentation Transcript

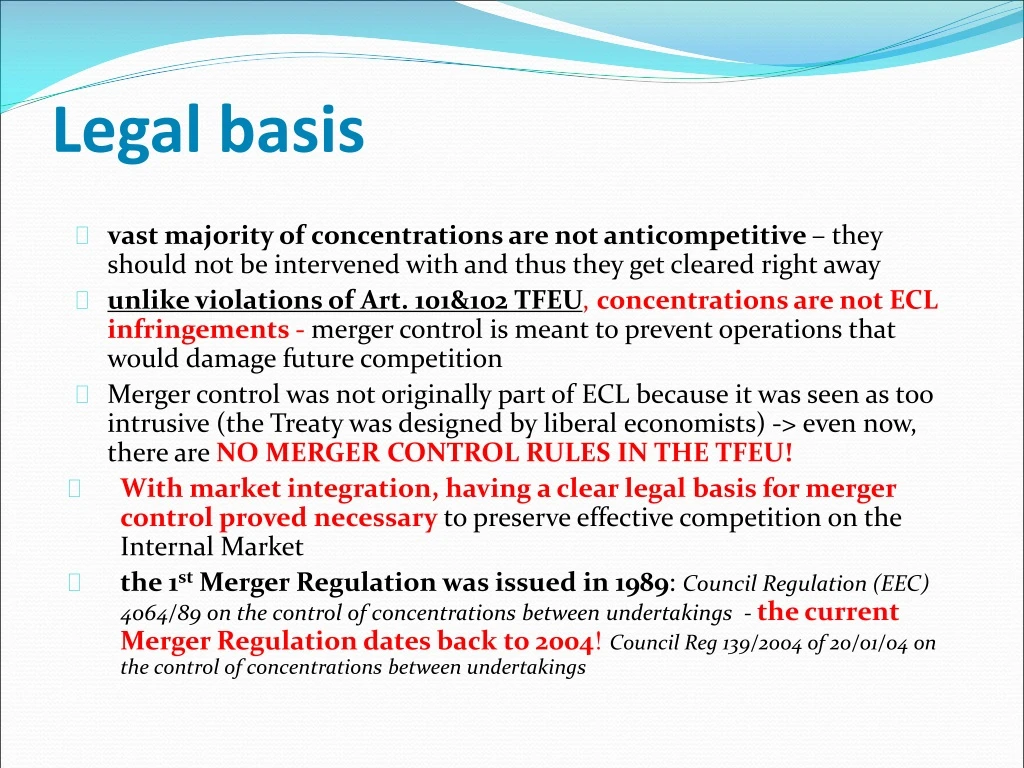

Legal basis • vast majority of concentrations are not anticompetitive– they should not be intervened with and thus they get cleared right away • unlike violations of Art. 101&102 TFEU, concentrations are not ECL infringements -merger control is meant to prevent operations that would damage future competition • Merger control was not originally part of ECL because it was seen as too intrusive (the Treaty was designed by liberal economists) -> even now, there are NO MERGER CONTROL RULES IN THE TFEU! • With market integration, having a clear legal basis for merger control proved necessary to preserve effective competition on the Internal Market • the 1st Merger Regulation was issued in 1989: Council Regulation (EEC) 4064/89 on the control of concentrations between undertakings - the current Merger Regulation dates back to 2004! Council Reg 139/2004 of 20/01/04 on the control of concentrations between undertakings

‘Pre-emptive’ enforcement • PLANED concentrations that fulfil the EU jurisdictional criteria (EU dimension) must be NOTIFIED to the Commission • The notification procedure ‘pre-empts’ the practice • a CLEARANCE decisionmust be obtained from the Commission to implement a concentration with EU dimension • Merger decisions should be taken as fast as possible to minimise the restriction of economic freedom (art.10 MR limits investigation to 25-35 days for Phase I & 90-125 days for Phase II) • Merger control timeline • Intention to concentrate (including hostile take overs) (in PL egumowaprzedwstepna) • Notification: what, to whom, when? • Receive clearance/conditional clearance • Complete the operation • Fulfil obligations attached to conditional clearances by a fixed date

1. Concentrations concentration = change of control on a lasting basis resulting from a • merger of independent companies or • acquisition of control incl. the creation of a joint venture [MR Article (3)(1), (2) & (4)] so called ‘MERGERS & ACQUISITIONS’ + full function JV 3 different ‘economic’ types of concentrations: -horizontal(between competitors) - vertical (eg. producer → distributor or distributor → supplier) -conglomerate(no common markets)

2. Notifications The turnover of the participants is decisive when it comes to the question IF an operation must be notified ↓ ALL concentrations between BIG COMPANIES are subject to ECL irrespective of the ‘nationality’ of the parties or location of the operation concentrations with EU(COMMUNITY) DIMENSION • combined EU-wide turnover of each of at least 2 participants > 250 mil EUROunless each of the companies gets more than 2/3/ of its aggregate EU turnover within 1 MS (eg large energy companies acting only in a single country) AND • a combined globalturnover > 5 000 mil EURO NOTE: 14/09/18 notification concerns Walt Disney Company and 21st Century Fox (Fox will remain outside); Disney acquired Lucas Films in 2012

Exclusive EU jurisdiction • Fulfilling the EU jurisdictional criteria (EU dimensions) generally means that the operation also fulfils national jurisdictional criteria (within the EU and elsewhere) • Within the EU, concentrations with EU dimension are to be NOTIFIED to the Commission only, even if they also fulfil jurisdictional criteria of individual MSs • This is known as the one-stop-shop principle meant to minimise delays and inconsistencies in merger decisions(= minimise negative market consequences (extraterritorial) pre-emptive merger control) • The European Commission has therefore‘exclusive jurisdiction’ to apply the MR NOTE: Concentrations with EU dimension are often also investigated elsewhere in the world and the decisions reached by the authorities do not have to be in agreement

Referrals EU->MS<-EU the pre-notification stage a concentration will not have EU dimension, despite fulfilling the turnover thresholds, if all of the parties to the operation achieve 2/3 of their EU turnover in the same MS– such operation has to be notified to the relevant NCAs the post-notification referral system The Commission has the discretion to accept /refuse referrals from/to NCAs • Article 9 MR - concentrations with Community dimension can be referred to MS, in whole or in part (the German Clause) • Article 22 MR - concentrations without Community dimension but with cross-border effects can be referred by MS to the Commission (the Dutch clause)

Dutch & German clauses Article 22 MR: from MS → Commission – it now takes place when a single transaction is notified to multiple NCAs and covers transactions that • Have no EU dimension but do affect trade between EU MSs; and • threaten to significantly affect competition within the territory of the requesting MSs Eg. Greece + Cyprus requested the Commission to assess Aegan/Olympic II COMP/M.6773 Article 9 MR: from Commission → MS for transactions with EU Dimension but of particular impact on a specific MS The Commission can accept a referral request submitted by a NCA if the operation: • threaten to affect competition significantly in a market in the requesting MS which has the characteristics of a distinct market (max national in scope); or • affect competition in a market in the requesting MS which has the characteristics of a distinct market and which does not constitute a substantial part of the EU egM.4522 Carrefour/ AholdPolska– UOKiK issued a conditional clearance

3. Substantive test = SIEC Only those concentrations will be stopped(banned) which are dangerous to future competition = likely to result in a significant impediment of effective competition (SIEC), in particular creation or strengthening dominant position (Article 3(2) & (3) MR) Unlike in Art. 102 TFEU that prohibits abuse not dominance, under the MR, the sole creation or strengthening of dominance can thus cause a merger to be prohibited NOTE: Until 2004, EU mergers were not allowed to create or strengthen a dominant position that would impede effective competition old test = dominance → impediment

SIEC SIGNIFINAT(not minor) IMPEDIMENT OF (must worsen) EFFECTIVE(is there effective competition before the operation?) COMPEITION eg the creation or strengthening of dominance DOMINANCE = SIEC per se Other factors relevant to assess SIEC • market share (<25% assumption that SEIC test is not fulfilled) • market concentration levels (HHI) • countervailing buying power • market entry + verifiable efficiencies (must benefit consumers, be merger specific ) + failing firm defence

Unilateral vs. coordinated effects SIEC can occur because of two types of anticompetitive effects of a concentration • unilateral (non-coordinated) effectsor • multilateral(coordinated) effects UNILATERAL EFFECTS are typical = the concentration lowers the level of competition(hence mostly horizontal mergers) They relate to the creation/strengthening of market power: • Increase in market share of the ‘merged’ entity • other ‘factors indicating dominance’ eg elimination of competing R&D • Increase in market concentration levels/decrease in competitive pressure

HHI Herfindahl-Hirschman Index = HHI calculated by squaring the market share of each firm competing in a market, and then summing the resulting numbers HHI = s1^2 + s2^2 + s3^2 + ... + sn^2 from 0 (nearly perfect competition) to 10,000 (monopoly, 1x100%) • < 1000 HHI = low concentration level • 1000-1800 HHI = medium • 1800-2400 HHI = high • > 2400 HHI = very high concentration A concertation should not be permitted (according to economic theory) if it results in a one-off increase by 150 points

Carey Agri/Jablonna UOKiK prohibition 04/05/06 nr DOK 41/06 Carey Agri (owner of POLMOS BIALYSTOK) zoladkowa + Jablonna (owner of POLMOS LUBLIN) zubrowka RM: national market for the sale of ‘flavoured’ vodka Market share after the operation: >40% for Carey HHI before the operation 2037 (high) HHI after the operation 3317 (very high)

Coordinated effects A CONCENTRATION might FACILITATE ‘COORDINATED’ effects = Make it possible/easy to coordinate MARKET BEHAVIOUR of multiple entities • In Horizontal mergers - it might facilitates cartelswhen the market players have: • ability to monitor behaviours of other firms; • credible deterrent mechanism; • actions of outsiders/consumers don’t pressure the coordination • In non-horizontal mergers – it might facilitate foreclosure

AOL/Time Warner AOL/Time Warner Case M.1845 conditional clearance issued in 2000 the Commission feared an exceptionally widespread potential foreclosure effects due to: the non-horizontal character of the merger + leadership in the market & superior technological know-how thus it was feared that after the merger AOL could • charge supra-competitive prices for the carriage content • favour TW/Bertelsmann - worsen access for ors • dictate the technical standards for internet music NOTE: the fear was justified since an internal pre-merger document stated that: one of the missions of the TW/AOL deal is to “[to ensure mass adoption of digital download delivery standards]

4. Merger decisions NOTIFICATION → administrative decision • CLEARANCE (UNCONDITIONAL) → merger can be implemented ‘as is’[Art. 6(1)b (phase 1) MR or 8(1) (phase 2) • CONDITIONAL CLEARANCE→ merger can be implemented according to the accepted ‘remedies’ • PROHIBITION→ merger cannot proceed • >90% of EU notifications are cleared • Most concentrations that raise serious doubts get a cond. clearance • Few operations are entirely prohibited

4.1.Clearances Unconditional clearances are issued for most notifications concentrations (cases that do not rise serious concerns) 8/02/10 Microsoft/Yahoo search 7/10/11 Microsoft/Skype (13/2/12 Google & Motorola) 10/2/12 GE/Microsoft (JV) 4/12/13 Microsoft & Nokia Devices & Services RM: downstream smart phones, Mobile OS, Mobile APPs Future: no overlaps, no potential & no incentive for future misconduct (no danger of ‘abuse’ since no dominance) 22/09/16 FIH Mobile & Feature Phone Business of Microsoft Mobile ?14/09/18 Microsoft/GITHUB

exceptional clearances An exceptional clearance can be used in special cases such as the FAILING FIRM DEFENCE [Guidelines on the assessment of horizontal mergers (2004/C 31/03)] where an otherwise problematic merger is compatible if one of the merging parties is a failing firm -the deterioration of competition after the merger is not caused by the concentration • the ff would in the near future be forced out of the market • there is no less anti-competitive alternative purchaser • without the merger, the assets of the ff would inevitably exit the market M.6796 Aegan/ Olimpic II 2013 NOTE: Some MSs including PL have ‘exceptional clearances’ for mergers that restrict competition but must be allowed for other reasons

4.2. Conditional clearance Conditional clearances are issued for mergers that cannot be cleared in the form they were notified but can be cleared provided the merging entities agree to some concessions MERGER REMEDIES can be structural or behavioural Structural = partial divestiture • separation of merged undertaking • sale of assets • disposition of stock or shares Behavioural remedies = how to behave in the future e.g. use of open technology, non discriminatory access, information disclosure – must have monitoring facilities to be effective

Universal/EMI RECORDED MUSIC 21/09/12 (M.6458) SPECIAL CONSIDERATIONS which justified a clearance despite clear negative, unilateral effects on competition resulting from the merger of the 2nd and 4th larges record company • ‘special’ social importance of music • economic difficulties of the industry overall and EMI in particular • challenge of digitalisation – piracy (lower income due to illegal access) & small size of record companies vs. on-line giants Apple, Goggle THREAT TO COMPETITION: Combined MS (40%) would allow Universal to overcharge its customers & use onerous licensing terms to on-line music providers especially SMEs & novel service operators COMMITTMENTS: • Extremely large divestiture of worldwide rights to digital & physical music = up to 2/3 of EMI EU revenue sources incl. EMI Recording Ltd + EMI’s 50% share in ‘Now this is what I call music’ + obligation to give licence to this venture for 10 year • forbidden to re-sign for 10 years • must be sold to a music company(not bank/fund etc)

Microsoft/LinkedIn Commission decision of 6 December 2016 Investigation focused on (a) professional social network services (danger of pre-installing LinkedIn + integrate LinkedIn into Office and integrate their databases) (b) customer relationship management software solutions (c) online advertising services Commitments offered: • PC manufacturers /distributors will remain free not to pre-install LinkedIn on Windows and users will be able to remove it • Allow current level of interoperability to other professional social network service providers with Office • Granting competing professional social network service providers access to Microsoft Graph (gateway for software developers) • Remedies applicable in the EEA for 5 years

4.3. Prohibitions Merger prohibitions are only issued if a concentration cannot be allowed under any circumstances – • parties refuse to offer remedies [TW/EMI] or • parties offer insufficient remedies [MSG] or • the parties & Commission cannot design remedies that would alleviate the competition problem [RYAN AIR] only 1 in about 250 EU notifications ends in a prohibition • 2013 UPS/TNT Express • 2013 Ryanair/AerLingus • 2012 Deutsche Borse/NYSA Euronext • 2011 Aegean Airlines/Olympic Air • 2008 withdrawn notification Ryanair/AerLingus • 27 June 2007 Ryanair/AerLingus - upheld by the GC 6 July 2010 (T-342/07)

Airline mergers Aegan Airlines/Olympic 2011 RM: typical city pairs operation – with the same ‘home’ airport Combined MS: quasi monopoly on 9 routs Lack of workable commitments: slots were not sparse NOTE: merger allowed 2013 due to failing firm defence Ryan Air/AerLingus 2013 RM: point-to-point scheduled air trasport Combined MS: monopoly on 28 out of 46 overlap routs with a 87% join MS in 2012 (80% in 2007) Lack of workable commitments: mostly divestment to Flybe which was not a ‘feasible’ buyer

fines related to mergers Up to 10 % turnover for failure to notify (intentionally or negligently)– so-called „JUN JUMPING” 06/09 Fine for Electrabel (EUR 20 million) for implementing its acquisition of CNR without approval (Case COMP/M.4994). Up to 1 % turnover for failure to fulfil info duty (intentionally or negligently): supplied incorrect, incomplete, misleading information; does not supply in time Up to 1% turnover for breaking seals made during inspections Up to 10% turnover for failure to comply with EC decision + periodic penalty payments: up to 5 % of the average daily aggregate turnover of the undertaking for each working day of delay, calculated from the date set by the Commission in its decision requiring information, ordering inspections, etc.

Gun jumping Implementing a merger without clearance – up to 10% fine 06/09 Fine for Electrabel (EUR 20 million) for implementing its acquisition of CNR without approval (Case COMP/M.4994). The notification was cleared in 03/08 but it was later discovered that Electrabel had actually acquired de facto control of CNR in 2003 Electrabel appealed - General Court dismissed the action 12/12 (Electrabel v Commission (Case T-332/09)) Electrabel appealed again 21/02/13 the ECJ (Electrabel v Commission (Case C-84/13 P)).