Download

1 / 10

0 likes | 9 Views

The overview delves into the intricacies of the Saudi Aramco IPO, exploring the Saudi Arabian context, privatization challenges, and specific issues related to privatizing Saudi Aramco. The drive for privatization stems from economic reforms aimed at diversification and revenue generation. Key concerns include disentangling the conglomerate, valuation dilemmas, and the need for transparency. Despite potential hurdles, the privatization program presents significant opportunities for economic transformation.

E N D

Saudi Aramco IPO – An overview Professor Paul Stevens Distinguished Fellow, Chatham House Professor Emeritus, University of Dundee Distinguished Fellow, Institute of Energy Economics, Japan Fossil Fuel Expert Round Table Chatham House 6thOctober 2017 20 mins

Presentation outline • The Saudi Arabian context • The privatization programme • Problems with privatization: general • Problems with privatization: Saudi Aramco Chatham House | The Royal Institute of International Affairs 2

The Saudi Arabian context Oil prices 2000-2016 (Brent) $2016 140 120 • Lower oil prices and budget implications 100 80 60 40 20 • Budgetary break even? • Apicorp August 2014 = $92 • IMF Early 2017 = $84 • MEES August 2017 = $67.6 0 2000 1990 1992 1994 1996 1998 2002 2004 2006 2008 2010 2012 2014 2016 Saudi Budget: Actual surplus/deficit 2010- 16 Mn rials 500000 400000 300000 200000 100000 0 -100000 -200000 -300000 -400000 Chatham House | The Royal Institute of International Affairs 3

The Saudi Arabian context Lower oil prices eating into financial reserves • Has been a serious failure to diversify • Weak private sector lacking property rights • “Change of personnel” Salman - Jan 2015 • MbS is head of reform and attracting some young Saudis but his position is uncertain? • Family alliances against him? • Economic reforms unpopular? • Disastrous war in Yemen • Growing “fundamentalist” opposition? • Saudi Arabia GDP constant 2010 prices Serious need for reform hence “Vision 2030” (April 2016) and the NTP (June 2016): • 543 initiatives. 346 targets including increasing non-oil revenue 3x by 2020. 5% VAT in 2018. Sort out public finances • Enhance private sector involvement to diversify the economy • Increase the employment of nationals (27% of population < 15 years old) Create 1.2 million private sector jobs by 2020 • Address social problems such as housing • Increase local content in spending from 36% to 50% by 2020 • 100% 80% 60% 40% 20% 0% 2010 2011 2012 2013 2014 2015 2016 Central to the NTP is the “privatization programme” • 1. Agriculture, Forestry & Fishing 2. Mining and Quarrying : 3. Manufacturing: 4. Electricity, Gas and Water 5. Construction 6. Wholesale & Retail Trade, 7. Transport, Storage & Communication 8. Finance, Insurance, Real Estate 9. Community, Social & Personal Services Chatham House | The Royal Institute of International Affairs 4

The privatization programme • Driven by a neo-Thatcherite “ideology” plus the need for revenue • Part of The National Transformation Programme • National Center for Privatization has targeted > 100 state owned enterprises • Central pillar is to privatize 5% of Saudi Aramco in early 2018 (going against the advice of McKinsey) • Funds from programmes (Saudi Aramco “valued” at $100 billion) paid into the Saudi Public Investment Fund. Capital to increase from $160 billion to 2 trillion by 2030 to fund diversification • Nov 2016 transferred $27bn from Central Bank reserves to PIF. Aim to increase foreign assets from 5 to 50 percent. Chatham House | The Royal Institute of International Affairs 5

Problems with privatization: general • Complex story • BUT to improve enterprise performance it is not enough to simply change the property rights • The key is creating competition • To maximize revenue sell as a monopoly • In Saudi: buyers with political ‘influence’ will maintain incumbent’s monopoly https://www.chathamhouse.org/publication/economic- reform-gcc-privatization-panacea-declining-oil-wealth Chatham House | The Royal Institute of International Affairs 6

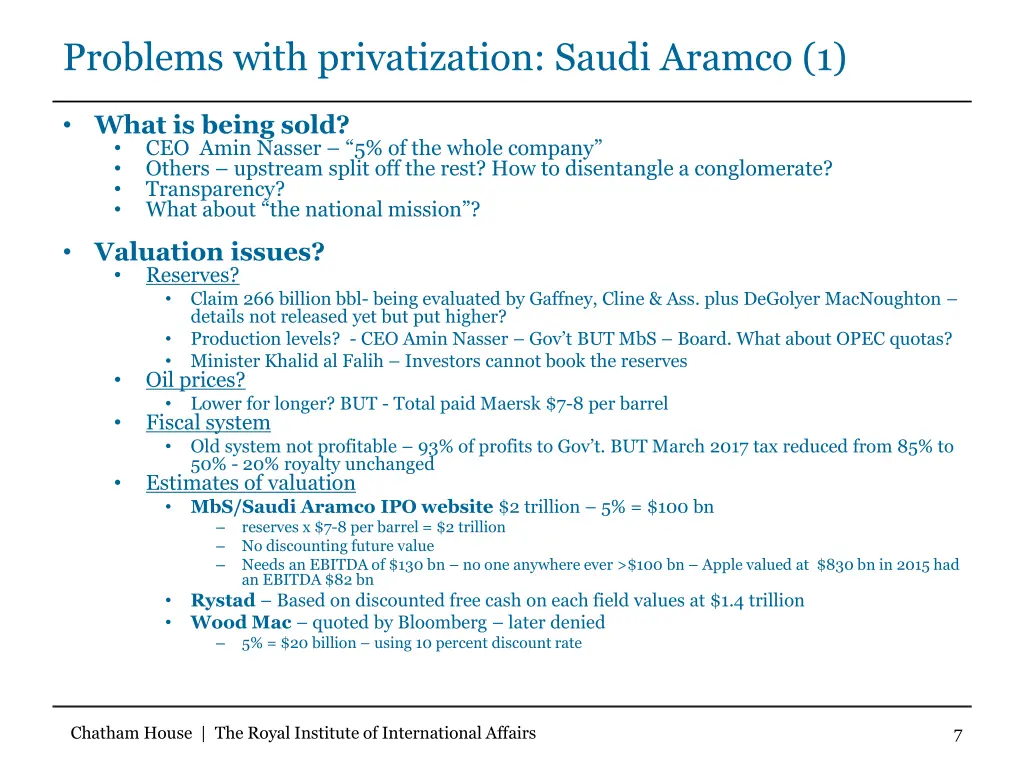

Problems with privatization: Saudi Aramco (1) What is being sold? • CEO Amin Nasser – “5% of the whole company” • Others – upstream split off the rest? How to disentangle a conglomerate? • Transparency? • What about “the national mission”? • Valuation issues? • Reserves? • Claim 266 billion bbl- being evaluated by Gaffney, Cline & Ass. plus DeGolyer MacNoughton – details not released yet but put higher? • Production levels? - CEO Amin Nasser – Gov’t BUT MbS – Board. What about OPEC quotas? • Minister Khalid al Falih – Investors cannot book the reserves • Oil prices? • Lower for longer? BUT - Total paid Maersk $7-8 per barrel • Fiscal system • Old system not profitable – 93% of profits to Gov’t. BUT March 2017 tax reduced from 85% to 50% - 20% royalty unchanged • Estimates of valuation • MbS/Saudi Aramco IPO website $2 trillion – 5% = $100 bn – reserves x $7-8 per barrel = $2 trillion – No discounting future value – Needs an EBITDA of $130 bn – no one anywhere ever >$100 bn – Apple valued at $830 bn in 2015 had an EBITDA $82 bn • Rystad – Based on discounted free cash on each field values at $1.4 trillion • Wood Mac – quoted by Bloomberg – later denied – 5% = $20 billion – using 10 percent discount rate • Chatham House | The Royal Institute of International Affairs 7

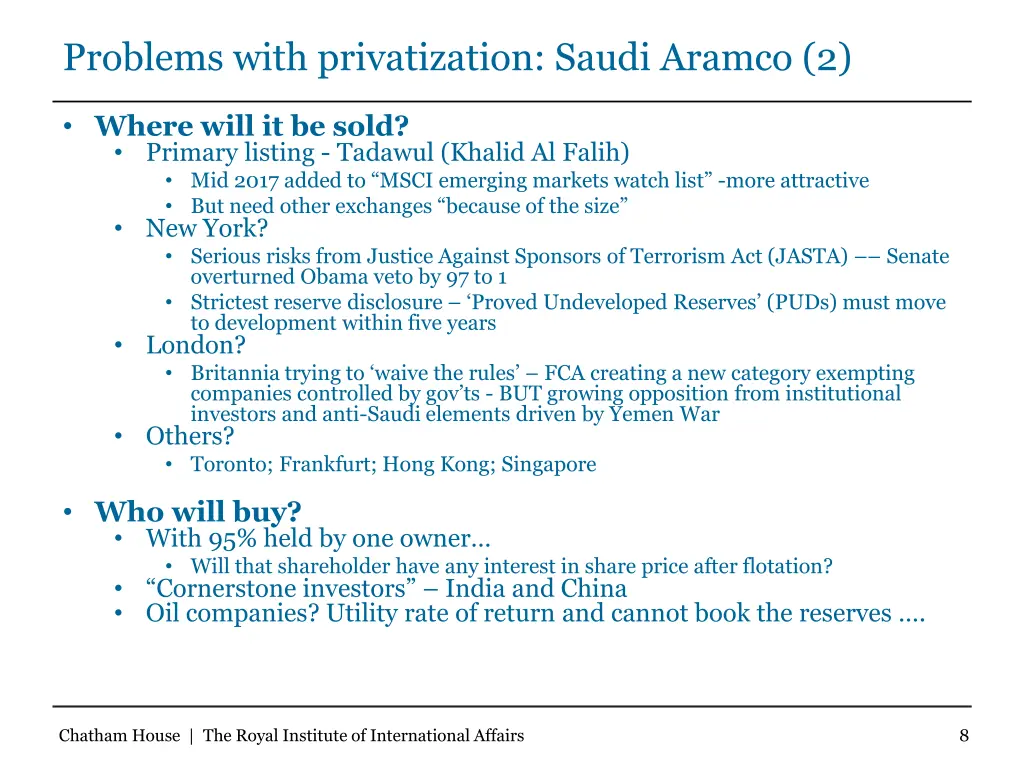

Problems with privatization: Saudi Aramco (2) • Where will it be sold? • Primary listing - Tadawul (Khalid Al Falih) • Mid 2017 added to “MSCI emerging markets watch list” -more attractive • But need other exchanges “because of the size” • New York? • Serious risks from Justice Against Sponsors of Terrorism Act (JASTA) –– Senate overturned Obama veto by 97 to 1 • Strictest reserve disclosure – ‘Proved Undeveloped Reserves’ (PUDs) must move to development within five years • London? • Britannia trying to ‘waive the rules’ – FCA creating a new category exempting companies controlled by gov’ts - BUT growing opposition from institutional investors and anti-Saudi elements driven by Yemen War • Others? • Toronto; Frankfurt; Hong Kong; Singapore • Who will buy? • With 95% held by one owner… • Will that shareholder have any interest in share price after flotation? • “Cornerstone investors” – India and China • Oil companies? Utility rate of return and cannot book the reserves …. Chatham House | The Royal Institute of International Affairs 8

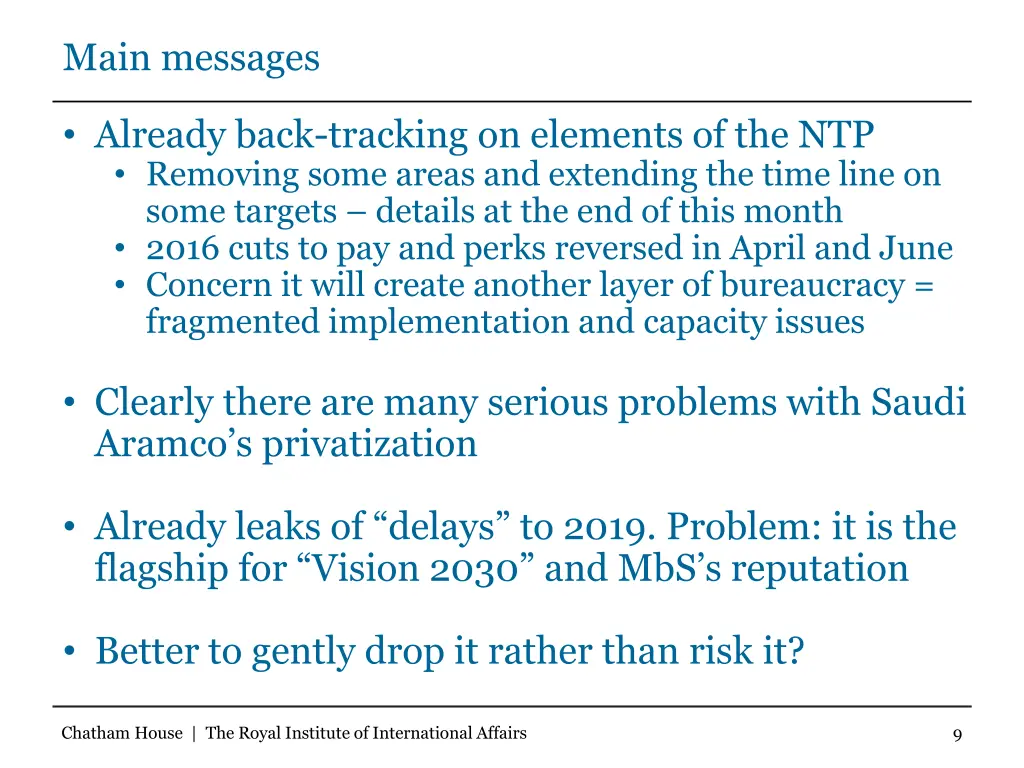

Main messages • Already back-tracking on elements of the NTP • Removing some areas and extending the time line on some targets – details at the end of this month • 2016 cuts to pay and perks reversed in April and June • Concern it will create another layer of bureaucracy = fragmented implementation and capacity issues • Clearly there are many serious problems with Saudi Aramco’s privatization • Already leaks of “delays” to 2019. Problem: it is the flagship for “Vision 2030” and MbS’s reputation • Better to gently drop it rather than risk it? Chatham House | The Royal Institute of International Affairs 9

THANK YOU FOR YOUR ATTENTION pstevens@chathamhouse.org