An Overview of Private Equity: Key Concepts, Categories, and Future Challenges

This document provides a comprehensive overview of private equity, defining it broadly as any equity investment in assets not freely tradable on public markets. It explores categories and key players within the private equity landscape, including angel investors, venture capitalists, and traditional private equity firms. Emphasizing the significance of leverage and value creation, it discusses strategic financial principles and examples like the Carlyle Group's leveraged buyouts. It also addresses ongoing challenges in the field, such as regulatory risks and market dynamics that could affect future performance.

An Overview of Private Equity: Key Concepts, Categories, and Future Challenges

E N D

Presentation Transcript

Private EquityAn Overview Clark L. Maxam, Ph.D. Director of Research – Braddock Financial Corporation and El Pomar Professor of Entrepreneurial Finance – University of Colorado, Colorado Springs

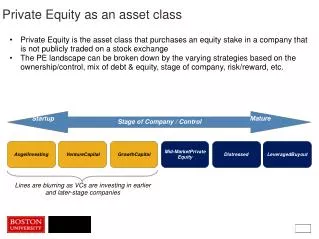

Private Equity – Broadly Defined • Technically refers to any type of equity investment in an asset in which the equity is not freely tradable on a public market. • Less liquid • Long Term in nature

Private Equity – Categories and Players • Angel • Early Stage: Seed, Start-up • Professional Venture Capital • Early Stage, Expansion, Later Stage • Private Equity • Later Stage, Buyout, Special Situations • Hedge Funds • All Stages

Key Player Overlap Angel Venture Capital Private Equity Hedge Funds

Traditional Private Equity – Primary Activity • Professional pools of capital that buy all the publicly traded equity of target companies = “Go Private” • Usually done with borrowed money • High degree of leverage • Aka : Leveraged Buyout

The Basic Value Creation FormulaFundamental Ideas • Re-focuses acquired businesses resulting in lower costs and improved efficiency. • Value is created through basic finance that says debt can increase firm value if you can afford it! • Exploits corporate aversion to debt (Henry McVey, Morgan Stanley). • Regulatory Arbitrage – Sarbanes-Oxley

The Basic Value Creation FormulaDebt can increase Value Dupont Equation Leverage – Debt as % of Assets Equity Multiplier ROE

The Basic Value Creation FormulaDebt can increase Value Consider a company that takes on debt at a cost of $3 in Net Income, but changes NOTHING ELSE. Could drop NI to 4.8 and still match the previous ROE!!

The Basic Value Creation FormulaAn Example – Carlyle Group Leveraged Buyout Case 1 (5 years) – No Profit Increase Case 2 (5 years) – Profit Increase

Private Equity Investments by Country Source: International Financial Services

Source: National Venture Capital Association,Thomson Venture Economics

Private Equity Issues Going Forward • PE as a new Model of General Management (Jensen) • Overcomes entrenched thinking, management and disjoint between manager incentives and capital markets. • Problematic Trends • Publicly held Private Equity – oxymoron • Fee Structures not tied to exit • Hedge funds in the PE business – not a transaction business.

Private Equity Issues Going Forward • 2007 estimate of$160B in dry powder $750B $590B in debt appetite. • Banking capacity is finite and already extended. • Potential regulatory limits

Private Equity Issues Going Forward • PE Boom has been fueled by • Historically low rates • Regulatory arbitrage • Both could reverse quickly and change the metrics dramatically