Private Equity An Overview

Private Equity An Overview. Clark L. Maxam, Ph.D. Director of Research – Braddock Financial Corporation and El Pomar Professor of Entrepreneurial Finance – University of Colorado, Colorado Springs. Private Equity – Broadly Defined.

Private Equity An Overview

E N D

Presentation Transcript

Private EquityAn Overview Clark L. Maxam, Ph.D. Director of Research – Braddock Financial Corporation and El Pomar Professor of Entrepreneurial Finance – University of Colorado, Colorado Springs

Private Equity – Broadly Defined • Technically refers to any type of equity investment in an asset in which the equity is not freely tradable on a public market. • Less liquid • Long Term in nature

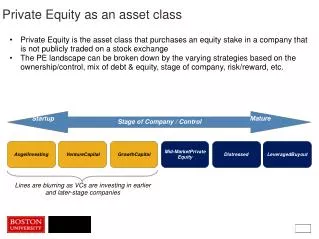

Private Equity – Categories and Players • Angel • Early Stage: Seed, Start-up • Professional Venture Capital • Early Stage, Expansion, Later Stage • Private Equity • Later Stage, Buyout, Special Situations • Hedge Funds • All Stages

Key Player Overlap Angel Venture Capital Private Equity Hedge Funds

Traditional Private Equity – Primary Activity • Professional pools of capital that buy all the publicly traded equity of target companies = “Go Private” • Usually done with borrowed money • High degree of leverage • Aka : Leveraged Buyout

The Basic Value Creation FormulaFundamental Ideas • Re-focuses acquired businesses resulting in lower costs and improved efficiency. • Value is created through basic finance that says debt can increase firm value if you can afford it! • Exploits corporate aversion to debt (Henry McVey, Morgan Stanley). • Regulatory Arbitrage – Sarbanes-Oxley

The Basic Value Creation FormulaDebt can increase Value Dupont Equation Leverage – Debt as % of Assets Equity Multiplier ROE

The Basic Value Creation FormulaDebt can increase Value Consider a company that takes on debt at a cost of $3 in Net Income, but changes NOTHING ELSE. Could drop NI to 4.8 and still match the previous ROE!!

The Basic Value Creation FormulaAn Example – Carlyle Group Leveraged Buyout Case 1 (5 years) – No Profit Increase Case 2 (5 years) – Profit Increase

Private Equity Investments by Country Source: International Financial Services

Source: National Venture Capital Association,Thomson Venture Economics

Private Equity Issues Going Forward • PE as a new Model of General Management (Jensen) • Overcomes entrenched thinking, management and disjoint between manager incentives and capital markets. • Problematic Trends • Publicly held Private Equity – oxymoron • Fee Structures not tied to exit • Hedge funds in the PE business – not a transaction business.

Private Equity Issues Going Forward • 2007 estimate of$160B in dry powder $750B $590B in debt appetite. • Banking capacity is finite and already extended. • Potential regulatory limits

Private Equity Issues Going Forward • PE Boom has been fueled by • Historically low rates • Regulatory arbitrage • Both could reverse quickly and change the metrics dramatically