Download

1 / 13

150 likes | 314 Views

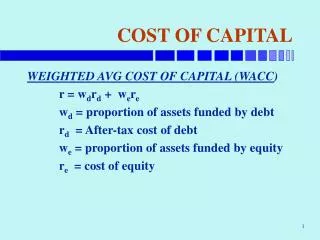

COST OF CAPITAL. WEIGHTED AVG COST OF CAPITAL (WACC ) r = w d r d + w e r e w d = proportion of assets funded by debt r d = After-tax cost of debt w e = proportion of assets funded by equity r e = cost of equity. COST OF CAPITAL. WACC = 40(.10)+10(.15)+50(.18)

E N D

COST OF CAPITAL • WEIGHTED AVG COST OF CAPITAL (WACC) • r = wdrd + were • wd = proportion of assets funded by debt • rd = After-tax cost of debt • we = proportion of assets funded by equity • re = cost of equity

COST OF CAPITAL WACC = 40(.10)+10(.15)+50(.18) = 4 + 1.50 + 9 = 14.50% • rd = 10% rp = 15% re = 18% • wd = 40% wp = 10% we = 50% • Proof: Firm raises $100 -- Buys an Asset • Asset earns $14.50: • Debt: $40 @ 10% = $ 4.00 • Prefs: $10 @ 15% = $ 1.50 • Equity: $50 @ 18% = $ 9.00 • Total $14.50

COST OF CAPITAL • WEIGHTS: • BOOK VALUE • MARKET VALUE • TARGET • COSTS: • HISTORIC • CURRENT (MARGINAL)

COST OF CAPITAL • ESTIMATING COSTS • DEBT: BANK RATE • YIELD TO MATURITY ON BONDS • Find the IRR on the bond: PV=Price • FV = 1000 • Payment = Coupon/2 • N = #years * 2 • Return you get (irr) is a six month return • Yield to maturity = rd = 2*irr • Note: Strictly, rd = (1+irr)2 - 1

COST OF EQUITY • Constant Growth Model: • re = DY + CGY • DY = Dividend Yield • CGY = Capital gains Yield (Growth) • Capital Asset Pricing Model • re = rf + (Mkt Premium) • rf = Risk Free Rate • = Relative Riskiness of Firm • Mkt Prem =Risk Premium Paid on Average Company • = rmkt - rf

Kellogg’s Costs • Debt: Bank Rate: 8.0% • rd = 8.0 * (1-0.34) = 5.28% • Equity: CGM: re = DY + CGY • = 0.90(1.08)/39 + .08 • = .025 + .08 • = 10.5% • CAPM: re = rf + (Mkt Premium) • = 6.00 + 0.73(6) • = 6.00 + 4.38 • = 10.38%

Kellogg’s WACC • BV Weights • WACC = .738*5.28 + .262*10.38 • = 3.90 + 2.72 • = 6.62% • MV Weights • WACC = .149*5.28 + .851*10.38 • = 0.79 + 8.83 • = 9.62%

EFFECTS OF LEVERAGE ON BETA • asset = unlevered = WE* equity • tgt = asset / WE;tgt • port = w11 + w22 + w33

Example: Kelloggs • Target Cap Structure: 25% Debt, 75% Equity • asset = unlevered = (E/V)* equity • = .851 * 0.73 • = .621 • tgt = (V/E)tgt* asset • = (1/.75) * .621 • = 1.33 * .621 • = .828

Example: Kelloggs • re = rf + (Mkt Premium) • = 6.00 + 0.83(6) • = 6.00 + 4.98 • = 10.98% • WACC = .25(5.28) + .75(10.98) • = 1.32 + 8.24 • = 9.56%