Download

1 / 65

670 likes | 755 Views

Learn about TDS provisions, payment coverage, filing returns, effects of tax evasion, and more. Understand the steps for TDS and payment categories. Explore case studies and legal issues related to TDS in India.

E N D

TAX DEDUCTED AT SOURCE CA. SUDHIR BAHETI 12 JUNE 2010

INDEX • Introduction • Payments covered under the scheme of TDS. • Provisions for filing Returns to the Income Tax Department. • Effects of Tax Evasion

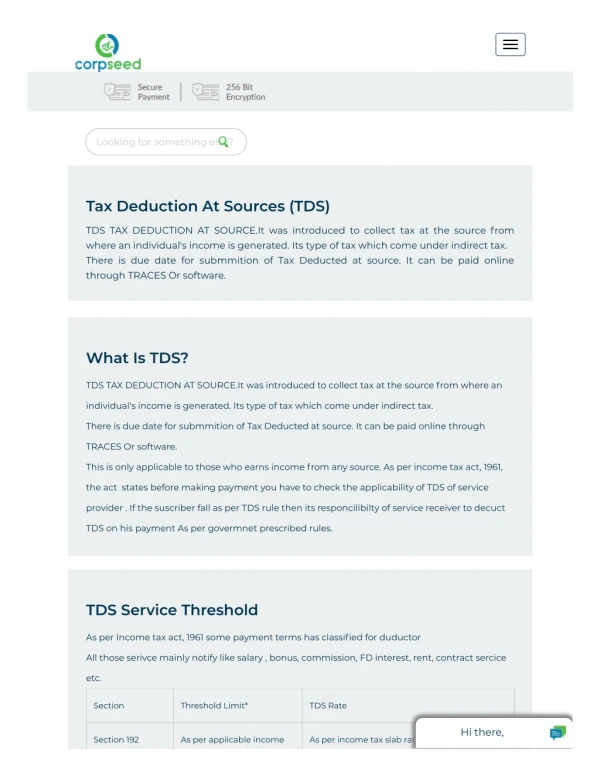

Introduction To avoid cases of tax evasion, the Income-Tax Act has made provisions to collect tax at source on accrual of income. Cases included in the scheme are, generally, those where income can be computed at the time of accrual of income. Under this scheme, persons responsible for making payment of income covered by the scheme are responsible to deduct tax at source and deposit the same to the Government’s treasury within the stipulated time. The recipient of income—though he gets only the net amount (after deduction of tax at source)—is liable to tax on the gross amount and the amount deducted at source is adjusted against his final tax liability. The details of the scheme of tax deduction and collection at source are briefly discussed in this presentation. To conclude one can say that the scheme of TDS is only payment of tax on adhoc basis by the payer of income on behalf of recipient.

TAN Every deductor is required to obtain a unique identification number called TAN (Tax Deduction Account Number) which is a ten digit alpha numeric number. This number has to be quoted by the deductor in every correspondence related to TDS

Tax Deduction & Collection Account Number • Every person deducting tax or collecting tax should obtain a tax deduction & collection number • Such person should quote such number in every challan for payment u/s 200 or 206C(3), in every certificate furnished u/s 203 or u/s 206C(5) • In all the TDS returns delivered • In all other documents pertaining to such transaction as may be prescribed in the interest of revenue.

Payment covered under the scheme of TDS. • Salary (Sec.192) • Interest on Securities (Sec.193) • Dividends (Sec.194) • Interest other than Interest on Securities (Sec.194A) • Winnings from Lotteries or crossword puzzles (Sec.194B) • Winnings from Horse Races (Sec.194BB) • Payments to Contractors and Sub-contractors (Sec.194C) • Insurance Commission (Sec.194D) • Payment to Non-resident sportsmen or sports association (Sec.194E) • Payment in respect of NSC (Sec. 194EE) Contd…

Payment covered under the scheme of TDS. • Payments in respect of Repurchase of units of Mutual Funds or UTI (Sec.194F) • Commission on Sale of Lottery Tickets (Sec.194G) • Commission or Brokerage (Sec.194H) • Rent (Sec.194I) • Fees for Professional or Technical Services (Sec.194J) • Payment of Compensation on acquisition of certain immovable property (Sec.194LA) • Other Sums (Sec.195) • Long term capital gain (Sec.196B) • Income or Long term capital gain from Foreign Currency bonds/Global Depository Receipts (Sec.196C) • Income of Foreign Institutional Investors from Securities (Sec.196D) Contd…

Payment to Non-resident sportsmen or sports association (Sec.194E)

Payments on account of repurchase of units of MutualFunds or UTI(Sec. 194F)

Furnishing of quarterly returns for payment of interest to residents without Deducting Tax (Sec. 206A) Banking company, Cooperative societies, & Public Companies shall furnish quarterly return to department in respect of payments of Interest (other than Interest on Securities) in any computer readable media.

Practical Issues Based on TDS Proceedings

Case Study 1FACTS • An assessee employer is liable to deducted tax at source under section 192. • Deduction of tax of the employees was not uniform during the year; very negligible in the initial months and high amount in the last months. • AO passed order levying interest under section 201(1A) on the grounds that tax was not properly deducted.

Case Study 1ISSUES • Whether the Assessing Officer has rightly levied interest on non-uniformity of TDS deducted? CASE LAWS • Vinsons v. ITO, 89 ITD 267 (Mum) • Grasim Industries Ltd. v. ITO, 92 TTJ 944 (Jodh) • Secy. Board Of Secondary Education, Rajasthan v. ITO, 93 TTJ 256 (Jaipur)

Case Study 2 FACTS • The assessee company (employer) deducted tax under section 192 treating leave travel expense as exempt on the basis of declarations filed by the employee. • The assessee did not obtain any documentary evidence to treat LTA as exempt. • AO passed order under section 201(1) treating ‘assessee in default’ having regard to non-verification of travel payments proof.

Case Study 2ISSUES • Is the AO’s order justified in treating the assessee as ‘assessee in default’ and levy interest u/s 201(1A)? CASE LAWS • DCIT v. HCL Infosystems Ltd. 282 ITR 263 • Savani Financials Ltd. v. ITO, 1 SOT 111 • Lintas India Ltd. v. Ass. CIT, 5 SOT 310 • DCIT v. Excel Industries Ltd., 5 SOT 235

Case Study 3 FACTS • G Ltd is a construction company engaged in the business of construction etc. • At the initiation of the job work, the client provides G Ltd. some interest bearing ‘mobilization and plant advance’, which is to be repaid by the end of the contract along with interest. • G Ltd. submits the running account bills on monthly basis depending on the completion of contract. • Against this the client recovers the principal + interest amount and thus G Ltd. does not actually pay any interest. • Since no direct payment of interest made, NO TDS deducted.

Case Study 3 ISSUES • Is the contention of assessee correct? • Whether tax is required to be deducted at source under section 194A- ‘Interest other than interest on securities’? • What are the other implications of such non-deduction? CASE LAWS • Raymond Limited V. DCIT 86 ITD 791. • Kanchanganga Sea Foods Ltd. v. CIT 265 ITR 644

Case Study 4 FACTS • Assessee engaged in business of imports and/or exports, engages services of Clearing & Forwarding agents. • Payments to such C&F agents comprise of the following: • Reimbursement of freight paid to shipping companies or airlines. • Reimbursement of freight on local transportation. • Reimbursement of import or export clearing expenses like payments to Port Trust, Airport Authorities of India, miscellaneous charges, etc. • Reimbursement of bonded warehousing charges. • Reimbursement of Customs duties and Octroi. • Reimbursement for Crane and Machinery charges to Port Trust etc. • Agency service charges.

Case Study 4ISSUES • Whether any tax is liable to be deducted on any of the above payments to C&F agents? • If the agent has already deducted TDS on freight payment to the Indian Shipping Co., then whether the importer/exporter also needs to deduct tax on the payments made to the agents and if so then on what amount? • When C&F agent deduct tax and pays it to the exchequer, the payment would be on his own TDS account or his clients’ account number? Contd……

Case Study 4CASE LAW • CIT v. Industrial Engineering Projects Pvt. Ltd., 202 ITR 1014 (Del.) • CIT v. Dunlop Rubber Co. Ltd, 142 ITR 493 (Cal.) • Raymond Ltd. 86 ITD 791 (Mum.) • Associated Cement Co. Ltd.(SC) 201 ITR 435

Case Study 5 FACTS • The assessee is a pharmaceutical company, engaged in manufacturing and selling business. • It procures packing material like plastics wrappers, containers, cardboard boxes etc from the vendors (manufacturers) as per assessee’s desired specifications viz. brand name, name & address, designs, trademarks etc. • Similarly, payments are also made to printing and stationary vendors who supply printed letterheads, business cards, sales and other printed literature where the printing is done as per the assessee’s specifications. • Vendor’s charge excise duty and sales tax on such items.

Case Study 5 ISSUES • Whether TDS is required to be deducted under section 194C for payments made as printing charges? CASE LAWS • BDA Ltd. v. ITO (TDS), 281 ITR 99 (Mum.)

Case Study 6 FACTS • G Ltd. is engaged in the business of engineering and construction. • G Ltd enters into execution of construction contracts. • G Ltd has made certain payments for carrying out certain ancillary work undertaken for the purpose of executing the above contracts.

Case Study 6ISSUES • Whether the payments made by G Ltd should be treated as payments for main contract or as sub-contract for deduction of tax at source u/s 194 C? CASE LAWS • Datta Digamber Sahakari Kamgar Sanstha Ltd. V. ACIT 83 ITD 148 (Pune) • ITO V. Rama Nand & Co. And Others 163 ITR 702

Case Study 7 FACTS • Assessee, a Govt. establishment procured milk from various Sanghs etc and sold it in the market through milk centres run by the appointed agents. • Agents sold the goods at the price fixed by the assessee. • Assessee used to reimburse these agents @ Re.0.90 per litre towards transport cost, container cost and chilling charges. • Assessee had given the nomenclature as Commission for such payments. • AO held to deduct tax u/s 194H as payments for commission.

Case Study 7ISSUES • Is the said transaction based on ‘principal-agent’ relationship? • Whether any TDS is required to be deducted u/s 194H? CASE LAWS • Government Milk Scheme v. ACIT [2006] 98 ITD 306

Case Study 8 FACTS • B Ltd is engaged in the business of providing cellular mobile telephone services through its distributors. • It sold SIM and other pre-paid cards at a fixed rate [below market price] to such distributors for ultimate sale to customers. • As agreed, all rights, title, ownership and property rights in such cards would all time vest with B Ltd. • Assessee claimed such price difference as discount allowed and not as commission defined in Expl. u/s 194H • AO treated it as default and levied interest under section 201(1) and 201(1A).