Download

1 / 43

430 likes | 590 Views

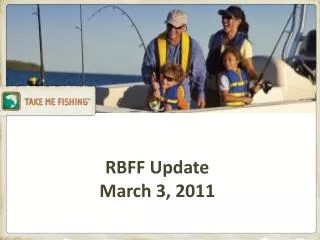

RCM. IFAS Faculty Assembly March 3, 2011. Dr. Joe Joyce Executive Associate Vice President Institute of Food and Agricultural Sciences University of Florida. http://www.hr.ufl.edu/training/rcm/index.html. What is RCM?

E N D

RCM IFAS Faculty AssemblyMarch 3, 2011 Dr. Joe Joyce Executive Associate Vice President Institute of Food and Agricultural Sciences University of Florida

What is RCM? Responsibility Center Management, or RCM, is a budgeting philosophy that decentralizes decisions and financial authority/responsibility to academic leadership – that is, to the college deans and their faculty who are in a position to understand the impact of resource use and related decisions. RCM is designed to encourage academic units to take greater responsibility for revenue generation and spending decisions – promoting “entrepreneurial thinking.” It can also support growth even when government funding is limited.

Other RCM Universities University of Illinois-Urbana Champaign Southern Illinois University Marquette University American University University of California at Los Angeles (UCLA) University of Toledo Clemson University Harvard University Washington University of St. Louis Indiana University of Pennsylvania Mercer University California Institute of Technology (Caltech) Vanderbilt University Duke University Auburn University Clarkson University (considering) Purdue University Temple University University of Oregon University of Pennsylvania University of Southern California University of Toronto West Chester University (PA) Central Michigan University University of Iowa University of Alaska McGill University Rensselaer Polytechnic Institute

How does RCM compare to our current budget model? UF currently uses an incremental budgeting process, which means that central UF administration provides funds to colleges and administrative areas based primarily on historic spending. Central authority for financial planning, execution, and control Budgets based on past allocations Changes are gradual and occur over time as circumstances warrant and resources allow

How does RCM compare to our current budget model? RCM uses a formula to allocate state appropriations based on Student Credit Hours (SCHs), enrollment, and other factors. Colleges/auxiliaries keep surplus funds and all entrepreneurial revenue generated. Instruction: Student Credit Hours Entrepreneurial Activities: Research Self-Funded Classes Auxiliaries, etc. Strategic Direction

With RCM: Deans have more info (increased transparency) and control over their budget Can use limited resources more effectively tosupport priorities Overall effect: Improved outcomes for UF

Let’s define some key concepts as they relate to RCM Colleges, auxiliaries, and certain centers are considered Responsibility Centers (RCs). Responsibility Centers generate revenue and incur costs. The appropriate dean, director, or vice president is accountable for both. Responsibility Center IFAS is a Responsibility Center

Let’s define some key concepts as they relate to RCM Support Centers are administrative units that tend to generate little or no revenue, but do incur costs. Managers of these areas are accountable for costs – and value of services provided. Support Centers will be funded via assessments to each Responsibility Center. Support Center

Let’s define some key concepts as they relate to RCM Each year, Support Centers will explain their value and services to a Budget Review Council to justify their budget requests. This council will be composed of 12 to 15 representatives from colleges, VP areas, and the Faculty Senate, with rotating membership. Every five to six years, each Support Center will go through a “zero-based” budget review in front of this council. Budget Review Council

Let’s define some key concepts as they relate to RCM Certain areas receive funding directly from the state. These Direct-Funded Units are neither Responsibility nor Support Centers. For these units, state-appropriated funds will be provided directly. They will receive their budgets going forward, which will change if they receive new state funding or budget reductions. Direct-Funded Unit

Hybrid: Unit has both Responsibility Center and Support Center functions. Support Center: Unit is an administrative unit that provides support services university-wide. Responsibility Center: Unit earns revenue from student credit hours and/or entrepreneurial activities. Direct Funded Center: Unit is appropriated State Appropriations outside student credit hour model. http://cfo.ufl.edu/rcmc/RCMMatrixDetail.pdf

Key concepts: What are Student Credit Hours (SCHs) and enrollment? Total SCH # of credit hours for classes # of students in classes # of students accepted and enrolled in a college regardless of where they are taking classes Enrollment

Here are some additional key concepts • Five weightings will be used for each college’s SCHs: Lower level, upper level, graduate I, graduate II, and graduate III. • These weightings are based on historical expenditure analysis (FY 09/10) of what it costs to teach classes in each college: • Number of personnel engaged in academic activity and salary cost • Actual state-appropriated expenditures • Number of SCH by level Weighted Cost of Delivery

Key concept: What is weighted cost of delivery? • The process used to determine weighted cost of delivery was non-judgmental, based on historical percentage of university state budget. • However, any funding biases in the past were brought forward since historical data were used. • To control for that, weightings were then compared with other schools: • For example, universities in Ohio, Texas, and other Florida publics. • The weights were then adjusted accordingly.

Here are some additional key concepts • Base Student Allocation refers to the value assigned to one student credit hour (SCH) with a weight of 1.00 – that is, it provides a baseline associated with a 1.0 weighting. • 1 Lower Level SCH = $109.77 (BSA) • BSA is then used to calculate how much of state appropriations the colleges will receive through RCM. • The end result is the allocation of state‑appropriated funds. Base Student Allocation (BSA)

Key concept: What is the Base Student Allocation (BSA)? If your college’s lower level SCH weighting is 10, then, for each lower level SCH, the college will receive state appropriation dollars of $1,097.70.

Here are some additional key concepts With RCM, there also is a strategic fund available that is designed to support new or key initiatives. This central fund is funded by tuition increases as well as the University’s Pepsi fund, logo fund, etc. It is used at the discretion of the President. Strategic Fund

There are five basic components associated with revenue under RCM State Appropriations Entrepreneurial Activities Contracts and Grants Endowment Earnings and Gifts Material & Supply (M&S) and Equipment Use Fees Total College Revenue

Let’s look at these revenue components more closely State Appropriations • Includes: • General Revenue • Lottery • Tuition

State Appropriations – General Revenue and Lottery Per College 70 Percent Based on Student Credit Hours (SCH) 30 Percent Based on Enrollment

State Appropriations – General Revenue and Lottery Goes to College Teaching the Class 70 Percent Based on Student Credit Hours (SCH) 30 Percent Based on Enrollment

State Appropriations – General Revenue and Lottery SCHs are Weighted Based on Cost of Instruction of the Class 70 Percent Based on Student Credit Hours (SCH) 30 Percent Based on Enrollment

State Appropriations – General Revenue and Lottery Based on Number of Students Enrolled in College. Also Weighted 70 Percent Based on Student Credit Hours (SCH) 30 Percent Based on Enrollment

State Appropriations – Tuition Tuition Distribution Per College 70 Percent Based on Student Credit Hours (SCH) 30 Percent Based on Enrollment

State Appropriations – Tuition Goes to College Teaching the Class. SCH Weighted 70 Percent Based on Student Credit Hours (SCH) 30 Percent Based on Enrollment

State Appropriations – Tuition Based on Students Enrolled. Not Weighted 70 Percent Based on Student Credit Hours (SCH) 30 Percent Based on Enrollment

CALS Update RCM, SCH • CALS 09-10 = 123,139 SCH, ~9.3% of UF • Weighted SCH ~ $$ Grad programs generate ~20% of credit hours but >50% of budget

FY 2010-11 RCM SCH Revenues College of Agricultural and Life Sciences

Expected expense components Info Technology General Admin HSC Admin Student Services Admin Facilities Library Sponsored Project Admin Total Assessments

University Support Units Budget for 2011 - $274.6 M

FY 2010-11 Support Unit Overhead Expenditure Rates $9.17/unweighted square foot Facility General Administration 7.39% Information Technology 3.74% Sponsored Projects Administration 8.25%

Space/Facilities Assessments Space Type Weight Lab 2.75 Classroom 1.50 Office 1.25 The current, unweighted cost per square foot is $9.17. For example, if 100 square feet of lab space is being used by an RC, such RC would incur a cost of $2,522 (9.17 x 100 square feet x 2.75 weight). Other 1.25

CALS Budget Base + Salary Savings + Grad Fellowships $7.5 million 95%+ goes to units Grad Fellowships $2.3 million To 22 Graduate Programs Base + Salary Savings Salary Savings $0.3 million To Depts by request & negotiation, for temporary teaching Base Unit Operating $1.5 million Depts ~70% RECs ~30% Base Matching Assistantships $3.0 million Depts ~80% RECs ~20% Base Carry forward CALS Operating $0.4 million Recruiting 15% Stu Travel 5% Comp lab 7% Travel 4% DE 18% Pubs 3% Income, SHARE & Endowments $0.2 million Study Abroad 2% Events, meetings 8% Alumni, Career 15% Awards, grants 18% Other 5%

BOG Minimum Graduate Levels Minimum/Year (5 year Average) Program CALS 6 2 B.S. 4 5 M.S. 3 1 Ph.D.

References • Introduction to Responsibility Center Management (RCM 100 - online course designed and developed by UF Training & Organizational Development in collaboration with the Office of the Vice President and Chief Financial Officer- located at: http://www.hr.ufl.edu/training/rcm/index.html). • Whalen, Edward L. (1991) Responsibility Center Budgeting: An Approach to Decentralized Management for Institutions of Higher Education. Indiana University Press, Bloomington, IN. • UF RCM Manual (TBP). • UF Annual Budget Book (TBP).