Chapter 11 Sales and Purchase

440 likes | 863 Views

Chapter 11 Sales and Purchase. Main Points: 1. Sales 1) Sales Return and Allowance 2) Trade Discount and Sales Discount 2.Purchase 1) Purchases Returns and Allowance Time Allocated: 4 Periods. 1. Learning Objectives. In this chapter the students will learn:

Chapter 11 Sales and Purchase

E N D

Presentation Transcript

Chapter 11 Sales and Purchase Main Points: 1. Sales 1) Sales Return and Allowance 2) Trade Discount and Sales Discount 2.Purchase 1) Purchases Returns and Allowance Time Allocated: 4 Periods 1

Learning Objectives In this chapterthe students will learn: Understand the way that companies earning an income is to buy and sell products and merchandise. Know the meaning of sales return and allowance. Grasp how to record the entry of trade discounting and sales discounting Compare with sales to understand the purchases 2

Revision(1) • 2. For whom are financial statements drawn up? • --- Financial statements are drawn up for private individual, non-profit organizations, retailers, wholesalers, and service industries.

Revision(2) • 1. Why is a work sheet essential? • --- For large companies, if the financial statements are prepared directly from the adjusted trial balance, errors are very difficult to avoid. So, a work sheet is very essential. • 2. Who use financial statements?

Revision(3) • ---Financial statements are used by management, investors, creditors and government regulatory agencies. • 3. What does the income statement show? • ---The income statement shows how much revenues are earned and how much expenses so that you can determine the operating performance of the business over a period of time.

Revision(4) • 4. What does the statement of the owner’s equity show? • ---The statement of the owner’s equity shows the total capital the company owns for a period of time and the investment the owner has made and how much the owner has withdrawn from the company’s account.

Warm-up (1) What? 1. What is revenue? ---Revenue: The increase in owner’s equity resulting from operations during a period of time, usually from the sale of goods or service. 2. What is sales revenue? ---Sales Revenue: Revenue from the delivery of goods and services. 7

Warm-up (2) • 3. What is gross margin? • ---gross margin: The difference between sales revenue and cost of sales. 4. What is expense? • Expense: A decrease in equity resulting from operations during an accounting period; that is, resources used up or

Warm-up (3) • consumed during an accounting period. e.g. wage expense. • 5. What is net income? • ---Net Income: The amount by which total revenues exceed total expenses for an account period: the “bottom line”. In a non profit organization, the surplus.

1. Sales (1) First Reading (para.1,2): Make clear the relationship among Revenue from sales, Cost of goods sold, Gross margin from sales, Operating expenses and Net income.

1.Sales (2) • _ Revenue from sales Cost of goods sold _ Gross margin from sales Operating expenses Net income

1.Sales (3) • (para.3,4,5): • Net sales= Gross proceeds of sales of merchandise – Sales return – Allowances – Sales discount • (Note: only net sales > cost of goods sold + operating expenses, the business can succeed.)

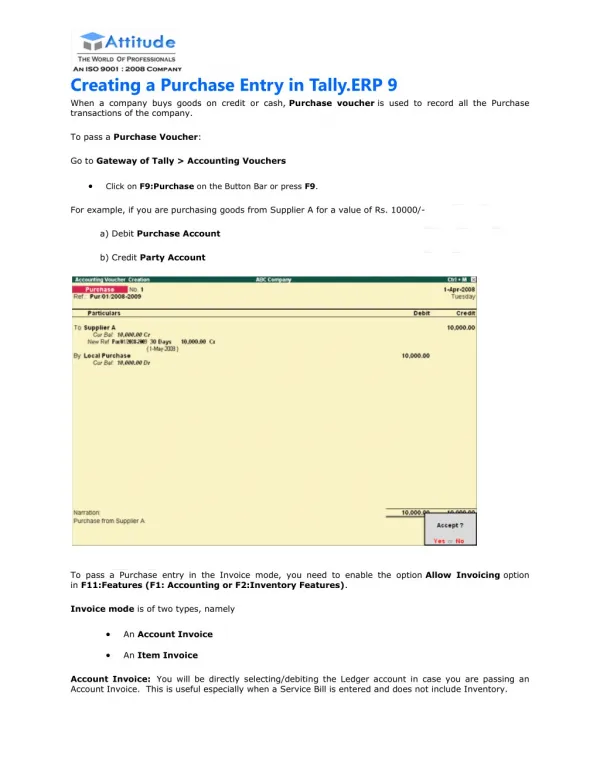

In-class Activities (1) • Suppose the sale is made for cash, the entry is shown as follows: • Dr. Cash $1.000 • Cr. Revenue from sales $1.000 • If on credit, the entry is shown as follows: • Dr. Accounts Receivable $1.000 • Cr. Revenue from sales $1.000

Sales Returns &Allowance (1) • Get the general idea of Sales Returns and Allowance. • Sales Returns and Allowance reflect the dissatisfaction of customers, so a company should provide efficient control of the sales returns and allowance.

Trade Discount & Sales Discount (2) Questions & Answers: • Get the general idea of trade discount and sales discount. • What is trade discount? • --- Trade Discount: In order to get a big sale, a merchandising company usually quotes prices of goods as a discount.

Trade Discount & Sales Discount (2) • What is sales discount? • ---Sales Discount: In order to let the seller pay early, the seller always provides discount to the customer, which can increase the seller’s liquidity. • What do terms of “2/10,1/20,N/30” mean?

Trade Discount & Sales Discount (2) • --2/10: means the customer may take a • 2% discount if the debt is paid within 10 days. • 1/20: means 1% if it is paid within 20 days. • N/30: means that the customer must pay the full amount after 30 days without discount.

In-class Activities (2) • Assume a company sells a computer to a customer on March 4 for $4000, on terms of “2/10, 1/20, N/30”. • 1) How to record the entry? • 2) If the customer paid the amount on March 12, how to record? • 3) If the customer paid the full amount on April 2, how to record?

In-class Activities (2) • Suggested answer: • 1) March 3 • Dr. Accounts Receivable $4,000 • Cr. Revenue from sales $4,000

In-class Activities (2) • 2) March 12 • Dr. Cash $3,200 • Sales Discount 800 • Cr. Accounts Receivable $4,000 • 3) April 2 • Dr. Cash $4,000 • Cr. Accounts Receivable $4,000

Purchases (1) Questions & Answers: 1) Where should the purchases account be used? ---It is only used for merchandise purchased for resale. 2) What’s its purpose? ---To accumulate the total cost of

Purchases (1) merchandise during an accounting period. 3) Should automobile be recorded in it? • ---No, it should be recorded in the appropriate asset account.

Purchases Returns &Allowances (2) • The key points: • 1) It happens when the goods purchased are damaged or unsatisfying. • 2) It is needed to record the allowance. • 3) It is contra account, only used to record the returns and allowance of merchandise.

In-class Activities (3) • Corp. A bought a unit of sweaters for $4,000 on credit from Corp. B. On the delivery day, A found some of the commodities are wetted. B took 20% off the total price as alternative to returning the goods for full credit.

In-class Activities (3) • 1) How to record the entry? • 2) If A bought the sweaters on credit on Sep. 9, on terms of “2/10,1/20,N/30”, A pays the debt on Sep. 29, A only need to pay $3,960. How to record? • 3) If the amount is paid on deadline, how to record?

In-class Activities (3) 1) Dr. Accounts Payable $800 • Cr. Purchases Returns $800 • &Allowances

In-class Activities (3) • 2) • Dr. Accounts payable $4,000 • Cr. Purchases Discount $40 • Cash $3,960 • 3) • Dr. Accounts payable $4,000 • Cr. Cash $4,000

Further Practice • 1.Exercise One at Page 84. • Match the professional terms in Column A with the Chinese explanations in Column B. • 2.Exercise Two at Page 85. • A sales is made on August 1 for $ 400, terms 2/10, n/30, on which a sales return of $100 is granted on August 6. The dollar amount received for payment in full on August 9 is: • a.$400; b.$300; c.$297; d.$392

Further Practice • 1. Answers for Exercise One: • 4/5/8/3/2/1/6/9/11/12/10 2. Answers for Exercise Two: • C.$294 • Calculation: • $400-$100-($400-$100)*2%=$294

Homework 1. Revise Chapter 11 to get further understanding. 2. Finish the exercises three and four on your homework book. 3. Preview Chapter 12.