Natural Monopoly

Natural Monopoly. Natural Monopoly – an industry in which economies of scale are so important that only one firm can survive. In other words, it is more efficient for there to be one firm in the industry. Example: Gas companies (we wouldn’t want multiple gas lines underground).

Natural Monopoly

E N D

Presentation Transcript

Natural Monopoly • Natural Monopoly – an industry in which economies of scale are so important that only one firm can survive. In other words, it is more efficient for there to be one firm in the industry. Example: Gas companies (we wouldn’t want multiple gas lines underground)

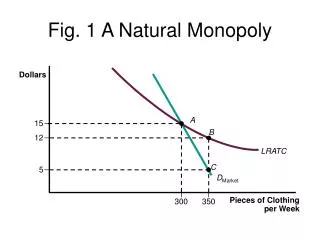

Unregulated Natural Monopoly • An unregulated natural monopoly would attempt to maximize profits by producing the quantity of output where marginal revenue equals marginal cost. • This is the option the profit maximizing firm would choose. • Problem: Huge dead weight loss.

The Profit Maximizing/ Unregulated Monopoly • The company will set the price by going to where • MR =MC • MR – marginal revenue is the additional money brought in by selling one more unit • MC – marginal cost is the additional cost of selling one more unit. • Simply put, if the money brought in is greater than or equal to the additional cost of getting the good or service to the customer, then an exchange will be made.

Deadweight Loss • Producing the profit-maximizing quantity of output causes a deadweight loss. • The deadweight loss is equal to the area between the demand curve and the marginal cost curve for the amount of underproduction.

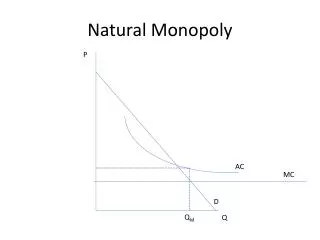

The Optimal Quantity for Society/Pricing Option 2 • The second pricing option in a Natural Monopoly model is to produce the quantity where price equals marginal cost (and thus where marginal social benefit equals marginal social cost). • P = MC • This is the best option for the consumer because the price is low and there is no dead weight loss. • See graph on next slide

Pricing Option 2 P = MC • When price is set where P = MC, notice that the price Popt is below the average cost at that quantity. If average cost is below the price, then the company would lose money. The only way for this company to survive is for the government to subsidize. • Examples: Amtrac, Privately operated transit companies • Often times large cities subsidize their transit system like MARTA in Atlanta, the Subway in NYC, the T in Boston • The subsidy encourages people to use public transportation and reduces pollution.

Regulating Natural Monopoly • If a natural monopoly is regulated to produce the optimal quantity of output, the firm will suffer an economic loss. • To keep the firm operating would require a government subsidy to the firm to eliminate the economic loss.

Zero Economic Profit • To avoid the need for a subsidy, natural monopolies are often regulated to earn zero economic profit (a normal rate of return). This leads to problems: • 1. The natural monopoly lacks incentives to control costs. • 2. The regulators may not be able to obtain accurate information.

The government option P = AC • When the Price is set where the demand curve and the average cost curve intersect it provides a best of both worlds solution. • - the price is lower than it would be if the government left the industry unregulated and the dead weight loss is smaller. • - the government would not have to subsidize the company • - the downfall is that there is no incentive for the company to keep cost low. AC will simply rise and costs will be pushed on to customers.

Theories of Regulation • 1. Public interest theory. This theory holds that regulation serves the public interest. • Assumes that elected officials are always motivated to act in ways that serve the public interest. • A great deal of government regulation does not seem to be serving the public interest.

Theories of Regulation • 2. Capture theory. This theory holds that the regulatory agency will be captured (controlled) by the industry being regulated. • The firms in the regulated industry have a special interest in the policies of the regulatory agency. • Regulations may be used to serve the best interest of the regulated industry.

Theories of Regulation • 3. Public choice theory. This theory holds that regulation serves the best interest of the government regulators. • Regulators would favor a regulatory approach that led to more regulatory power and a growing budget for the regulatory agency.

Costs of Regulation • Regulations impose costs on the economy: • 1. Costs of the regulatory agency. • The costs to operate regulatory agencies are paid by the taxpayers.

Costs of Regulation • 2. Costs to the regulated firms of complying with the regulations. • These costs add to a company’s cost of production and are ultimately paid by the consumers. • See Example 5 on page 29-7.

Costs of Regulation • 3. Inefficiency costs if the regulations reduce competition. • Regulation often reduces competition in the regulated industry. A lack of competition leads to higher prices for consumers. • See Example 6 on page 29-7.

Costs of Regulation • 4. Costs of unintended consequences of regulations. • Regulations intended to accomplish a desirable goal may have unintended consequences that are undesirable. • See Examples 7 and 8 on pp. 29-7 and 29-8.