Comprehensive Guide to CFO Responsibilities: Finance, Tax, and Strategic Planning

This comprehensive guide outlines the critical responsibilities of a CFO in today's corporate environment, focusing on finance planning, reporting, tax management, and strategic operations. It emphasizes the importance of understanding diverse tax responsibilities, including federal and state duties, and the intricacies of international tax planning. Key elements include the management of audit processes, business analysis, cost accounting, and effective negotiations during mergers and acquisitions. Relevant systems and integrated operation strategies are highlighted to ensure robust decision-making and financial health for modern businesses.

Comprehensive Guide to CFO Responsibilities: Finance, Tax, and Strategic Planning

E N D

Presentation Transcript

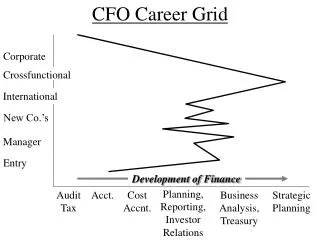

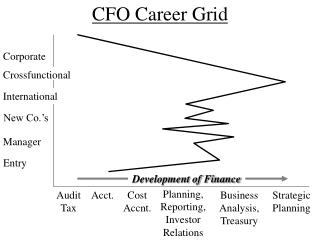

CFO Career Grid Corporate Crossfunctional International New Co.’s Manager Entry Development of Finance Planning, Reporting, Investor Relations Audit Tax Acct. Cost Accnt. Business Analysis, Treasury Strategic Planning

Tax - Responsibilities • Federal • Social Security • Corporate • Sales • State • Sales • Payroll • Audit • Any of the above.

Tax - Personnel • Personnel • Rules & Regs. Specialized/Technical People who make it their career • During Audit Time(s) • Need other Specialists & Best Negotiators to provide support

Tax - Responsibilities • Minimization of Given Tax Payments • Effects of M&A’s • Classification of Assets • Ownership • Depreciation

Tax - Responsibilities • International Planning Function • For at least 4-5 Countries • (or different places with Impacts on Business) • Incentives • Tax-Sheltered Programs

International Tax Planning U.S.GmbHEire 35% 55% 10% Royalties Trademarks Management Fees (Same Scenario w/ States) • State Income Taxes •Property Taxes •Sales Taxes •Corporate Payrolls

Lessons Learned - Tax • Aggressively Challenge IRS • But reserve aggressively as well • Global Businesses demand - World Class Planning • Always include Tax Management in M&A • Planning and Negotiations • At the Beginning & Strategic Level

Operations & Cost Accounting • Highly Competitive Global Economy • Firms that Accurately Measure and Understand their Costs may Survive. Those that Don’t, Will Not.

Operations & Cost Accounting • Controlling Costs & Capital • Raw Materials • Processes • Systems • Capital Budgeting & Returns on Capital -- Productivity

Operations & Cost Accnt. SystemImperatives • CEO & Team Understand Concepts of System • Shared commitment to making them work efficiently. • Timely & Accurate (System) Numbers

Operations & Cost Accnt. SystemImperatives • Integrated Systems One Forecast • Marketing - Updated & Sensitized • Manufacturing as necessary • Distribution, etc… (-bonuses based on the above One Forecast)

Operations & Cost Accnt. Systems • Management from Top to Bottom must Know the Systems • Lower Levels must be trained in the use of the systems and the need for required discipline. • i.e.: Time Lines & Accuracy

Operations & Cost Accnt. Systems Responsibilities: • Sales & Production Forecasts • Procurements • Maintenance of Product Data Records • Info. must be clearly defined & accepted by the members of management • Inventory Levels • Shrinkage, Obsolescence

Operations & Cost Accnt. Systems • Assigned to Specific Management Fxns. • Computer Based Systems • Updated on a Daily Basis • For Key Items: Manufactured, Used, or Purchased • Constant Training & Retraining • Accountability for Training

Operations & Cost Accnt. Systems • Manufacturing/Inventory Planning Systems • Must be Soundly Conceived • Integrated with: • Financial/Cost Accounting Systems

Operations & Cost Accounting Capital Appropriation Needs: • Climate in which Innovation Flourishes • Acceptable method for Evaluation of Proposals • Expenditures on a project to be Controlled & Periodically Reviewed • Planned Post-Audit Program • Shared Lessons Learned

Operations & Cost Accounting Budgeting & Financial Models • Capital Expenditures • Cost of Capital • Capital Rationing • i.e.: Strategically Important Projects • NPV & EVA

Analysis Methods • Breakeven Point • Cost/Volume • Variance

Break-Even Point • B.E.P. = Sales Revenue that Equals the Total Variable and Fixed Costs for a Given Volume at a Particular Capacity Utilization. • BEP units = Fixed Costs Unit Contribution • BEP dollars = Fixed Costs Contribution Margin

Cost-Volume-Profit Analysis $ Contribution Profit B.E.P. Fixed Costs Loss Units

Contribution Analysis • Contribution = Excess of Sale(s) over the Variable Costs or the Amount of Money Available to Cover Fixed Costs & Generate Profit.

Variance Analysis • Ability to Analyze & Explain The Casual Factors Behind Changes in Profits.

Variance Analysis • Volume Variance Variance = = (100 units – 110 units) * $4 = ($ 40) -- Unfavorable due to Fewer Units Actual Quantity Standard Quantity Standard Profit Per Unit _ *

Variance Analysis • Price/Cost Variance Variance = = 110 units * ($9.5/unit - $10/unit) = $ 55 -- Favorable if Price Unfavorable if Cost Actual Quantity Actual Price/Cost Standard Price/Cost _ *

Earnings Variance Analysis Good Volume Offset by Lower Price Levels and Higher Unit Costs

Operations & Cost AccountingNeed to Account for & Manage: • Overhead • Payroll, Benefits, etc… • Absorption • Sunk • Fixed • Semi-Variable • Influenced • Affects of every addition Costs

Operations & Cost Accounting Manage By: • Standard Cost Accounting • Std’s, Budgets, Variances • Inventory Valuation and Control • Avg., Std., LIFO, FIFO, Cost Specific LOT

Operations & Cost AccountingManage By: • Budgeting • Cycles • Annual are the most effective • Gamesmanship • Under promise, Over deliver • Allocations • Know their Influences

Lessons Learned - Restructuring • Bite the Bullet, for everyone’s sake • Cut Once and Cut Deep • Collapse Layers • Keep it Secret • Do it Quickly • Do All that You Can for Employees • Continue Recruiting

L.L. – Restructuring II • Empower People – Increase Span of Control • Over Communicate, At All Levels • Be Humble, Be Honest • For People and Markets: “Cutting Losses Rather Than Hoping for Rebounds.” “Hope is Not a Strategy”