Download

1 / 10

100 likes | 245 Views

Activity-based job costing. Opgave 11.16. Opgave 11.16 (deel 1).

E N D

Activity-based job costing Opgave 11.16

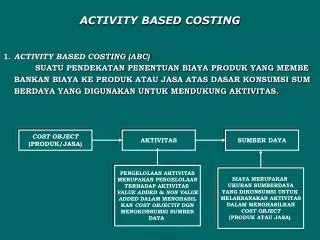

Opgave 11.16 (deel 1) Baden-Möbel GmbH produceert een aantal verschillende stoelen. Hun job-costing system is ontworpen vanuit een standpunt dat kijkt welke activiteiten er plaats vinden binnen het bedrijf. Er zijn twee direct-cost categoriën (direct materials en direct manufacturing labour en drie indirect-cost pools. Deze 3 cost pools geven de 3 handelingen op de fabriek weer

Opgave 11.16 (deel 2) Er zijn twee soorten stoelen geproduceerd in Maart, the executive stoel en de chairman stoel. Hun hoeveelheden, direct material costs en andere gegevens voor Maart 2002 zijn als volgt: De direct manufacturing labour waarde is €2 per uur. Neem aan dat er geen begin- of eindvoorraad is.

Vraag 1: Bereken de totale productiekosten, alsmede kosten per eenheid over Maart 2002 voor de directeursstoel en de vorzitters stoel.

De totale manufacturing costs worden berekend door de direct material costs, de parts costs en de direct manufacturing labour costs bij elkaar op te tellen. De direct material costs zijn al gegeven:

De parts costs worden als volgt berekend: Totale indirecte manufacturingkosten bedragen:Executive chair: Dkr 462.500Chairman chair: Dkr 22.125

Nu alleen de direct manufacturing costs nog berekenen: Totale directe manufacturing kosten:Executive chair: Dkr 750.000Chairman chair: Dkr 10,000

Oplossing vraag 1: Nu kunnen we al deze kosten bij elkaar optellen: Totale productiekosten:Executive chair: 750.000 + 462.500 = Dkr 1.212.500Chairman chair: 35.000 + 22.125 = Dkr 57.125Kosten per stoel (unit costs):Executive chair: 1.212.500 / 5000 stoelen =Dkr 242,5Chaiman chair: 57.125 ? 100 stoelen = Dkr 571,25

Vraag 2: Veronderstel dat de upstream activities (R&D en design) en de downstream activities (marketing, distribution en customer service) om de produkten te produceren berekend zijn. De unit costs in 2002 waren als volgt: Bereken de totale produktie kosten per unit van elke stoel. (De totale produktie kosten zijn de som van de kosten in alle business function areas)

Oplossing vraag 2: Je moet de upstream activities, de downstream activities en de unit costs uit vraag 1 bij elkaar optellen: