Silver linings in dark clouds

160 likes | 364 Views

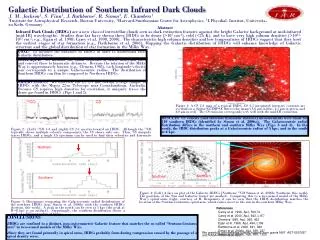

Silver linings in dark clouds. James McCann RBS Group Economics May 2013. Great Depression. 2008 onwards. Depressing times!. UK national income during and after recessions (Pre-recession peak level = 100). 125. 120. Average UK recession. 115. 110. 105. 100. 95. 90. 0. 1. 2. 3.

Silver linings in dark clouds

E N D

Presentation Transcript

Silver linings in dark clouds James McCann RBS Group Economics May 2013

Great Depression 2008 onwards Depressing times! UK national income during and after recessions (Pre-recession peak level = 100) 125 120 Average UK recession 115 110 105 100 95 90 0 1 2 3 4 5 6 7 8 Years since pre-recession peak in national income Source: National Statistics and Group Economics Calculations

Traditional export markets struggling Export growth 2012 (%y/y) 6 4 2 0 -2 -4 -6 -8 -10 -12 Total Eurozone Spain Germany Non-EU USA China Source: National Statistics

Money’s too tight to mention UK household debt-to-income ratio (%) Source: National Statistics and Group Economics Calculations

How much “austerity” to go in the UK? Tax increases Investment cuts Benefit cuts Day-to-day spending Total Start Finish How much of scheduled austerity completed at end of 2012-13

Okun’s law broken? Relationship between unemployment and growth in the UK 10% -3% GDP growth Unemployment rising 8% -2% 6% -1% 4% 0% 2% 1% 0% 2% -2% 3% -4% %y/y GDP growth (4 quarter ma, LHS) 12m Change in unemployment rate (RHS) -6% 4% Q1 1971 Q1 1981 Q1 1991 Q1 2001 Q1 2011 Source: National Statistics and Group Economics Calculations

What’s going on?? UK productivity (100 = Q1 2000) Source: National Statistics and Group Economics Calculations

What “should” have happened? Actual employment and employment under constant productivity assumptions 30,000,000 29,500,000 29,000,000 28,500,000 28,000,000 27,500,000 Employment Constant productivity employment 27,000,000 26,500,000 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2008 2009 2010 2011 2012 Source: National Statistics and Group Economics Calculations

What has been driving the unemployment rate? The UK labour market story so far (changes in the number of people (thousands) between Q1 2008 and Q4 2012 Source: National Statistics and Group Economics Calculations

Where has job creation been strongest? Change in employment by sector (2010-2012) Source: National Statistics and Group Economics Calculations

1. Real wages are falling Real average employee compensation and the unemployment rate Source: National Statistics and Group Economics Calculations

2. Firms substituting labour for capital Net lending/GDP (inverted scale) and the unemployment rate Source: National Statistics and Group Economics Calculations

3. Firms hoarding workers Business confidence (inverted scale) and the unemployment rate Source: National Statistics and Group Economics Calculations

What does this mean for the future? Unemployment forecast Source: National Statistics and Group Economics Calculations

Thank you and keep in touch! Internet www.rbs.com/economics E-mail www.rbs.com/economics/registration Social media @rbs_economics

A word from our lawyers This material is published by The Royal Bank of Scotland plc (“RBS”) which is authorised and regulated by the Financial Services Authority for the conduct of regulated activities in the UK. It has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments, other financial instruments or related derivatives (“Securities”). It should not be reproduced or disclosed to any other person, without our prior consent. This material is not intended for distribution in any jurisdiction in which its distribution would be prohibited. Whilst this information is believed to be reliable, it has not been independently verified by RBS and RBS makes no representation, express or implied, nor does it accept any responsibility or liability of any kind, with regard to the accuracy or completeness of this information. Unless otherwise stated, any views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the RBS Group’s Group Economics Department, as of the date of publication of this material and are subject to change without notice. Recipients of this material should make their own independent evaluation of this information and make such other investigations as they consider necessary (including obtaining independent financial advice), before acting in reliance on this information. This material should not be regarded as providing any specific advice. RBS accepts no obligation to provide any advice or recommendations in respect of the information contained in this material and accepts no fiduciary duties to the recipient in relation to this information.