Download

1 / 0

10 likes | 164 Views

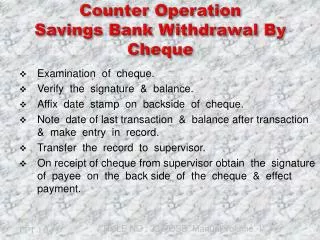

Cheque system in PO Savings Bank. Introduction. PO Savings bank transacts in cheques for Acceptance of cheques for opening of accounts or investment in certificates Subsequent deposits in accounts Allowing withdrawals from cheque accounts Stocks and issues cheque books to depositors.

E N D