Download

1 / 8

80 likes | 191 Views

This article delves into the theory of portfolio optimization, focusing on the concept of the Efficient Frontier. It explains how investors can achieve optimal returns relative to risk through diversification. The Efficient Frontier illustrates the set of optimal portfolios producing the highest returns for a given level of risk. Key equations, such as the Security Market Line and Beta calculations, are discussed alongside practical examples to illustrate the application of these concepts using simulation and optimization techniques.

E N D

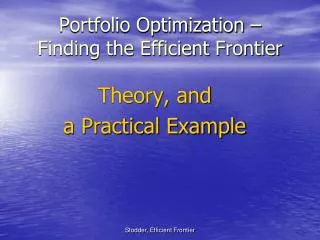

Portfolio Optimization – Finding the Efficient Frontier Theory, and a Practical Example Stodder, Efficient Frontier

Concept of Beta Stodder, Efficient Frontier

Source: Value Line, March 2005 Stodder, Efficient Frontier

Security Market Line Equation Required Return=Risk Free + Risk Premium on Stock iRate on Stock i Required Return=Risk Free + βi(Market Risk) on Stock iRate Premium Ri = Rrf + βi(Rm - Rrf) Stodder, Efficient Frontier

Beta of the Market = 1 βi= (Ri– Rrf)/(Rm - Rrf) So if Ri = Rm, βi = βm then βm = (Rm– Rrf)/(Rm - Rrf) = 1 Stodder, Efficient Frontier

The Efficient Frontier Non-Diversifiable Risk Stodder, Efficient Frontier

How do We Find the Efficient Frontier? Basic Strategy: • Find the Standard Deviation(σi) and Mean Return(μi) of every stock Stock i. • For any given rate of return, find the minimal standard deviation portfolio that can achieve that return. Stodder, Efficient Frontier

Run Simulation • From Financial Models Using Simulation and Optimization by Wayne Winston: Ch. 16, “Portfolio Optimization” Stodder, Efficient Frontier