Download

1 / 65

650 likes | 872 Views

Recruitment Ready. General Finance Interviews. Outline. General Interview Tips Resources Most Common Mistakes Interview Etiquette Common Questions Behavioural Questions Employer Questions Understanding the Job Basic Technical Questions Capital Structure Valuation methodologies

E N D

Recruitment Ready General Finance Interviews

Outline • General Interview Tips • Resources • Most Common Mistakes • Interview Etiquette • Common Questions • BehaviouralQuestions • Employer Questions • Understanding the Job • Basic Technical Questions • Capital Structure • Valuation methodologies • Accounting • Other Questions • Summer 2014 Student Recruiting Experiences

General Tips Practice, Practice, Practice!

Resources • Career services • Danielle Dagenais(Finance, Investment Banking, Investment Management) • Offers help with • Resume & Cover Letter • Job Opportunities • Preparation for interviews and mock interviews • Evaluation of internship and job offers • McGill Investment Club workshops • Prep Documents • Breaking into Wall Street • Mergers & Inquisitions • Vault guide • Queen’s Commerce Prep Guide • BCom Career Handbook • Myself Use the resources available to you!

How to Make a Good Impression • Dress for the job • Be on time! Actually, be 10 min early! • If there are other candidates, receptionists, talk to them • Keep your cell phone off at all times • Offer a strong firm handshake and follow person to room with conviction • Look in the eyesand sit fully erect • Smileand use your hands to emphasize the points you are making • Do not fidget, scratch… • Beware of excess familiarity but mirror your interviewer

Must Do’s in an Interview • Ask for a business card at the end if not given • When asked “do you have any questions”, absolutely ask some! • Prepare 3-4 questions you could ask to any interviewer that are not generic • Don’t ask about the salary • It is ok to ask about the next steps in the process • Thank them twice at the end (for the opportunity and for taking their time) • Again, send a follow-up/thank you note • Make sure you can easily be reached after the interview and be ready for calls at random hours

Prepare for Fit Questions • Your story • Happy and sappyexperiences • Structures • Practice – BCom CareerHandbook • Practice live

Walk me through your CV? • Tell me about yourself? • Whyshould I pickyou? • Tell me about yourexperience? • Whatshould I know about you? • Whatwouldmakeyou a good XYZ? • Whatbringsyouhere? • Be chronological • Show how each experience along the way led you in the direction of finance • State why you’re here interviewing today (important to land the question) • Aim for 2-3 minutes max

Key Experiences • Happy: • What are yourstrengths ? • Whendidyoudemonstrate leadership? • Tell me about this part of yourresume? • How do youhandleconflict? • Sappy: • Whatisyourgreatestweakness? Anyother? • Tell me about somethingyouwould do differently? • Whatisyourgreatestfailure? • Tell me about a time you failed to honour a commitment

Variants • Variants of strengths and weaknesses question: • What kind of feedback did you receive in your internship last summer? • If your friends could describe you in 3 words, which ones would they choose? • If I talk to somebody who doesn’t like you, what would they say about you? • Why would we NOT hire you today? • In 3 sentences why would we hire you? • 1st sentence: School • 2nd sentence: Previous relevant experience • 3rd sentence: Something that makes you unique

Personal Questions • Where do you see yourself in 5 years? • OK to say that you are not sure and that it is not prudent to make predictions now, especially given the fact that you have never tried the job • However, make sure to say that given what you know now, this is what you think you are best fitted for and where you can contribute the most as an individual • What do you do for fun? • Bankers will spend 80-100 hours/week with you in the office. They want to know if they can spend some time with you talking about other things than finance • In this case, the worst possible answer would be “I love reading the WSJ and researching stocks” • Don’t necessarily have to be very original, but show that there is more to you than good grades and a passion for finance

Personal Questions • Why do you want to work in Toronto? • Again, given that finance has high employee turnover rates, it is important for banks to now that you are committed to stay with the office • This is especially true for regional offices like Montreal and Calgary from where a lot of people want to transfer to Toronto or New York • Tell me something interesting about you that’s not listed on your resume • It’s a difficult question that can be surprising given that we usually put most of what is interesting about us on our resumes • Here, it is important to be somewhat original and show that there is something unique about you • It doesn’t have to be an interest, it can be a special story or event • Nothing illegal! Nothing related to sex, religion or politics.

Employer Questions • Why do you want to work for XXX? • Extremely important to be able to back up arguments! Everybody will say “You have an amazing culture”, but how do you show that this is true? • Typically, you need to talk to professionals or fellow students who have worked there to get a sense of what it’s like • Be able to talk about the bank’s strengths and recent important deals • Where else are you interviewing? • If you’re interviewing for an IB position, say that you are interviewing only for IB at other banks too (shows that you are convinced this career is right for you) • Often times, banks will feel more rushed to give you an offer if they know you have attracted attention from competitors, but don’t be too cocky about it! • Don’t lie about it, they can check very easily

Employer Questions • Why do you want to work in Montreal? It’s a regional office with a very small team • Working in a small office has a lot of advantages! • If you are good, people will give you more work and trust you with more challenging tasks earlier on • Senior people are much more approachable • You can work on a lot of different kinds of projects • More opportunities to attend client meetings and have direct exposure to the job • Why do you want to work in metals and mining? There is hardly any activity these days • Highlight your long-term view and cyclical nature of this industry and capital markets • Once activity picks up, there will be a vacuum for human capital and more opportunities

Employer Questions • What do you think is our biggest weakness / which of our competitors do you admire most? • Important to do your research beforehand! • Saying something like being “weaker in some geographic region” or “lacking experience in a given industry” is acceptable to say, but indicate how it doesn’t really matter because they are really strong in something else • Always talk with respect about competitors! • Who is our CEO? • Absolutely crucial to know and makes you look very bad if you can’t answer

Understanding the Job • Why do you want to do Investment Banking? • Everyone should have a personalized answer and his own reasons why they want to do it. You want to sound credible and passionate about this job • Worst possible answer here is to say “I’m not sure” or “for the money” • Common answers include: “I want to be pushed to my limits”, “I want to work with the smartest people” and “Investment Banking will teach me a lot”

Understanding the Job • What will you actually be doing as an intern? • As an investment banker summer analyst, you cannot expect to be making models and other fancy stuff • It is important to recognize that you will spend most of your time working on pitch books and researching companies/industries • However, even if the tasks appear simple, you should also recognize that you will actually be exposed to a ton of very smart people and that you will learn a great amount about the industry • What is a pitch book? • Sales tool of the investment bank. There are three main types: • Market Overview / Bank Introduction • Deal Pitches (M&A, IPO, debt issuance, etc.) • Management Presentations

Understanding the Job • How much do you expect to work in a typical work week? • As an investment banking summer analyst, you will probably spend anywhere between 80 and 100 hours per week in the office • This is true for the analyst level, but the hours do get better as you progress towards associate and VP • How do companies select the bankers they want to work with? • Everything in finance has to do with relationships, and this is especially true in investment banking • Typically, all the banks will pitch to the company in what is called a “beauty pageant contest” • You are asked to summarize a company on one slide with four quadrants • This question tests your ability to summarize the most important facts about a company in a restricted space. Typically, you would probably include some valuation metrics, a company description, share performance chart and summary of management

Recruitment Ready Technicals - Basics

Outline • Corporate Structure • Valuation • DCF • Comparable Company Analysis • Precedent Transactions • Accounting

Corporate Structure • Secured Debt • Underfunded Pension • Operating Leases • Unsecured Debt • Convertible Debt • Preferred Shares • Equity Seniority

Optimal Capital Structure • The advantage of debt is that it gives tax shields to the company through the interest paid • It would NOT be optimal for the firm to add on 100% debt as bankruptcy costs eventually become more important than the benefits derived from tax shields

Enterprise Value Enterprise Value = Market Capitalization + Debt + Minority Interest + Preferred Equity - Cash + Underfunded Pension + Capital and Operating Leases + Contingent Liabilities + Long-term Provisions + Tax Liabilities - Short-term Investments

Capital Structure Questions • Why do you subtract cash from EV? Is it always accurate? • Should you use the book value or market value of each item when calculating EV? • Why do we look at both Enterprise Value and Equity Value? • What’s the difference between Equity Value and Shareholder’s Equity? • Should cost of equity be higher for a $1B or $100B company? • Same question for WACC?

“Value determined by calculating the present value of a stream of projected cash flows over a certain period and a terminal value” Discounted Cash Flow - Principles • Projected after-tax unlevered free cash flows • Forecast period should be long enough so that business reaches a steady state by the end of period and incorporates a cycle (if a cyclical industry) • Typically 5 to 10 years • Terminal value • Value of perpetual cash flows following end of forecast • Terminal year should best mirror company's normalized future steady state • Discount rate • Weighted average cost of capital (“WACC”) • Depends on capital structure (typically weighted average cost of equity and debt) • WACC should reflect optimal and sustainable capital structure and underlying estimate of business risk

“Determining the terminal value involves the application of one of the following going concern approaches” Discounted Cash Flow – Terminal Value Practice Considerations • Based upon current trading multiples ~ multiples of EBITDA • Based upon multiples paid in comparable company transactions • Industry or company considerations may make the current environment not comparable to the terminal year • Implies a perpetual growth rate from the terminal point onward Comparable Trading / Transaction Multiple • Single stage – constant growth perpetuity • Unlevered Free Cash Flow * (1+ Perpetual Growth Rate) / (WACC – Perpetual Growth Rate) • 2 stage – growth rate 1 for n years followed by growth rate 2 • Ideal when company is in steady state • Very sensitive to changes in inputs, especially perpetual growth rate assumptions • Implies multiples as if the business was transacted in the terminal year Perpetual Growth

Strengths Limitations Discount Cash Flow • Based on well accepted corporate finance theory • Flexibility to handle different patterns of cash inflows and outflows • Recognizes time value of money • Allows explicit consideration of project risks • Focuses on future operations • False perception attributed to sophisticated technique due to inherent subjectivity in forecast, terminal value and WACC • Demands extensive set of forecast data and related due diligence • Sensitive to long term growth assumptions • Lacks external reference to reconcile valuation differences

Enterprise Value Equity Value Comparable Company Analysis (‘’Comps’’) • Comparable trading analysis: Key Valuation Metrics / Multiples • What is comparable company analysis? • Provides a market-based valuation perspective on comparable publicly traded companies • It is based on publicly available information; reflects what the many independent investors that comprise the market think • Implied valuation does not reflect premium for control or any synergy potential • Effectiveness of this valuation method depends on the comparability of the companies selected and metrics used to compare the companies • Revenues • EBITDA • Unlevered Cash Flow • Earnings • Levered Cash Flow • Book Value Multiples based on economics that all stakeholders are entitled to (debtholders and shareholders) Multiples based on economics that only shareholders are entitled to

Comparable Trading Analysis Less affected and easier to interpret when there are capital structure differences Permits the use of statistics less affected by accounting policy variations General Preference for Enterprise Value / EBITDA Multiples… More comprehensive – focuses on the business and not just the equity investor’s stake More flexible – can be modified to exclude non-core assets

Select the right peer group • Focus on the appropriate financial metric and ratios: each sector utilizes a standard set of ratios/metrics • Make the necessary adjustments to ensure comparability (non-recurring items, accounting policies, M&A activity) Making a comps table Value Drivers Illustrative Considerations • Market / Product leadership • Client-base & supply chain • Technology & patent • Market presence, operating “leverage” • Good proxy for risk • Cost structure • Margin analysis • Consistency • Financial leverage • Quality of management • Non-recurring items • Different accounting practices • Sales, EBITDA, earnings • Consistency of growth / volatility • Growth potential Relative Risk Profile Strategic Positioning Size Profitability Capital Structure Others Relative Growth Growth Profile

Strengths Limitations Comparable Trading Analysis • Objective comparison reflecting all publicly available information on the overall sector and the individual companies • Growth / profitability expectations • Sector trends • Risk factors • Often provides a reliable, useful first order approximation of value • May be forward looking, and can also be backward looking • Ease of understanding and application • Requires fewer assumptions (e.g. Discount rates) • Standard practice when valuing emerging companies, as forecasting cash flows is difficult • Challenge of finding true “comparability” within peer groups • Very difficult to adjust for differences in underlying business of comps • Company specific issues may limit analysis and effectiveness (e.g. limited liquidity) • Other external factors may impact share price performance • Market sentiment, M&A activity in the sector and regulatory issues • Analysis is focused on trailing date and on next 1-2 years, thus ignoring future performance and long-term issues • Assumes market prices of comparable companies correctly reflect all available information

Valuation based upon applying observed financial and operating metrics from comparable transactions • Provides useful information on valuation multiples that acq • Provides indication of private market value • Value of consideration that willing buyers and sellers are prepared to exchange in current economic environment • Many considerations discussed in Comparable Trading Analysis section apply, however three specific nuances to this methodology must be addressed Precedent Transactions Analysis Considerations • Comparability of precedent deals and the acquired companies • Was the deal completed under comparable economic conditions • Is the other consideration comparable (cash vs. stock)? • Eliminate all deals that are too small or too large compared to the potential transaction • Look at relative size of acquirer versus target • Only include deals where sufficient / reliable information is available • Private deals: if no public data is available, do not use in deal comparison • Timing: the more recent the data, the more relevant the benchmark • Auction / Interlopers: competition for the assets drives valuation up Relevance Size Information Type of Deal

Strengths Limitations Precedent Transactions Analysis • Based on public information • Reflects different premium at which transactions have been completed in the past (important to isolate impact of economic cycles) • Overview of potential interlopers based on historical behaviour and their strategic approach to M&A • Ease of understanding and calculation • Commonly used yardstick / rule of thumb • Relevance deteriorates over time • Important not to miss context for the premium paid in different transactions to avoid drawing misleading conclusions. • Financial versus strategic investor; • Governance issues, commercial agreements, etc.; • Asset competition driving up prices; and • Distressed sales. • Important to distinguish what kind of assets were traded in order to achieve like-for-like comparisons. • Market conditions at the time of a transaction can have substantial influence on valuation (ie. Sector consolidation) • Challenge of true “comparability”

DCF • What is the purpose of a Discounted Cash Flow analysis? • Obtain intrinsic value of company by forecasting free cash flows 5 to 10 years into the future, discounting them and the terminal value to today

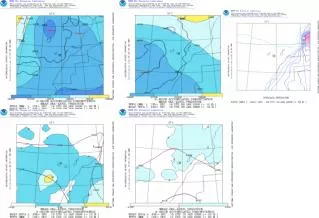

Sensitivity Analyses WACC / Capital Expenditures WACC / Operating Margins WACC / Intermodal Growth WACC / Long-Term Growth