Download

1 / 21

210 likes | 322 Views

The Price-to-Earnings (P/E) ratio is a crucial metric used by investors to evaluate the potential return on their investments. It indicates the number of years it would take for an investment to recoup its cost through earnings. This article explores the P/E ratio's calculation from share price and earnings per share (EPS), exemplified by Infosys Technologies. We discuss the comparative analysis of investing in stocks versus bank deposits, highlighting the risks and returns associated with each option. Discover how P/E ratios can guide smart investment choices for better future gains.

E N D

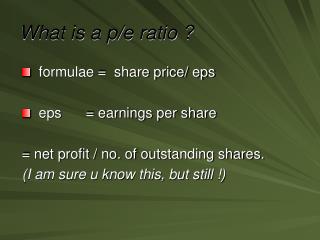

What is a p/e ratio ? formulae = share price/ eps eps = earnings per share = net profit / no. of outstanding shares. (I am sure u know this, but still !)

What does it say? • It tells me the number of years a company would take to return me my capital investment as profits. Which means assuming the share price remains constant throughout the holding period, how much time will the co. take to double my investment.

for example: • Infosys Technologies • Net profit – Rs.150 • No. of shares – 3 • EPS – Rs.50 • CMP - Rs.1,500 • p/e - 30 Now if Mr. John were to buy one of the three shares, the other two being Bon and Tom. Note – there are no other shareholders. Which means all the profit will be shared by John, Bon and Tom. Right ? Yep.

for example:…..cont • What is the return on capital employed for Mr.John ? ROCE = (50/1500) = 3.33 % • Not a good investment by any measure, is it? Bank deposits yield = 5.5 % • p/e ratio for bank deposits can be calculated as – • Investment – Rs.100 • Interest earned annually – Rs.5.5 • p/e ratio – 100 / 5.5 = 18.2 Similarly p/e ratio can be calculated for bonds, or for that matter any investment.

Two questions should emerge in your mind, viz. • One, When bank deposit is at a p/e of 18.2 and that of Infosys Technologies is at 30, where should one invest ? The obvious answer – YES, the bank deposit is a better option. • The most important reason being the ‘zero risk’ associated with banks or sovereign bonds compared to an Infy. • Also because the bank deposit yields more than Infy, 5.5% v/s 3.3 %. This also implies that money invested in the bank deposit would double in 13.1 years as opposed to 22 years taken by an investment in Infy.(Remember ‘rule of 72’. If not then – it says that the number of years taken by any investment to double is equal to (72 / rate of interest) …..cont

Answer to question no.1 – Any rationale investor ‘would not’ put his money in an investment that is not only riskier than a bank or a govt. but also gives him a lower return on investment.

Questions…cont. • Two, why do then people invest in Infosys and not in bank deposits ? Well, this is because Infosys by virtue of being a business has the potential to increase its profits, and therefore its earnings per share, therefore its yield for its investors (John, Bon and Tom in this case). As we all know the same is not the case for a bank or a govt. bond, right? And there in lies, the reason for people investing in stocks such as Infosys (which have high p/e and not with the ‘no-risk’ bank deposit or sovereign bonds.

What does this potential mean for you and me as investors? • Recall the earlier numbers for Infy, (YEAR I) - • Net profit – Rs.150 • No. of shares – 3 • EPS – Rs.50 • Share price - Rs.1,500 • p/e ratio – 30 • Now assume that Infosys records a 100 per cent jump in its net profit the following year. (YEAR II) • Net profit - Rs.300 • No. of shares - 3 • EPS - Rs.100 • Share price - Rs.1,500 • p/e ratio - 15

Looking at the Infosys share in the second year makes it a better investment than the bank deposit, because not only does your ROCE improve from 3.3% to 6.7%, your investment will now double in 10.8 years (compared to 22 years earlier) and better than bank deposit (13 years and ROCE of 5.5 %).

Year III for Infy (PAT up 100%) • The numbers would now look something like this – • Net profit - Rs.600 • No. of shares - 3 • EPS - Rs.200 • Share price - Rs.1,500 • p/e ratio - 7.5 • ROCE - 200 / 1500 = 13.3 % • Years to doubling of inv. - 72 / 13.3 = 5.4 years. John, Bon and Tom now have every reason to stay invested in Infy forever. Even if it doesn’t grow from here they will be happier doubling their investments every 5.4 years. Isn't it ?

All this while we’ve assumed that the share price remains the same, i.e. the initial investment made by John, Bon and Tom. John suddenly wanted to opt out of Infy because of some personal reasons so he decides to auction his share in Infy on www.xyztrading.com. How many people do you think will be willing to pay him Rs.1,500. My guess is every person on this earth. But John will sell it to only one person. So demand outstrips supply by a zillion, resulting in people bidding up the share price. To what extent would people bid it up……on next slide.

The bidding would ideally continue till the point the ROCE is better than one from the bank deposit (plus some risk premium associated with a co.) In this case it should be around Rs.2,500 per share. ROCE = 8%, which is still better than the bank deposit. So we have people bidding for infy share at 8% return…some people may even be happier by getting 7% return…and may drive up the Infy price even higher. But we assume that the max. bid came in at Rs.2,500 per share. Remember the EPS in the third year is Rs.200 per share, hence the ROCE at 8% for a share price of Rs.2,500.

Enter Ms. Fiona, a security analyst with www.xyztrading.com. According to her calculations Infy will post a 100 per cent rise in net profit in year IV. The estimated calculations – (YEAR IV) • Net Profit - Rs.1200 • No. of shares - 3 • EPS - Rs.400 • CMP - Rs.2,500 • ROCE - 16 % • Eureka, eureka !! Immediately she believes she’s got a great investment in Infy. One which will yield (16 % return per annum, compared to 5.5 per cent by bank deposit) and one which will double her money in a mere 4.5 years.

But there’s a problem. Both Bon and Tom would not sell their share in the business (remember we’ve only three shares in this company). But the last buyer, who bought from John, Mr. Adam Smith may, however, be willing to sell his share, provided he gets a better share price. Ms. Fiona after thinking hard suggests a price of Rs.3,200 per share, 28 % premium to what Mr. Smith had paid to John. But, Mr. Adam Smith being a smart economist, does his calculations and reverts to Miss Fiona with an ask price of Rs.4,000. Miss Fiona gets back to her numbers and feels Infy at Rs.4,000 may still be a good investment, yielding 10 % per annum. Given the present low interest rate regime. She buys it from Adam Smith for Rs.4,000

FIIs have been quite entry in the Indian markets but do not seem to find any great investments. However, they carry with themselves lots of knowledge of the sunrise industries in the world, IT services being one of them. Back home in the US, they are increasingly hearing names like TCS and Infosys. They get classified information that Infosys is likely to get a big order from General Electric, which would result in Infy’s profits to grow by 100 per cent for the next two years. Impact of this on Infy’s profits -

Year V Year VI • Net profit - 2,400 4,800 • No. of shares - 3 3 • EPS - Rs.800 Rs.1600 • Share price - Rs.4000 Rs.4000 • p/e ratio - 5 2.5 We have a situation where the company’s yield at current prices exceed 20 % in Year V and 40% in Year VI. But, our Ms.Fiona is unaware of this development and would probably sell her holding in Infy if good offer in put on table.

There are over a dozen FIIs willing to pay higher price for Fiona’s share in Infy. They all start bidding. Remember the share will become unattractive when the ROCE on Infy share is less than 5% (this is because FIIs get 2% return in their own country, they would expect a risk premium from an Indian co. of around 3%). As more and more FIIs bid, they all start discounting the expected earnings of Infy in Year VI (ie. EPS of Rs.1600). The final bid came in at Rs.25,000. (with an expected ROCE of 6.4 per cent in Year VI) Which is much better than most of the FIIs are getting in today’s scenario and infact interest rates may go down further in Year VI. What this means for the Infy share in the current year – • Net profit - Rs. 1200 • No. of share - 3 • EPS - Rs.400 • Mkt price - Rs.25,000 • p/e ratio - 62.5 • ROCE - 1.6 % • No. of yrs to double - 45 years.

Although Infy is not a sound investment if a person is looking at one year’s perspective but if the company’s net profit is going to grow by 100 per cent for the next two years than the Rs.25,000 paid now would look good investment two years from now (Year V ROCE = 3.2%, Year Vi ROCE = 6.4 %, compared to an estimated interest rate of 4.5% in Year VI in India and a mere 1.25 % in the US). Conclusion – An investor is willing to pay 62.5 times (pe ratio) of Infy’s current years earnings to gain healthy returns in the future.

What happens if the GE order for Infy is half its estimated size? Year V Year VI • Net profit - 1,800 2,400 • No. of shares - 3 3 • EPS - Rs.600 Rs.800 • Share price - Rs.25,000 Rs.25,000 • p/e ratio - 41.67 31.25 • ROCE (est) - 2.4% 3.2% • THIS IS LESS THAN THE REQD 6.4 %

The FII dumps the share as the size has turned out to lower than his estimates. So now when others bid for the Infy share they would include the effect of the GE order. The new share price on offer in the market is Rs.12,500 per share ( or 6.4 per cent estd. ROCE for the year VI). What this means for the Infy share in the year IV (or the current year) – • Net profit - Rs. 1200 • No. of share - 3 • EPS - Rs.400 • Mkt price - Rs.12,500 • p/e ratio - 31.25 • ROCE - 3.2 % • No. of yrs to double - 22.5 20years.

Final Conclusion PE ratio is generally an indicator of the markets expectation of a company’s future earnings. Higher the PE ratio, higher the expectation. Infosys, Wipro and TCS all trade at PE ratio of 30+ this is because the company’s are expected to report 30+ profit growth in the foreseeable future. High growth stocks tend to have high PE ratios because lot of expectations are built in their stock prices. But growth stocks are also the ones with highest risk as if the growth is not realized the PE’s of these stocks tend to fall with the strongest of gravitational forces. Contrary to IT companies, TISCO which reported over 100 % growth in net profits last year is trading at a PE ratio of around 7-8. This is because it belongs to the infrastructure sector where growth is often directly co-related to the GDP growth. Hence u would find PE ratio of all infrastructure related industries to be near 6-10. And the current growth in net profit is an aberration which will eventually correct when steel prices head down-south.