Download

1 / 46

460 likes | 484 Views

This article explores the importance of profit and loss statements in maximizing profitability in the optometric industry. It covers topics such as understanding income statements, practice operating ratios, industry benchmarks, and evaluating financial success.

E N D

Profit and Loss…Do I Really Have A Choice? Steven Sunder, BS, ABOC, FNAO Practice Management Consultant

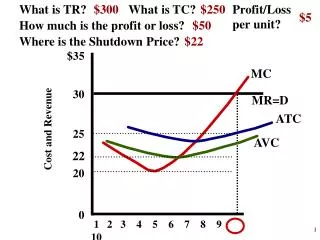

Agenda • Objective • Understanding the Profit & Loss statement • Practice Operating Ratios • Optometric Industry Benchmarks & Your Practice Ratios • Conclusion • Q & A • Terms The most important goal of financial management is to “maximize the highest possible profit for the practice” while providing superior medical eye care to your patients.

Objective • How do I read this thing? • How do I measure my financial success? • How am I doing? • How do I compare to my peers/industry?

Income/Profit and Loss Statement An income statement, otherwise known as a profit and loss, is a financial statement summarizing all the revenue and expense transactions that result in a profit or loss over a period of time.

Components of an Income Statement • Practice Revenue • Cost of Goods Sold • Gross Profit/Margin • Operating Expenses • Net Margin

Components of an Income Statement • Practice Revenue • Cost of Goods Sold • Gross Profit/Margin • Operating Expenses • Net Margin

Components of an Income Statement • Practice Revenue • Cost of Goods Sold • Gross Profit/Margin • Operating Expenses • Net Margin

Components of an Income Statement Does an “in-house” lab truly increase profit?

Components of an Income Statement • Practice Revenue • Cost of Goods Sold • Gross Profit/Margin • Operating Expenses • Net Margin

Income/Profit and Loss Statement • The gross margin on sales minus the total operating expenses provides the net income on operations (pretax).

Components of an Income Statement Practice A Statement of Earnings For The 4 Months Ending April 30, 20__ Actual Budgeted Variance Variance YTD YTD $'s % Revenue: 291,644 257,882 33,762 13% Cost of sales: 72,832 53,505 (19,327) -36% 218,812 Gross profit 204,377 (14,435) -7% Would Frame Board Management Increase Gross Profit?

Components of an Income Statement • Practice Revenue • Cost of Goods Sold • Gross Profit/Margin • Operating Expenses • Net Margin

Income/Profit and Loss Statement • Operating expenses include fixed and variable expenses.

Profit & Loss Statement The Profit and Loss Statement shows how well your practice buys and sells inventory (or services) to make a profit.

Using Income and Profit & Loss Statements for Feedback You use an income/profit and loss statement to track revenues and expenses so that you can determine the operating performance of your business over a period of time.

Components of an Income and Profit & Loss Statements Examination Fee (92004): $89.00 TPA Reimbursement: $45.00 Net Revenue to Practice: $45.00 Practice “Write Off”: $44.00 Gross Profit Margin: 50.5%

Components of an Income and Profit & Loss Statements OPPORTUNITY COST: The amount of income that would result from the best available alternative to a proposed use of cash or its equivalent. In other words, it represents the forgoing of possible income associated with a lost opportunity.

Components of an Income and Profit & Loss Statements • Controllable Expenses • Fixed Expenses • Miscellaneous

Using the Income and Profit & Loss Statements for Feedback • How do you know if your practice suffers from “practicea inefficoccus,” also known as practice inefficiency? Would you like to make more money? If so, your practice must become efficient and productive. • To evaluate just how efficient your practice is, you will need to measure three criteria: • Your practice history • Your practice ratios • Optometric industry benchmarks for comparison

Using the Income and Profit & Loss Statements for Feedback Creating a profit and loss statement on a regular basis will provide you with a true cash picture of your practice’s profitability and help you decide where to make changes in the budget, collections policies or spending habits.

Using the Income and Profit & Loss Statements for Feedback “The foundation of effective leadership is thinking through the organization’s difference, defining it and establishing it, clearly and visibly.”

Practice Operational Ratios • Practice Ratios: • When evaluating the financial “health” of your practice, practice ratios are used to measure your your financial state.

Practice Operational Ratios Where is the revenue coming from?

Practice Operational Ratios What are my cost of goods sold and gross profit margin?

Practice Operational Ratios What are my practice operational expenses?

Practice Operational Ratios What is my practice net margin?

Practice Operational Ratios • Tracking and controlling your practice ratios is a very simple yet a valuable tool used in evaluating your practice for operational efficiency opportunities. • Controlling practice ratios = more $ in your savings account

Optometric Industry Benchmarks Should you care how your practice measures against your peers?

Optometric Industry Benchmarks The 11 Key Industry Benchmarks Optometric Industry Benchmark Analysis As a Rate to Net Revenue Revenue Industry Professional: 32.00% Optical: 46.00% Contacts: 22.00% Total 100.00% Cost of Goods Sold 27.00% Expenses Compensation Staff Optometrist: 21.00% Support Staff: 18.00% Facility: 8.00% Marketing & Advertising: 4.00% Equipment: 5.00% General: 6.00% Net Revenue 30.00%

Optometric Industry Benchmarks Practice A Industry Benchmark Analysis Optometric Industry Benchmark Analysis As a Rate to Net Revenue Revenue Industry Practice A Variance +/- Professional: 32.00% 59.11% 27.11% Optical: 46.00% 40.89% -5.11% Contacts: 22.00% - - Total 100.00% 100.00% - Cost of Goods Sold 27.00% 24.97% -2.03% Expenses Compensation Staff Optometrist: 21.00% 19.62% -1.38% Support Staff: 18.00% 16.44% -1.56% Facility: 8.00% 2.35% -5.65% Marketing & Advertising: 4.00% 0.63% -3.37% Equipment: 5.00% 1.01% -3.99% General: 6.00% 9.51% 3.51% Net Revenue 30.00% 25.47% -4.53%

Components of an Income and Profit & Loss Statements Labor Cost Initiatives • Determine the costs to your practice for: • Manual Confirmation Calls • Hard Copy Recalls • Frame Board Management System • Chair Costs • After determining what your current costs are of these processes, evaluate alternatives to increase net margin/ net profit.

Optometric Industry Benchmarks You have attained an understanding of the Profit and Loss Statement, calculating practice ratios and comparing to the optometric industry benchmarks, so what is the next step in evaluating your practice operational efficiencies?

Optometric Industry Benchmarks • Questions to ask yourself are: • What are the total number of exams generated? • How much revenue do I generate per hour? • How do I increase my Gross Profit? • How do I reduce my laboratory and frame expense? • How much revenue does my support staff generate per hour? • What is my practice revenue per square foot? • What is my frame inventory turnover rate? • Would “Frame Board Management” improve profit margin?

Terms BALANCE SHEET: A financial statement listing the assets, liabilities, and owner’s equity of a business entity as of a specific date. [How much am I worth] BUDGET: A formal written statement of management’s plans for the future, express in financial terms. [Future projection of revenue, COG’s, expenses, and net revenue] CASH FLOW: Earnings before depreciation and amortization. [Amount of excess cash available at end of month] COST OF GOODS SOLD: The cost of the manufactured product sold. Costs include materials purchased from outside suppliers used in the manufacture of your products, as well as any internal expenses directly expended in the process such as finishing lab optician.

Terms DEPRECIATION: The decrease in usefulness of all practice assets except land. EXPENSES: The amount of assets consumed or services used in the process of earning revenue. [What it costs to run your practice] GROSS PROFIT: The excess of net revenue from sales over the cost of the merchandise sold. [Profit available to pay expenses] INVENTORY TURNOVER: The relationship between the volume of goods sold and inventory, computed by dividing the cost of goods sold by the average inventory. [How many times your physical inventory is sold]

Terms NET INCOME: The final figure in the income/profit and loss statement when revenues exceed expenses. [What you have left over after paying all practice expenses aka, your savings account] OPPORTUNITY COST: The amount of income that would result from the best available alternative to a proposed use of cash or its equivalent. In other words, it represents the forgoing of possible income associated with a lost opportunity.