Download

1 / 21

210 likes | 428 Views

Mathematical Programming Models for Asset and Liability Management Katharina Schwaiger, Cormac Lucas and Gautam Mitra, CARISMA, Brunel University West London. 22 nd European Conference on Operational Research Prague, July 8-11, 2007 Financial Optimisation I, Monday 9 th July, 8:00-9.30am.

E N D

Mathematical Programming Models for Asset and Liability ManagementKatharina Schwaiger, Cormac Lucas and Gautam Mitra,CARISMA, Brunel University West London 22nd European Conference on Operational Research Prague, July 8-11, 2007 Financial Optimisation I, Monday 9th July, 8:00-9.30am

Outline Problem Formulation Scenario Models for Assets and Liabilities Mathematical Programming Models and Results: Linear Programming Model Stochastic Programming Model Chance-Constrained Programming Model Integrated Chance-Constrained Programming Model Discussion and Future Work

Problem Formulation • Pension funds wish to make integrated financial decisions to match and outperform liabilities • Last decade experienced low yields and a fall in the equity market • Risk-Return approach does not fully take into account regulations (UK case) use of Asset Liability Management Models

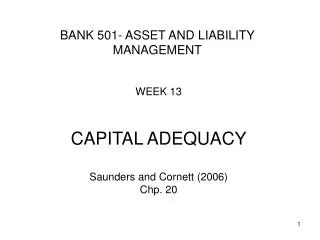

Pension Fund Cash Flows Sponsoring Company Figure 1: Pension Fund Cash Flows • Investment: portfolio of fixed income and cash

Mathematical Models • Different ALM models: • Ex ante decision by Linear Programming (LP) • Ex ante decision by Stochastic Programming (SP) • Ex ante decision by Chance-Constrained Programming • All models are multi-objective: (i) minimise deviations (PV01 or NPV) between assets and liabilities and (ii) reduce initial cash required

Asset/Liability under uncertainty • Future asset returns and liabilities are random • Generated scenarios reflect uncertainty • Discount factor (interest rates) for bonds and liabilities is random • Pension fund population (affected by mortality) and defined benefit payments (affected by final salaries) are random

Scenario Generation • LIBOR scenarios are generated using the Cox, Ingersoll, and Ross Model (1985) • Salary curves are a function of productivity (P), merit and inflation (I) rates • Inflation rate scenarios are generated using ARIMA models

Linear Programming Model • Deterministic with decision variables being: • Amount of bonds sold • Amount of bonds bought • Amount of bonds held • PV01 over and under deviations • Initial cash injected • Amount lent • Amount borrowed • Multi-Objective: • Minimise total PV01 deviations between assets and liabilities • Minimise initial injected cash

Linear Programming Model • Subject to: • Cash-flow accounting equation • Inventory balance • Cash-flow matching equation • PV01 matching • Holding limits

Linear Programming Model PV01 Deviation-Budget Trade Off

Stochastic Programming Model • Two-stage stochastic programming model with amount of bonds held , sold and bought and the initial cash being first stage decision variables • Amount borrowed , lent and deviation of asset and liability present values ( , ) are the non-implementable stochastic decision variables • Multi-objective: • Minimise total present value deviations between assets and liabilities • Minimise initial cash required

SP Model Constraints • Cash-Flow Accounting Equation: • Inventory Balance Equation: • Present Value Matching of Assets and Liabilities:

SP Constraints cont. • Matching Equations: • Non-Anticipativity:

Stochastic Programming Model Deviation-Budget Trade-off

Chance-Constrained Programming Model • Introduce a reliability level , where , which is the probability of satisfying a constraint and is the level of meeting the liabilities, i.e. it should be greater than 1 in our case • Scenarios are equally weighted, hence • The corresponding chance constraints are:

CCP Model Cash versus beta

CCP Model SP versus CCP frontier

Integrated Chance Constraints • Introduced by Klein Haneveld [1986] • Not only the probability of underfunding is important, but also the amount of underfunding (conceptually close to conditional surplus-at-risk CSaR) is important Where is the shortfall parameter

Discussion and Future Work Generated Model Statistics:

Discussion and Future Work • Ex post Simulations: • Stress testing • In Sample testing • Backtesting

References • J.C. Cox, J.E. Ingersoll Jr, and S.A. Ross. A Theory of the Term Structure of Interest Rates, Econometrica, 1985. • R. Fourer, D.M. Gay and B.W. Kernighan. AMPL: A Modeling Language for Mathematical Programming. Thomson/Brooks/Cole, 2003. • W.K.K. Haneveld. Duality in stochastic linear and dynamic programming. Volume 274 of Lecture Notes in Economics and Mathematical Systems. Springer Verlag, Berlin, 1986. • W.K.K. Haneveld and M.H. van der Vlerk. An ALM Model for Pension Funds using Integrated Chance Constraints. University of Gröningen, 2005. • K. Schwaiger, C. Lucas and G. Mitra. Models and Solution Methods for Liability Determined Investment. Working paper, CARISMA Brunel University, 2007. • H.E. Winklevoss. Pension Mathematics with Numerical Illustrations. University of Pennsylvania Press, 1993.