Y = C + I + G + NX

300 likes | 511 Views

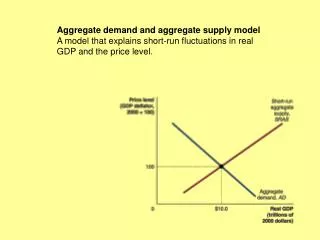

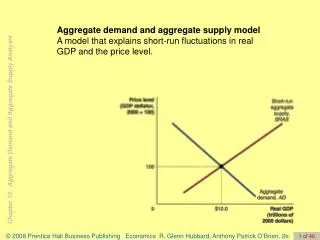

Aggregate demand and aggregate supply model A model that explains short-run fluctuations in real GDP and the price level.

Y = C + I + G + NX

E N D

Presentation Transcript

Aggregate demand and aggregate supply model A model that explains short-run fluctuations in real GDP and the price level.

Aggregate DemandGDP has four components: consumption (C), investment (I), government purchases (G), and net exports (NX). If we let Y stand for GDP, we can write the following: Y = C + I + G + NX Why Is the Aggregate Demand Curve Downward Sloping? The International-Trade Effect (substitution of foreign stuff for our stuff): When our price level rises, foreigners buy less of our exports and we import more things from abroad. When our price level rises, the real value of our monetary wealth declines. We feel poorer. The Wealth Effect: When our monetary wealth declines, we feel poorer and buy less. When our price level rises, real money balances (M/P) become scarcer and the interest rate rises. The Interest-Rate Effect: A higher interest rate discourages spending, investment spending in particular.

What Shifts the Aggregate Demand Curve? Changes in Government Policies intended to achieve macroeconomic objectives: high employment, price stability, steady economic growth. • Monetary policy Actions the Federal Reserve takes to manage the money supply and interest rates. • Fiscal policy Changes in federal taxes and purchases. Changes in Expectations of Households and Firms • If households become more optimistic about their future incomes, they are likely to increase their current consumption. Changes in Foreign Variables • If foreign economies expand, foreign firms and households will buy more U.S. goods. • If the dollar depreciates, foreign firms and households will buy more U.S. goods and U.S. firms and households will buy fewer foreign goods. Net exports will rise and the aggregate demand curve will shift to the right.

Movements along the Aggregate Demand Curve versus Shifts of the Aggregate Demand Curve When taxes increase or government spending decreases, when the money supply is reduced or when people lose confidence, aggregate demand shifts to the left When price rises, less domestic output is demanded owing to the international-trade effect, the wealth effect and the interest rate effect.

The Long-Run Aggregate Supply Curve LRAS reflects the economy’s output capacity at full employment of available resources using the best available technology. LRAS shifts outward as capital accumulates, the labor force grows and as technology improves.

Aggregate Supply The Short-Run Aggregate Supply Curve Why does the short-run aggregate supply curve slope upward? 1 Contracts make some wages and prices “sticky.” 2 Firms are often slow to adjust wages. 3 Menu costs make some prices sticky.

Variables That Shift the Short-Run Aggregate Supply Curve Expected Changes in the Future Price Level How Expectations of the Future Price Level Affect the Short-Run Aggregate Supply

Aggregate Supply Variables That Shift the Short-Run Aggregate Supply Curve Adjustments of Workers and Firms to Errors in Past Expectations about the Price Level Unexpected Changes in the Price of an Important Natural Resource Supply shock An unexpected event that causes the short-run aggregate supply curve to shift.

Variables That Shift the Short-Run Aggregate Supply Curve Unexpected Changes in the Price of an Important Natural Resource

Macroeconomic Equilibriumin the Long Run and the Short Run Long-Run Macroeconomic Equilibrium

Macroeconomic Equilibriumin the Long Run and the Short Run Recessions, Expansions, and Supply Shocks Because the full analysis of the aggregate demand and aggregate supply model can be complicated, we begin with a simplified case, using two assumptions: 1 The economy has not been experiencing any inflation. The price level is currently 100, and workers and firms expect it to remain at 100 in the future. 2 The economy is not experiencing any long-run growth. Potential real GDP is $10.0 trillion and will remain at that level in the future.

Macroeconomic Equilibriumin the Long Run and the Short Run Recessions, Expansions, and Supply Shocks Recession The Short-Run and Long-Run Effects of a Decrease in Aggregate Demand

Macroeconomic Equilibriumin the Long Run and the Short Run Expansion FIGURE 12.6 The Short-Run and Long- run Effects of an Increase in Aggregate Demand

Learning Objective 12.3 Macroeconomic Equilibriumin the Long Run and the Short Run Recessions, Expansions, and Supply Shocks Supply Shock Stagflation A combination of inflation and recession, usually resulting from a supply shock.

Macroeconomic Equilibriumin the Long Run and the Short Run Supply Shock Stagflation The Short-Run and Long-Run Effects of a Supply Shock

A Dynamic Aggregate Demandand Aggregate Supply Model We can create a dynamic aggregate demand and aggregate supply model by making three changes to the basic model. • Potential real GDP increases continually, shifting the long-run aggregate supply curve to the right. • During most years, the aggregate demand curve will be shifting to the right. • Except during periods when workers and firms expect high rates of inflation, the short-run aggregate supply curve will be shifting to the right as productivity increases.

Learning Objective 12.4 A Dynamic Aggregate Demandand Aggregate Supply Model FIGURE 12.8 A Dynamic Aggregate Demand and Aggregate Supply Model

A Dynamic Aggregate Demandand Aggregate Supply Model The Usual Cause of Inflation: AD increases by more than AS

Learning Objective 12.4 A Dynamic Aggregate Demandand Aggregate Supply Model The Slow Recovery from the Recession of 2001 The recession of 2001 was caused by a decline in aggregate demand. Several factors contributed to this decline: • The end of the stock market “bubble.” • Excessive investment in information technology. • The terrorist attacks of September 11, 2001. • The corporate accounting scandals.

The Slow Recovery from the Recession of 2001 Aggregate demand increased slowly following the dot.com bust and 9/11

K e y T e r m s Aggregate demand and aggregate supply model Aggregate demand curve Fiscal policyLong-run aggregate supply curve Menu costs Monetary policy Short-run aggregate supply curveStagflation Supply shock

Keynesian revolution The name given to the widespread acceptance during the 1930s and 1940s of John Maynard Keynes’s macroeconomic model and activist policy prescriptions. • Macroeconomic Schools of Thought These alternative schools of thought use models that differ significantly from the standard aggregate demand and aggregate supply model. We can briefly consider each of the three major alternative models: 1 The monetarist model 2 The new classical model 3 The real business cycle model

TheMonetaristModel • Macroeconomic Schools of Thought The monetarist model—also known as the neo-Quantity Theory of Money model—was developed beginning in the 1940s by Milton Friedman, an economist at the University of Chicago who was awarded the Nobel Prize in Economics in 1976. Monetary growth rule A plan for increasing the quantity of money at a fixed rate that does not respond to changes in economic conditions. Monetarism The macroeconomic theories of Milton Friedman and his followers; particularly the idea that the quantity of money should be increased at a constant rate.

The New Classical Model • Macroeconomic Schools of Thought The new classical model was developed in the mid-1970s by a group of economists including Nobel laureate Robert Lucas of the University of Chicago, Thomas Sargent of New York University, and Robert Barro of Harvard University. New classical macroeconomics The macroeconomic theories of Robert Lucas and others, particularly the idea that workers and firms have rational expectations.

The Real Business Cycle Model • Macroeconomic Schools of Thought Beginning in the 1980s, some economists, including Nobel laureates Finn Kydland of Carnegie Mellon University and Edward Prescott of Arizona State University, argued that Lucas was correct in assuming that workers and firms formed their expectations rationally and that wages and prices adjust quickly to supply and demand but wrong about the source of fluctuations in real GDP. Real business cycle model A macroeconomic model that focuses on real, rather than monetary, causes of the business cycle.

MakingtheConnection • Karl Marx: Capitalism’s Severest Critic • … or most perceptive analyst? Karl Marx predicted that a final economic crisis would lead to the collapse of the market system.