Download

1 / 11

130 likes | 280 Views

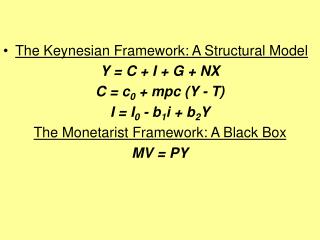

The Keynesian Framework: A Structural Model Y = C + I + G + NX C = c 0 + mpc (Y - T) I = I 0 - b 1 i + b 2 Y The Monetarist Framework: A Black Box MV = PY.

E N D

The Keynesian Framework: A Structural Model Y = C + I + G + NX C = c0 + mpc (Y - T) I = I0 - b1i + b2Y The Monetarist Framework: A Black Box MV = PY

… Speculators may do no harm as bubbles on a stream of steady enterprise. But the position is serious when enterprise becomes a bubble on a whirlpool of speculation. When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done. John Maynard Keynes The General Theory of Employment, Interest and Money

Keynesian - Monetarist Debates • Keynesians: Monetary policy does not matter • Low interest rates during the Great Depression expansionary monetary policy didn’t help • Nominal interest rates don’t affect investment • Surveys confirmed investment in physical capital not based on market interest rates • Monetarists: Money matters most • Depression -- The Great Contraction • Deflation high real interest rates • Interest-rate effects are only one of many channels • But is there reverse causation?

Beware Financial Instability! • … small events at times have large consequences, there are such things as chain reactions and cumulative forces. It happens that a liquidity crisis in a fractional reserve banking system is precisely the kind of event that can trigger – and often has triggered – a chain reaction. And economic collapse often has the character of a cumulative process. Let it go beyond a certain point, and it will tend for a time to gain strength from its own development as its effects spread and return to intensify the process of collapse. Because no great strength would be required to hold back the rock that starts a landslide, it does not follow that the landslide will not be of major proportions. • Milton Friedman and Anna Jacobson Schwartz, A Monetary History of the United States, 1867 – 1960, p. 419.

Lessons for Monetary Policy • Don’t associate the stance of monetary policy with ups and downs of short-term nominal interest rates • Other asset prices are important elements in various monetary policy transmission mechanisms • Monetary policy can be highly effective in reviving a weak economy even if short-term interest rates are already near zero • Pump up liquidity … pump up asset prices

Lessons for Monetary Policy (cont’d) • Monetary policy can be highly effective in reviving a weak economy even if short-term interest rates are already near zero • Avoiding unanticipated fluctuations in the price level is an important objective of monetary policy, thus providing a rationale for price stability as the primary long-run goal for monetary policy