Download

1 / 10

100 likes | 128 Views

Explore the fixing of exchange rates and interest rates in the Eurozone from 2008 to 2011. Delve into current account balances, real estate prices, and the Target 2 rescue mechanism. Discover the challenges and potential solutions for European financial stability.

E N D

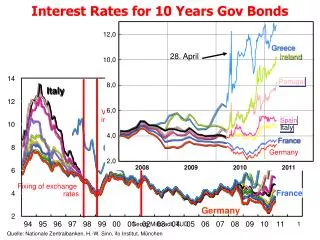

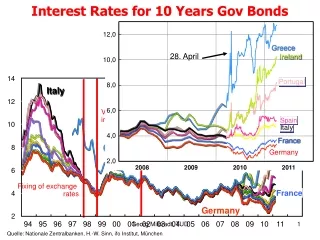

12,0 10,0 14 Virtual Euro introduction 8,0 Tatsächliche Einführung 12 6,0 10 4,0 8 2,0 6 2008 2009 2010 2011 Fixing of exchange rates 4 2 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 Interest Rates for 10 Years Gov Bonds 30. März 7. Mai Greece 28. April Ireland % Portugal Italy Spain Italy France Greece Germany France Germany Georg Milbradt, TUD Quelle: Nationale Zentralbanken, H.-W. Sinn, ifo Institut, München. März 2011

Quelle: EEAG, 2011, S.76 2 Georg Milbradt, TUD

5,6 Luxembourg 5,4 Netherlands Germany 4,9 Austria* 3,2 Finland 1,3 Belgium 0,5 Slowenia -1,0 -2,2 France Ireland -2,9 Italy -3,2 Slowakiai -3,2 Malta -3,9 Spain -5,4 -8,3 Cyprus -10,3 Portugal Greece -11,2 5 -15 -10 -5 0 10 Current Account Balance in % GDP (2009) % des BIP Georg Milbradt, TUD 3 * 2008 Quelle: H.-W. Sinn, ifo Institut, München

130 120 110 100 90 80 70 60 50 40 30 20 10 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 Real Estate Prices 1996 – 2009 1th Quarter 2006 = 100 Spain Germany -16%** -17% Ireland -24% Italy France UK* ** Spain: IV Quarter 2008. Georg Milbradt, TUD 4 Quelle: The Economist and Social Research Institute; UK: Land Registry ; Deutschland: DESTATIS; Frankreich: INSEE; Italien: Banca d`Italia, H.-W. Sinn, ifo Institut, München * England und Wales. 23. September 2009

Target 2 – The Unknown Rescue Mechanism Milliarden Euro 400 Dec. 2010: 326 bln Euro ECB Money Supply 1,061 bln Euro ( 8th March 2011) 350 March 2011 323 vbn Euro 4th Q. 2010: 315 bln Euro Accummulated current account deficits of GIPS 300 250 200 150 100 50 TARGET2 Bundesbank 0 -50 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Georg Milbradt, TUD 5 Quelle: Hans-Werner Sinn, ifo; Nichts als Zeitgewinn Quelle: Eurostat; EZB; Deutsche Bundesbank.

Target 2- Balances Georg Milbradt, TUD Quelle: Hans-Werner Sinn; Nichtsals Zeitgewinn

Rescue Packages -Total Liabilities (Bln Euro) German Share Total Default of all GIPS-Countries IMF with ESM 250 Cash (ESM) 15 80 22 Guaranties (ESM) 168 2 620 27 IMF Rescue Package Greece 25 EU Rescue Package Greece 30 ECB Purchase of Gov Bonds 115 80 76 TARGET-Liabilities (only GIPS) 373 344 1480 Georg Milbradt, TUD 7 Quelle: Hans-Werner Sinn, ifo; Nichts als Zeitgewinn

Black Mail Potential • European banks – low capital-asset ratio • European Central Bank – risk of losses and problems with reputation • Governments – fear to face situation and fiscal consequences before the public • Loyal countries are blackmailed by the sinners Buying of time without solutions, problems and imbalances becoming bigger and bigger, solutions more and more expensive Georg Milbradt, TUD

EU Propositions March 2011 • Permanent European Stability Mechanism, higher amount, with cash contributions, priority like IMF, no automatic participation of private creditors, breach of EU treaty legalized by amendment • Tightened Stability and Growth Pact (speeding up, semi-automatic, inclusion of total debt and other important economic indicators), but still basic decisions by EcoFin-Council • Euro-Plus-Pact (self commitment of governments to more convergence), no sanctions, fig-leaf Georg Milbradt, TUD

Solutions (I) • No improvement without politically accepted defaults of sovereigns and banks • Otherwise danger of shifting the bill to the tax payers • Extension of mistakes Therefore institutional Improvements to avoid black mail: • Recapitalization of banks • Restriction of the ECB to pure monetary policy • Bankruptcy regulation for states, collective action clauses Georg Milbradt, TUD