Exchange Rates

Exchange Rates. Antu Panini Murshid. Today’s Agenda. Nominal vs. real exchange rate Asset market approach Uncovered interest rate parity. Currencies and Exchange Rates. Each country has a currency in which the prices of goods and services are quoted

Exchange Rates

E N D

Presentation Transcript

Exchange Rates Antu Panini Murshid

Today’s Agenda • Nominal vs. real exchange rate • Asset market approach • Uncovered interest rate parity

Currencies and Exchange Rates • Each country has a currency in which the prices of goods and services are quoted • An exchange rate is the price of one currency in terms of another. This is sometimes called the nominal exchange rate

Exchange Rate Quoting • An exchange rate can be quoted in two ways • Direct (American) terms and indirect (European) terms • In this course we will always (unless otherwise stated) quote the exchange rate in direct terms

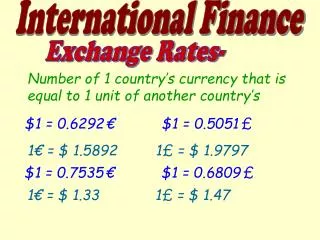

Direct Terms • Price of foreign currency in terms of national currency • How many units of national currency do we need to buy a unit of foreign currency • Example $/€, $/¥ • Today’s dollar-euro exchange rate is $1.07384 per euro

Indirect Terms • Price of national currency in terms of foreign currency • How many units of foreign currency do we need to buy a unit of national currency • Example €/$, ¥/$ • Today’s euro-dollar exchange rate is €0.931015 per USD

Appreciation and Depreciation of a Currency • A depreciation of the dollar against the euro means that the price of a euro in terms of dollars has gone up • An appreciation of the dollar against the euro means that the price of a euro in terms of dollars has gone down

Appreciation and Depreciation of a Currency • If the dollar depreciates against the euro this must mean that the euro has appreciated against the dollar • If the dollar appreciates against the euro this must mean that the euro has depreciated against the dollar

Appreciation and Depreciation of the Exchange Rate • An exchange rate depreciation means the domestic currency has depreciated and an exchange rate appreciation means the domestic currency has appreciated • If the exchange rate depreciates then e↑ • If the exchange rate appreciates then e↓

Example • If the $/€ exchange rate moves from e=1.00 to e=.95…. • exchange rate has appreciated by 5% • Dollar has appreciated against the euro by 5% (it now cost $0.95 as opposed to $1 to buy €1) and the euro has depreciated against the dollar by approximately 5% (it now costs €1.05 to buy $1)

Real Exchange Rate • Suppose a car in UK costs ₤30,000, if e=1.50, then dollar price is $45,000, i.e. the price of foreign goods in terms of domestic currency is ePf • Suppose the same car in the US costs $36,000, then the price of the foreign car in terms of the price of domestic cars is ePf/P=1.25

Real Exchange Rate • The real exchange rate (θ) gives the price of a unit of a foreign goods, in terms of the price of domestic goods • That is θ = ePf / P, where P is the domestic price level and Pfis foreign price level

Real Exchange Rate Appreciation/Depreciation • If θ↑ we say that the real exchange rate has depreciated • θ↑ if either e↑ P↓ or Pf↑ • If θ↓ we say that the real exchange rate has appreciated • θ↓if either e↓ P↑ or Pf↓

Competitiveness • If the real exchange rate depreciates, the price of foreign goods relative to the price of domestic goods increases and exports become more competitive while imports become more expensive • If the real exchange rate appreciates, the price of foreign goods relative to the price of domestic goods decreases and exports become less competitive while imports become cheaper

Foreign Exchange Market • Players in the foreign exchange market • Commercial banks, large corporations, non-bank financial institutions, central banks • Commercial banks are by far the largest players in the foreign exchange market. However large corporations like IBM and GE also engage in significant transactions. Another groups of important players are central banks

Foreign Exchange Market • Characteristics of the market • The main markets are London, New York, Tokyo • Daily global value of forex trading $1.7 trillion • $ vehicle currency

Determination of the Spot Exchange Rate • What determines the exchange rate? • Demand and supply • What factors might affect demand and supply? • Inflation rates? • Trade deficits? • Demand for assets?

Expected Returns • Expected rate of return • Risk and liquidity • We will abstract from risk and liquidity for now and assume that these characteristics are the same across different assets. If this is the case, we will prefer to hold assets offering the highest expected rate of return

How Do We Compare Returns on Various International Assets? • $-assets pay returns in dollars • €-assets pay returns in euros • In order to compare these returns, we need to measure all returns in terms of one currency

How Do We Compare Returns on Various International Assets? • But why does it matter, isn’t 5% interest in the US just the same as 5% in Germany? • No…because the exchange rate between dollar and the euro may change

Example • Suppose the $/€ exchange rate is 1.00 • The interest rate in the US is 10% • The interest rate in Germany is 5% • Expect $/€ exchange rate to be 1.10 • Which asset offers the highest rate of return?

Example • Gross return on $1 deposited at a US bank is $1.10 • What is the gross return on $1 deposited in a German bank?

Example • 1. Convert dollars to euros: • $1→ €1 • 2. Invest in Germany: • Gross return €1.05 • 3. Convert back to dollars • €1.05 → $1.15 • Return on €-asset is 15% = if+E(%De)

Equilibrium Exchange Rate • If the rate of return on dollar assets is greater than the dollar rate of return on euro assets there will be an excess demand for dollar assets • If the rate of return on dollar assets is less than the dollar rate of return on euro assets there will be an excess demand for euro assets • Only when the rate of return on dollar assets is equal to the rate of return on euro assets will the exchange rate be in equilibrium

Uncovered Interest Rate Parity Condition • The UCIP condition states that the return to investing in domestic assets must equal the expected return on investing in foreign assets (when the returns are measured in the same currency) • i ≈ if + %E(∆e)

Example: UCIP Holds • i = 10% (US rate), if = 5% (German rate), et = 1.00 ($/€) and E(et+1) = 1.05 • Expected return to a $100 investment in €-denominated German asset is: • 1. Convert $ to €: $100/e = 100€ • 2. Receive 105 € in 1 year • 3. Covert back to $: (105 €)*1.05 ≈ $110 • UIPC holds

Example: UCIP Doesn’t Hold • i = 10% (US rate), if = 8% (German rate), et = 1.00 ($/€) and E(et+1) = 1.05 • Expected $-return in €-denominated German asset is 8%+5%=13% > 10% ($-return on US asset) • Demand for €-deposits/assets ↑ • $ depreciates immediately (e↑) e = 1.03. • Since E(et+1) = 1.05, %E(∆e)=2% • Hence %E(∆e)+if=8%+2%=10%=i

Example: UCIP Doesn’t Hold • Suppose now instead that the domestic interest rate increases such that i = 12% (US rate). If if = 5% (German rate), et = 1.00 ($/€) and E(et+1) = 1.05, then the demand for US assets increases and the dollar appreciates to et = 0.98. Thus %E(∆e)=7%, so UCIP is again restored

$-Return on Foreign Assets and the Exchange Rate $/€ e 1.10 Expected $-return on € assets 1.05 1.00 0.95 0 5 10 15 $-rate of return on € assets

Equilibrium Exchange Rate—Graphical Representation $/€ e Rate of return on dollar assets e2 UIPC holds—equilibrium exchange rate e1 Expected return on € assets e3 $-rate of return on € assets

Effect of an Increase in Domestic Interest Rates $/€ e Original equilibrium New equilibrium—the exchange rate appreciates today and UCIP is restored Domestic interest rate increases e1 e2 Expected return on € assets i1 i2 $-rate of return on € assets

Effect of an Increase in Foreign Interest Rates $/€ e New equilibrium Original equilibrium e2 Foreign interest rate increases e1 Expected return on € assets i $-rate of return on € assets

Effect of a Change in Expectations $/€ e New equilibrium Original equilibrium e2 Rise in expected future price of euros e1 Expected return on € assets i $-rate of return on € assets