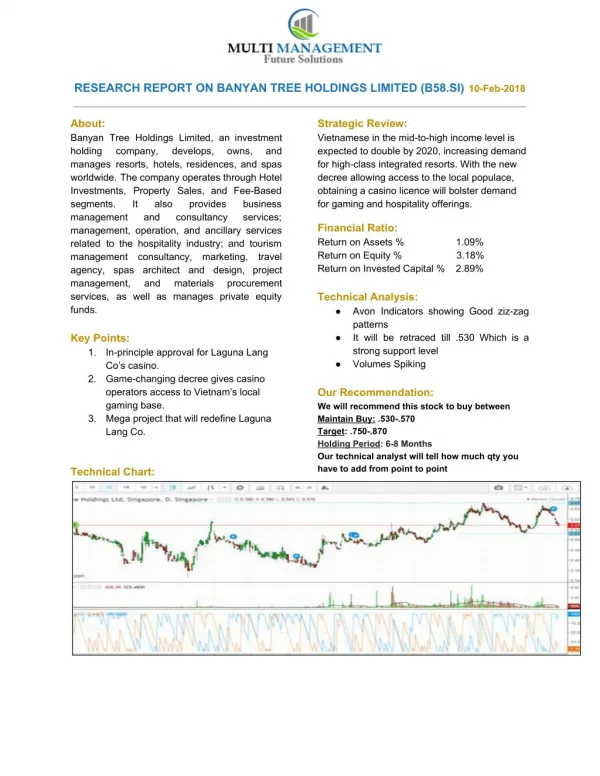

Download

1 / 44

440 likes | 600 Views

ABC HOLDINGS LIMITED. Results Presentation for the year ended 31 December 2008. AGENDA. Economic Environment Financial Performance Overview Income statement review Balance sheet review Outlook Challenges & outlook Capitalisation Dividend.

E N D

ABC HOLDINGS LIMITED Results Presentation for the year ended 31 December 2008

AGENDA • Economic Environment • Financial Performance • Overview • Income statement review • Balance sheet review • Outlook • Challenges & outlook • Capitalisation • Dividend

ECONOMIC ENVIRONMENT & INDUSTRY ATTRACTIVENESS *Estimates Sources: - IMF – World economic outlook database: October 08 -Central Banks statistics

ECONOMIC ENVIRONMENT • Due to the negative impact of the global economy, GDP growth slowed down in all Southern African economies • Zimbabwe registered negative GDP growth for the tenth consecutive year • Commodity prices weakened significantly in sympathy with the global economic downturn • Banking assets however continued to grow, albeit at a slower pace • Botswana boasts the highest GDP per Capita and highest banking assets per Capita but other countries are making strides

ECONOMIC ENVIRONMENT • Average inflation was in double digit level ( except in Zimbabwe, where it was well in excess of this) • Generally all currencies weakened particularly in the second half of 2008 • Zimbabwe in a hyperinflationary environment; Last official inflation at 231m% in July 2008

ECONOMIC ENVIRONMENT– Inflation & Interest Rates * 90 day ** 1 year ***July 2008

ECONOMIC ENVIRONMENT– Exchange Rates • ZWD Old Mutual implied rate • ZWD revalued in 2008

ECONOMIC ENVIRONMENT– Exchange Rates • ZWD Old Mutual implied rate • ZWD revalued in 2008

NYSE Tokyo SE 4 3.9 3.6 3.1 1.4 1.9 2.4 9.2 4.3 Shanghai London Nasdaq 15.6 International Equity Market Cap, US$ Trillions

International Banks Market cap Source: Bloomberg, March 9th 2009

FINANCIAL PERFORMANCE • Overview • Income Statement Review • Balance Sheet Review

FINANCIAL PERFORMANCE - Overview • Attributable profit at BWP86m is down from BWP 124m in prior year • Net asset value up by 39% from BWP 314m to BWP B438m • Net interest income for financial operations up by 40% from BWP 127 m to BWP 178 m • Total income up to BWP 401m from BWP 339 million • Return on equity of 23% compared to 42% in 2007

FINANCIAL PERFORMANCE - Overview • Balance sheet growth of 38% to BWP 4 billion • Loans and advances up by 80% to BWP 2.2 billion, reflecting impact of Tier II capital injection • Deposits increased by 40% to BWP 2.8 billion

FINANCIAL PERFORMANCE: Attributable Profit per Subsidiary *Adjusted for minority interest & includes TDFL

INCOME STATEMENT REVIEW • All Banking operations profitable, except ABC Zambia • ABC Zambia’s poor performance due to a combination of high impairments and exchange losses in fourth quarter • Zimbabwe performance adversely affected by reduced investment income as economy reached meltdown point • Strong growth in total income in Botswana, Mozambique and Tanzania • Massive depreciation of the Zimbabwe dollar continued • Zimbabwe contribution to total income down to 15% from 35% • Quality of the book has marginally improved

INCOME STATEMENT REVIEW • NII increased by 72% to BWP 184m • NII contribution to total income increased from 32% to 42% • NII now covers 78% of total costs, up from 67% in 2007 • All banking operations, with the exception of Zimbabwe, showed significant growth in NII

INCOME STATEMENT REVIEW • Non-interest income declined by 7% to BWP 216m. • Investment income in Zimbabwe declined 78% from BWP 116m to BWP 26m • Impairment charge of BWP 44m up 35% compared to 2007. Botswana and Zambia most affected. • Operating expenditure increased by 48% to BWP 237m • Increased costs are largely due to additional staff for the new retail business and strengthening of credit department.

INCOME STATEMENT REVIEW – Total income* *Before impairments **Including TDFL

INCOME STATEMENT REVIEW – Net interest income *Including TDFL

INCOME STATEMENT REVIEW – Net interest income • Spread has increased across the board

INCOME STATEMENT REVIEW – Other income *Including TDFL

INCOME STATEMENT REVIEW – Total income composition Excluding impairments Increase in NII contribution due to increase in lending book NII income covers 78% of costs, up from 67% in 2007

INCOME STATEMENT REVIEW – Operating expenditure Due to retail banking roll out Cost containment strategy • Imperative to strengthen cost containment measures

INCOME STATEMENT REVIEW – Operating expenditure • Cost to income ratio up from 47% to 59% • Head count increased from 395 to 484 due to new retail banking and credit department staff • Employee costs accounted for 50% of total costs • Operating expenditure up 48% to BWP 237m • Marketing costs set to increase in support of growth targets and retail roll out

Head count per Operation • Total employee costs up 31% from BWP91m to BWP119 m • Employee costs 50% of total costs • Staff compliment of 484 (2007: 395) • Staff compliment up by 89 people mainly due to retail & credit

BALANCE SHEET REVIEW • Balance sheet growth of 38% to BWP 4 billion • Loans and advances up by 80% to BWP 2.2 billion, reflecting impact of Tier II capital injection • Deposits increased by 40% to BWP 2.8 billion • Net asset value up by 39% from BWP 314m to BWP B438m • Zimbabwe FCTR up BWP 95m in 2008

BALANCE SHEET REVIEW - Total Assets 38% balance sheet growth compared to December 07 sustained balance sheet growth since 2004 Compound annual growth rate of 23%

BALANCE SHEET REVIEW - Geographic split of deposits • 40% growth in Deposits • Botswana continues to lead with deposits of BWP 1.3 billion • Growth of 118% & 63% in Mozambique & Tanzania respectively; albeit from a low base

BALANCE SHEET REVIEW - Geographical Split of Loans • 80% growth in Loans. • Growth in excess of 48% in all countries except Zimbabwe • Growth shows impact of capital injection in late 2007

BALANCE SHEET REVIEW - Capital *Including Tier II **Including TDFL Zimbabwe FCTR up BWP 95m since Dec 07

BALANCE SHEET REVIEW - Capital Adequacy Healthy capital adequacy ratios

CAPITALISATION • Rights issue postponed as a result of the turmoil in the global financial markets • IFC subscription of 13.9 million shares, bringing shareholding to 10.7% in January 2008 • IFC convertible loan still to be drawn down as Group is in the process of clearing outstanding conditions precedent. Draw down imminent. • All conditions precedent on the CVCI convertible loan fulfilled. Drawdown in the coming weeks

RETAIL BANKING • Retail Banking head office now appropriately staffed • First few branches to be opened in July 2009 • Funds raised from IFC and CVCI to be used for capitalisation of this business • Largely driven by state of the art technology

DIVIDEND • Need to strengthen operations in the face of the uncertainty in global markets • Directors propose that a final divided be passed

OUTLOOK & CHALLENGES • Environment expected to be challenging during most of 2009 and 2010 due to a deterioration in the global markets • Major thrust will be consolidation and ensuring modest growth notwithstanding high costs as a result of retail banking • Proactive management of the loan book • Support clients in the face of adversity • Introducing fresh thinking and smart banking

OUTLOOK & CHALLENGES • Changing the business model –People, processes, systems and culture • Branch profitability still estimated to be between 12 to 24 months • Deposit mobilization remains a key focus area for the group, particularly in Zambia