Download

1 / 6

60 likes | 84 Views

This commentary explores the multifaceted impact of tax regulations on corporate governance dynamics with a focus on controlling shareholders. While corporate and securities laws play a significant role, tax implications, media pressures, and compliance also shape governance structures. Examining tax effects on corporate pyramids in North America and the UK reveals varying trends based on dividend tax policies and ownership structures. The historical context in the UK illustrates how tax incentives influenced ownership and control dynamics over the decades, shedding light on the evolution of corporate governance systems. The implications suggest a need for further research on tax's role in shaping governance practices and the interplay with regulatory frameworks.

E N D

Tax and Controlling Shareholders Brian R. Cheffins Comment: “Comparative Regulation” Transatlantic Corporate Governance Dialogue Brussels, June 27, 2006

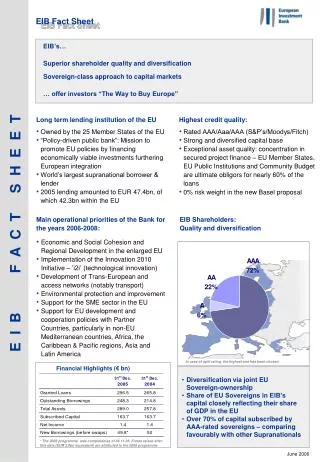

There is More to Regulation than Corporate/Securities Law • Research byLa Porta, López-de-Silanes and Shleifer and their co-authors has put corporate and securities law centre-stage in debates about the reform of corporate governance • But there is more to the story • Dyck and Zingales (2004), in their study of determinants of private benefits of control, found that while corporate law mattered, media pressure and tax (measured by compliance) mattered more • Tax merits further study

Tax and Corporate Pyramids in North America • The extent to which a country taxes dividends paid by one corporation to another influences the use of corporate pyramids: Morck and Yeung (2005) • In the US, New Deal tax reforms introduced taxation of intercorporate dividends and the use of corporate pyramids declined thereafter • Canada has a “group friendly” corporate tax structure as there is no tax payable on dividends distributed to a corporate blockholder • Blockholders and pyramids are common in Canada

Taxation of Corporate Dividends in the UK • Large U.K. companies are typically widely held and corporate pyramids are not a major concern • However, there is no US-style tax on intercorporate dividends (and there never has been) • On the other hand, when UK public companies have blockholders, the use of pyramids is as common as in the rest of Europe • Thus, the evolution of corporate ownership, not tax, displaced corporate pyramids as a cause for concern

Tax and the Unwinding of Ownership and Control in the U.K. • Tax helps to explain how ownership separated from control in the UK • In the 50s, 60s and 70s blockholders had a powerful tax incentive to exit: tax on income was punishing and capital gains were untaxed or taxed much more lightly • For individuals, institutional investment was tax favoured • This contributed to an institutional “wall of money” that was invested largely in shares • Institutional investor passivity in turn yielded the UK’s “outsider/arm’s-length” corporate governance system

Implications • Researchers should do more to find out about the impact of tax on corporate governance arrangements, including the status of blockholders • Using tax as corporate governance policy instrument is tricky • Nevertheless, we should seek to find out more about the extent to which tax is fostering or hindering efforts to use corporate and securities law to reconfigure corporate governance