Download

1 / 9

90 likes | 209 Views

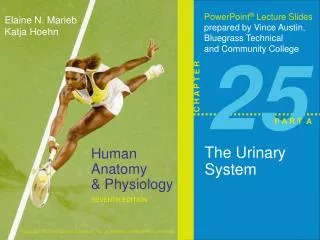

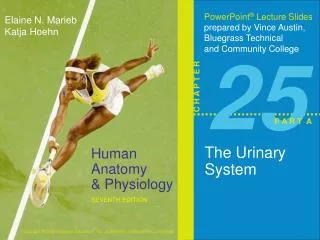

EXCESS D&O – What’s Up With That? . David Bell Senior Vice President Allied World Assurance Company, Ltd. Settlement Value of $40,000,000. $50m. $50m. 10x40. 10x40. 3.5. 7. 6.5. 3. $40m. 10x30. 10x30. 2.75. 5.5. 7.25. 4.5. $30m. 10x20. 10x20. 2. 4.

E N D

EXCESS D&O – What’s Up With That? David Bell Senior Vice President Allied World Assurance Company, Ltd.

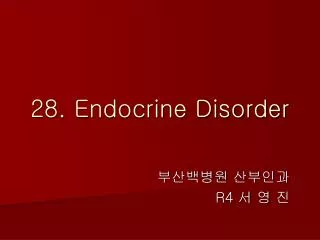

Settlement Value of $40,000,000 $50m $50m 10x40 10x40 3.5 7 6.5 3 $40m 10x30 10x30 2.75 5.5 7.25 4.5 $30m 10x20 10x20 2 4 50% or $20m Insured Contribution 20% or $10m Insured Contribution 8 6 $20m 10x10 10x10 1.25 2.5 8.75 7.5 $10m 0.5 $10m $10m 1 9.5 9 Deductible Deductible

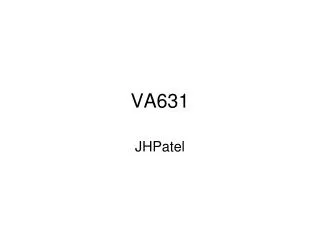

Settlement Value of $40,000,000 $50m $50m 10x40 7 3 $40m 10x40 10x30 6.5 5.5 10x40 Attachment Point for “Covered Loss” = $33.5m 4.5 10x30 7.25 $30m 7.25 10x20 4 50% or $20m Insured Contribution 8.00 10x20 6 8 $20m 10x10 2.5 8.75 10x10 8.75 7.5 $10m $10m 9.5 1 $10m 9.5 9 Deductible Deductible

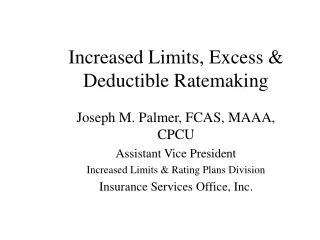

Settlement Value of $40,000,000 $50m $50m $50m $40m 10x40 6.5 10x40 Attachment Point for “Covered Loss” = $33.5m 10x30 $30m 7.25 10x40 Attachment Point for “Covered Loss” = $27m 3 10x20 10x40 8 10x30 4.5 $20m 10x20 6 10x10 8.75 10x10 $10m 7.5 $10m $10m 9.5 9 Deductible Deductible

Comparing 10x40 Limits Paid as a % of Primary to Premium $50m $50m 10x40 10x40 3.5 $158,203 75% 6.5 $40m 10x30 10x30 2.75 $210,937 75% 7.25 $30m 10x20 10x20 2 25% or $10m Insured Contribution $281,250 75% 10x40=31% of Primary Premium 10x40 limit paid is 68% of primary 8 $20m 10x10 10x10 1.25 $375,000 75% 8.75 $10m 0.5 $10m $10m 9.5 $500,000 Deductible Deductible

Problems with the Primary and High Excess Layers Being the Same Carrier $50m 10x40 10x40 $40m 10x30 $30m 10x20 10x20 $20m 10x10 Damage Analysis Of $15m Payout of $33m $10m $10m $10m Deductible

Not a “Loss” • legal fees and expenses incurred in connection with internal investigations or special litigation committee investigations; • expert and consulting fees incurred in connection with internal investigations or SLC investigations; • legal fees and expenses incurred in connection with government or regulatory investigations for all time periods prior to the date the investigation became or becomes a "Claim" under the primary D&O policy in question; • those portions of legal fees and expenses incurred in connection with non-covered matters or on behalf of non-covered parties. • legal fees and efforts spent on corporate transactional issues (such as indemnification) or in securing D&O coverage.

Change the Process • Broker should guide the insured’s counsel to keep separate files by functional activity. • If coinsurance is effectively the result, then do it from the start. • Claims Rep should send the pricing sheet at the first hint of a “work out”. • “Cram Down Letter”

Exhaustion • It is expressly agreed that liability for any covered Loss with respect to claims first made during the Policy Period or Discovery Period (if applicable) shall attach to the Insurer only after the Underlying Insurers have paid or have been held to pay the full amount of the Underlying Aggregate Limit above the applicable retention for such Policy Period. Therefore, in the event that the Underlying Insurers assert coverage defenses that result in an allocation or apportionment of covered Loss versus uncovered Loss, all covered Loss will be paid by the Underlying Insurers and the uncovered portion of the Loss will not erode the limits of the Underlying Insurers. This policy shall not pay until and unless all Underlying Insurers exhaust their available limits for covered Loss and any applicable Defense costs.