Download

1 / 38

390 likes | 1.22k Views

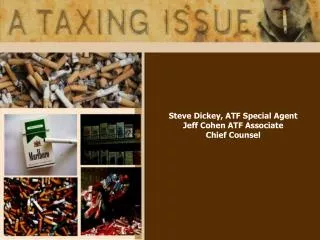

Steve Dickey, ATF Special Agent Jeff Cohen ATF Associate Chief Counsel. ILLICIT CIGARETTE TRAFFICKING. Steve Dickey ATF Special Agent Jeff Cohen ATF Associate Chief Counsel . Cigarette Diversion.

E N D

Steve Dickey, ATF Special Agent Jeff Cohen ATF Associate Chief Counsel

ILLICIT CIGARETTE TRAFFICKING Steve Dickey ATF Special Agent Jeff Cohen ATF Associate Chief Counsel

Cigarette Diversion ATF Enforces the Federal Criminal Laws Involving Illegal Cigarette Trafficking Including The Contraband Cigarette Trafficking Act (CCTA)

Cigarette Diversion The primary goal of a cigarette diversion scheme is to profit by evading State or Federal cigarette taxes. Criminals worldwide deprive Governments of 50 Billion Dollars a year through cigarette diversion. Cigarette diversion has been used to finance terrorist activities and organized criminal organizations. Cigarette smugglers have been implicated as Money Launderers for drug cartels. Cigarette diversion defeats Government Health Initiatives

Criminal Elements Involved • Latino/Italian Organized Crime (FL, NY, CA, NV, IL) • Eastern European Organized Crime (CA, WA, MD, VA, FL) • Middle Eastern Organized Crime (IL, MI, MN, WI, CA, NV, FL, NY) • Asian Organized Crime (TX, CA, OR, WA, FL, MI, IL, NY/NJ) • Mexican Organized Crime [Drug Cartels] (TX, KY, CA, FL, NY, NJ)

Types of Diversion • Diversion across state lines from low tax states to high tax states. State taxes on cigarettes range from 7 ¢ in South Carolina to $4.25 in New York City. • Cigarettes are smuggled between countries. • Untaxed Internet sales deprive state governments of millions of dollars. • Counterfeit cigarettes are produced in Asia and Eastern Europe and smuggled into the U.S. and other countries. • Untaxed cigarette sales on Indian reservations. • MSA Payment Fraud

Truck Hijacking Types of Diversion

Worldwide Cigarette Activity Countries with smuggling problems Countries used for Transit routes Countries with no smuggling problems Countries without Sufficient data recorded

Cigarette Tax Variance in the U.S. NYC, NY, NJ & WA are High Tax States SC, KY & VA are Low Tax States Traffickers can Earn $4.18 per Pack of Cigarettes by Diverting them from SC to NYC

Seattle Detroit NY & NJ Chicago San Francisco Los Angeles El Paso FTZ Miami and Port Everglades FTZs Laredo FTZ Primary U.S. Entry Points

US Customs Long Bch-Seizures of Counterfeit Cigarettes Declared As Other Commodities August 18th, 2001- November 9th 2002 Note: (11) of the (22) incidents came from Shanghai, China Port of Lading Source: U.S. Customs

Cigarette Packaging One Pack = 20 cigarettes One Carton = 10 packs = 200 cigarettes One Case = 60 cartons = 600 packs = 12,000 cigs CCTA Jurisdiction = 10,001 cigarettes = .8 case and 1 cigarette

Where Cigarettes are Sold Year End 2003 Native American 2.6% Supermarket Tobacco Stores 11.6% 14.9% Balance 13.9% Convenience Store 57.0% Source: IRI/Capstone Retail Panel

Criminal Schemes Involving Counterfeit Tax Stamps • Counterfeit tax stamps are brought into the U.S. for use by Organized Criminal Groups and groups possibly tied to Terrorist Organizations. • The Stamps are distributed throughout areas of California, New York, Massachusetts, New Jersey, Michigan, Illinois, Oregon, Texas and Florida. • The Stamps are then attached to contraband cigarettes purchased in low tax states with no tax stamps. • They are also attached to counterfeit cigarettes smuggled into the U.S. as well as diverted “for export” cigarettes.

Counterfeit California Tax Indicia Counterfeit California Tax Stamp, which was already attached to cigarettes, seized in Vancouver, Canada, on April 5, 2001.

Counterfeit New Jersey Tax Indicia Counterfeit NJ Tax Indicia intercepted at the border crossing point in Laredo, TX.

Cigarette Statutes • 18 U.S.C. § 2342 – Contraband Cigarette Trafficking Act makes possession of more than 10,000 unstamped cigarettes in a State which requires a tax stamp a felony. Possession of more than 500 units of other tobacco products in violation of State law • 18 U.S.C. § 2343 – If you distribute more than 10,000 cigarettes than you must keep accurate records pertaining to the shipment, receipt, sale and distribution of cigarettes – 3 yr felony • 18 U.S.C. § § 2314/2315 – Transportation & receipt of fraudulent state tax stamps is a felony

Cigarette Statutes • 18 U.S.C. § 2320 – Trafficking of counterfeit cigarettes is a felony. • 15 U.S.C. § 375 – Jenkins Act makes it illegal to ship cigarettes to a non-licensee in a State without notifying the State taxation authority. • The I.R.C. imposes a 39¢ per pack Federal tax and requires a permit for manufacturers and importers. • 26 U.S.C. § 5762 – failure to pay to the tax/illegal manufacture or importation of cigarettes.

Mail & Wire Fraud 18 U.S.C. §§ 1341 & 1343 • Purpose: To prevent the instrumentalities of interstate commerce be used to facilitate criminal activities. • Unlawful to use U.S. mail, wire, radio or T.V. in interstate commerce for the purpose of executing a scheme to defraud, including schemes to defraud the government of tax revenue. • Scheme need not be successful. • Penalty: Up to 5 years imprisonment & fines.

Mail & Wire Fraud Examples • In a scheme to transport cigarettes from NC to NY, phone calls made to a bank serve as the basis of wire fraud charge. • Wire fraud statute used to seize untaxed cigarettes offered for sale over the Internet. • Wire fraud statute used by ATF in scheme to defraud Canada of cigarette taxes during the 1990s when Canada raised taxes to discourage smoking and finance health care. • Mail fraud statute used to prosecute individuals who distributed untaxed cigarettes through the mails.

Currency Reporting Act • Currency transaction reports must be filed with the I.R.S. by businesses for currency transactions over $10,000. • To avoid government scrutiny, criminals in cigarette diversion cases often structure transactions to avoid the $10,000 level. • Structuring is unlawful. • Note that pursuant to Ratzlaf v. United States, 510 U.S. 135 (1994), the government, in a structuring case, must prove that the defendant knew the specific legal requirements of structuring statute.

Money Laundering • General purpose is to penalize the use of proceeds from one crime to facilitate another crime. • 18 U.S.C. § 1956 makes it unlawful to conduct or attempt to conduct a financial transaction which involves the proceeds of a Specified Unlawful Activity (CCTA, mail/wire fraud), with the intent to: • promote the carrying on of a SUA, or • to violate the IRC (tax evasion), or • to conceal or disguise the nature, source, or ownership or control of the proceeds of a SUA, or • to avoid a Federal/State transaction reporting requirement. Example: CCTA trafficker uses proceeds of CCTA violation to promote business by purchasing more cigarettes.

Simple Money Laundering • Engaging in monetary transactions in property derived from a specified unlawful activity. • 18 U.S.C. § 1957(a) makes it unlawful to engage in a monetary transaction with criminally derived property over $10,000. • There is no willfulness or intent requirement. Examples: Wire transfer of funds that are the proceeds of a CCTA scheme. CCTA trafficker deposits $10,001 of proceeds in the bank.

Racketeering Influenced & Corrupt Organizations (RICO) • Unlawful for a person who received income through a pattern of racketeering activity or an unlawful debt collection to: • use or invest the money towards any enterprise that affects interstate commerce (aimed at mob infiltration of legitimate business). • Unlawful for a person to be employed or associated with an enterprise which affects interstate commerce and to conduct a pattern of racketeering activity. • Unlawful to conspire in such activities. • Previously identified Federal crimes are a racketeering activity. • Used in cases where criminal organizations are engaged in large scale trafficking. • Note that a pattern of activities is 2 or more unlawful activities w/in 10 years, although AUSAs may require more.

Aiding & Abetting Whoever aids in the commission of a crime can be punished as the principal. This may include parties that knowingly supply traffickers.

Conspiracy • Conspiracy requires: • Intent to commit the crime • An act in furtherance of the crime • Crime need not succeed

Under Washington v. Confederated Tribes ofColville Indians, 447 US 134 (1980, Native Americans can possess and distribute untaxed cigarettes for tribal members personal consumption on the reservation. Natives Americans can also regulate and tax sales on the Reservation. All other Native sales are subject to State tax NATIVE AMERICAN ISSUES

Under S. Ct Attea case, States can regulate sales to reservation. CCTA is a statute of general applicability and applies to Native Americans. ATF believes that Jenkins Act applies to Native Americans With exception of Yakima Indians Right to travel Treaty, generally, treaties have not been defense to criminal violations by Native Americans. Native American Issues

Illegal manufacturing/Smuggling on St. Regis Reservation. Canada losing billion dollars in taxes Native American Issues

Seizure & Forfeiture Issues • For most violations involving smuggling/diversion, the conveyance used and profits gained are subject to seizure & forfeiture. • Conveyances and proceeds may be seized either civilly or criminally. • In certain instances, U.S. can sell cigarettes seized or confiscate proceeds associated with illegal cigarette trafficking and share the proceeds with participating State, local or foreign law enforcement agencies.

Civil Forfeiture • Divests property without prosecuting a defendant. • CAFRA applies – it requires that ATF notify the person from whom property was seized within 60 days and to then bring to court within 90 days of claim. • Two Types of Civil Forfeiture: • Administrative – used for property valued at less than $500k and where ATF has primary jurisdiction. • Judicial – used for property valued at more than $500k or where ATF has ancillary jurisdiction. • ATF Special Agent may be affiant in warrant. • Assets are deposited in Forfeiture fund.

Criminal Forfeiture Provides for a forfeiture count in indictments of persons charged with crimes.

Largest ATF Seizure /Foreign Internet Sales Otamedia/Yes Smoke Case

Cigarettes & Terrorism Mohamad Hammoud Immigration Fraud Guilty Immigration Fraud/False Statements Guilty Conspiracy to Smuggle Cigarettes Guilty Cigarette Smuggling Guilty Conspiracy to Money Launder Guilty Conspiracy to Commit Credit Card Fraud Guilty Credit Card Fraud Guilty Racketeering Guilty Conspiracy to Support Hezbollah Guilty Providing Support to Hezbollah Guilty Chawki Hammoud Conspiracy to Smuggle Cigarettes Guilty Cigarette Smuggling Guilty Conspiracy to Money Launder Guilty Credit Card Fraud Guilty Racketeering Guilty

Summary • ATF is committed to assisting State & foreign governments in fighting cigarette diversion and to preventing cigarette diversion proceeds from being used as a source of terrorist and organized criminal activities. • ATF is also committed to working with the business community to eliminate tax evasion and counterfeiting associated with cigarette diversion.