Download

1 / 67

670 likes | 951 Views

WEALTH TAX CHARGING AND PROCEDURAL ASPECTS. Nasik Branch of WIRC of ICAI 10 th May 2014 CA Abhijit Modi. Basic. The Wealth Tax Act came into force on 1 st April 1957. The Wealth tax Act, 1957 is applicable to the whole of India , including Jammu and Kashmir.

E N D

WEALTH TAX CHARGING AND PROCEDURAL ASPECTS Nasik Branch of WIRC of ICAI 10th May 2014 CA AbhijitModi

Basic • The Wealth Tax Act came into force on 1st April 1957. • The Wealth tax Act, 1957 is applicable to the whole of India , including Jammu and Kashmir. • The purpose of the introduction of Wealth tax Act: • To tax idle wealth and to de-motivate to hold idle wealth • To support the revenue collection • The Regulatory Body - CBDT

Wealth tax – Session plan • Session can be divided into two parts • The Charging provisions • The Procedural Provisions

Coverage of Wealth Tax • Charging Provisions • Section 2(ea) – Definition of an Asset • Section 2(q) – Valuation Date • Section 2(m) – Net Wealth • Section 3 – Charging Section • Section 4 – Deemed Asset • Section 5 – Exemption • Section 7 – Valuation of Assets

Coverage of Wealth Tax • Procedural Provisions • Section 14/14A/14B – Filing of Return of Net Wealth • Section 15 – Belated Return and Revised Return • Section 16 – Assessment • Section 16A – Reference to Valuation Officer • Section 17 – Wealth Escaping Assessment • Section 17A – Time Limit to Complete the Assessment • Section 17B – Interest for Late Payment and Late Filing of return • Section 18 - Penalties

Valuation Date (section 2(q) • The ‘valuation date’ means the last date of the previous year in respect of the assessment year for the purpose of income tax assessment. • Since the tax is charged on the net wealth of an assessee on the corresponding valuation date, the existence of assets on the valuation date is a necessary condition for the levy. • Where there is change of ownership of assets on the valuation date – Net wealth at the last moment of the day shall be the subject of assessment of Wealth Tax.

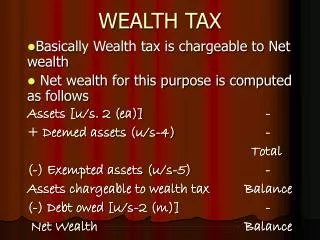

Section 2(m) – Net Wealth • "net wealth" means • the amount by which the aggregate value computed in accordance with the provisions of this Act (Schedule III – Valuation Rules) • of all the assets, (Section 2(ea) – Definition of Asset) • wherever located, belonging to the assessee (section 6) • on the valuation date, (section 2(q)) • including assets required to be included in his net wealth as on that date under this Act, (section 4 – Deemed Assets) • is in excess of the aggregate value of all the debts owed by the assessee on the valuation date which have been incurred in relation to the said assets. (Deduction allowed)

Section 3 – Charging Section • Every Individual, HUF and Company, • to pay tax @ 1% • on net wealth (section 2(m)) • exceeding Rs.30,00,000 • on the corresponding valuation date (section 2(q)) (No Education Cess prescribed on Wealth tax)

Other Assessee’s Wealth • Partnership Firm/LLP/AOP/BOI • As per section 3, Partnership Firm/LLP/AOP/BOI are not liable to pay wealth tax. • However, Rule 15 and 16 of the Valuation Rules as per Schedule III, prescribes the mechanism to club the net wealth of the Partnership Firm/LLP/AOP/BOI in the hands of partners/members in the proportionate manner.

Other Assessee’s Wealth • Section 21AA – AOP where share of members is unknown or indeterminate • wealth tax leviable in like manner and to the same extent as applicable to an Individual • thus, AOP has to be treated as individual, in such cases, and liable for tax.

Other Assessee’s Wealth • Trust • Any property held under trust or other legal obligation for any public purpose of a charitable or religious nature in India is exempt from Wealth Tax u/s 5. • Thus, any property held by a trust for the purpose other than a charitable or religious purpose, will be taxable, to the same manner and extent to an individual

Asset (section 2(ea)) • The definition of Wealth Tax is exhaustive (i.e. exclusive). Section 2(ea) defines an asset and contains 6 assets liable to wealth tax. Any asset owned, other than the six specified assets, as per section 2(ea) as on valuation date is not liable to wealth tax.

Section 2(ea) • 6 assets are covered and liable for Wealth Tax: • Building • Motor Car • Jewellery • Yachts, Boats and Aircrafts • Urban Land • Cash in hand

Building • Any building or land appurtenant thereto, • whether used for residential or commercial purposes or for the purpose or maintaining a guest house or otherwise, • including a farmhouse situated within 25 kilometres from local limits of any municipality (whether known as Municipality, Municipal Corporation or by any other name) or a cantonment Board, • but does not include:

Building • a house meant exclusively for residential purposes and which is allotted by a company to an employee or an officer or a director who is in whole time employment, having a gross annual salary of less than Rs.10,00,000/- • any house for residential or commercial purposes which form part of stock-in-trade. • any house which the assessee may occupy for the purpose of any business of profession carried on by him. • any residential property that has been let out for a minimum period of 300 days in the previous year. • any property in the nature of commercial establishments or complexes

Building • Definition of Building - not defined in the Act • General Dictionary meaning of Building: a structure with a roof and walls, such as a house or factory • Definition of Farm House – not defined in the Act • If reference is taken from Income Tax Act, 1961, farm house could be considered as - any building owned and occupied by the receiver of the rent or revenue of any such land, or occupied by the cultivator or the receiver of rent-in-kind, of any land with respect to which, or the produce of which, any agricultural process is carried on.

Building – Exemptions (Sec. 5) • any one building in the occupation of a Ruler, being a building which was his official residence by virtue of a declaration by the Central Government. • one house or part of a house or a plot of land (comprising an area of five hundred square metres or less) belonging to an individual or a Hindu undivided family.

Building • To sum up, following building are not taxable to Wealth Tax: • Any commercial building or part of the commercial building (irrespective of use) • Farm house situated beyond 25 kms from the municipality limits • Building held as stock in trade • Building used for business or profession • House property let out for 300 days or more during the previous year • Residential house owned by company and provided for accommodation to the employees drawing annual salary less than Rs.10,00,000 • One self occupied residential house (for Individual and HUF) • On residential house (palace) of Ex Ruler

Building - Valuation • Rule 3 to 8 of the Valuation Rules prescribe the procedure of Valuation of Building • Pegging Down value Concept • Deduction of Unearned Increase of Leased Assets • Adjustment for Excess of Un-built Area over a Specified Area. • If not covered by Rule 3 to 8, buildings has to be valued as per Residuary Rule 22 – (Market Value)

Building - FAQ • Is “Farm House” liable to wealth Tax? • Whether incomplete building is liable for wealth tax? • CIT v. Smt. Neena Jain (2011) 330 ITR 157 (P & H) • [2010] 189 TAXMAN 225 (KER.) Apollo Tyres Ltd. • [2007] 107 ITD 451 (COCHIN) Federal Bank Ltd. • Whether residential flat used for the purpose of business or profession liable for Wealth tax? • Tracstar Investments (P.) Ltd. [2008] 23 SOT 290 (MUM.) • [2009] 123 TTJ 945 (Mumbai)

Building - FAQ • Whether a temporary shed on plot be construed as asset liable for Wealth Tax? • Whether vacant shop, office, godown, warehouse, not being used for the purpose of business or profession be treated as an “asset” for Wealth Tax purpose? • Can assessee claim exemption of all the residential house properties for Wealth tax purpose? • Whether a house owned by the partner, which is being used for the purpose of business or profession by the partnership firm is also an asset?

Motor Car • other than those used by the assessee in the business of running them on hire or as stock-in-trade

Motor Car • Definition of Motor car – not defined under the Act • As per Webster’s Dictionary a motor car is an automobile which produces motion through the help of engine operating on gasolene. • Indian Rayon & Industries Ltd. [2002] 81 ITD 47 (MUM.)

Motor Car – Exemption (Sec.5) • No specific exemption provided for any type of Motor Car in Section 5.

Motor Car - Valuation • No specific rule provided for the valuation of Motor car in Schedule III – Valuation Rules • Thus, Residuary Rule 22 will apply (Market Value as on the Valuation Date)

Motor Car - FAQ • Whether the motor car used for the purpose of profession or business liable for Wealth Tax? • Whether the vehicles other than Motor cars are assets? • Whether buses and trucks are covered by the definition of an asset? Whether delivery vans or display vans will be covered by the definition of an asset?

Jewellery • Jewellery, bullion, furniture, utensils or any other article • made wholly or partly of gold, silver, platinum or any other precious metal or any alloy containing one or more of such precious metals, • Provided that where any of the said assets is used by the assessee as stock-in-trade, such asset shall be deemed as excluded from the assets specified

Jewellery • "jewellery" includes— • ornaments made of gold, silver, platinum or any other precious metal or any alloy containing one or more of such precious metals, whether or not containing any precious or semi-precious stones, and whether or not worked or sewn into any wearing apparel • precious or semi-precious stones, whether or not set in any furniture, utensils or other article or worked or sewn into any wearing apparel

Jewellery – Exemption (Sec 5) • Jewellery in the possession of any Ex-Ruler, • not being his personal property, • which has been recognised by the Central Government as his heirloom or the Board may, subject to any rules, recognise as his heirloom

Jewellery - Valuation • Rule 18 and 19 of Valuation Rules as per Schedule III • The value of jewellery shall be taken to the price which it would fetch if sold in the open market on the valuation date. • Return of Net Wealth shall be supported by – • A statement in the prescribed form where the value of jewellery on valuation date does not exceed Rs.5,00,000 • A Report of a registered valuer in the prescribed form where the value of jewellery on valuation date exceed Rs.5,00,000

Jewellery - Valuation • As per Circular No. 646 issued by CBDT, it has been decided that the report of the registered valuer obtained for one assessment year can also be used in the subsequent 4 assessment years subject to the adjustments of gold and silver rate applicable as on relevant valuation date.

Jewellery - FAQ • Whether missing jewellery is includible in the net wealth? • Is jewellery in the nature of “StriDhan” exempt from Wealth Tax? • Is silver utensils owned by assessee liable to Wealth Tax? • Is bullion kept as deposit (which bears interest) with the Jeweler be treated as an asset for Wealth Tax purpose? • Is gold and silver bought as ETF’s, bonds and on MCX Commodity be subject to Wealth tax?

Yachts, boats and aircrafts • Yachts, boats and aircrafts • (other than those used by the assessee for commercial purposes) • It does not include – Ship, Vessels, Cruise Lines

Yachts, boats and aircrafts – Exemption (sec 5) • No specific exemption provided for any type of Yachts, boats and aircrafts in Section 5.

Yachts, boats and aircrafts – Valuation • No specific rule provided for the valuation of yachts, boats and aircrafts in Schedule III – Valuation Rules • Thus, Residuary Rule 22 will apply (Market Value as on the Valuation Date) • Global Valuation of Business

Yachts, boats and aircrafts – FAQ • Any boat or yacht owned by the company for business purpose – marketing, advertisement purpose – be considered as an asset liable for Wealth Tax? • Any aircraft owned by the company for the Director’s personal use be subject to Wealth tax? • [2013] 37 taxmann.com 348 (Delhi) Jay Pee Ventures Ltd

Urban Land • "urban land" means land situate— • in any area which is comprised within the jurisdiction of a municipality (whether known as a municipality, municipal corporation, notified area committee, town area committee, town committee, or by any other name) or a cantonment board and which has a population of not less than ten thousand; or

Urban Land • in any area within the distance, measured aerially,— • not being more than two kilometres, from the local limits of any municipality or cantonment board referred to in sub-clause (i) and which has a population of more than ten thousand but not exceeding one lakh; or • not being more than six kilometres, from the local limits of any municipality or cantonment board referred to in sub-clause (i) and which has a population of more than one lakh but not exceeding ten lakh; or • not being more than eight kilometres, from the local limits of any municipality or cantonment board referred to in sub-clause (i) and which has a population of more than ten lakh,

Urban Land • but does not include land classified as agricultural land in the records of the Government and used for agricultural purposes or • land on which construction of a building is not permissible under any law for the time being in force in the area in which such land is situated or • the land occupied by any building which has been constructed with the approval of the appropriate authority or • any unused land held by the assessee for industrial purposes for a period of two years from the date of its acquisition by him or • any land held by the assessee as stock-in-trade for a period of ten years from the date of its acquisition by him.

Urban land – Exemption (sec 5) • one house or part of a house or a plot of land (comprising an area of five hundred square metres or less) belonging to an individual or a Hindu undivided family. • No other specific exemption provided for any type of Urban Land in Section 5.

Urban Land • To sum, following lands are not liable for Wealth tax: • Agricultural land (as per records and used for agricultural purpose) • Land situated in rural area (as per discussed territorial limits) • Stock in trade for less than 10 years • Land occupied by legally constructed building • Vacant land upto 2 years for industrial purpose • Land on which construction is not permissible (No development Zone) • Plot (Area less than 500 square metres)

Urban Land - Valuation • Rule 22 of the Valuation Rules as per Schedule III, specifically provides that the Urban Land shall be valued as per Market Value on the Valuation Date

Urban land - FAQ • Is agricultural land situated in “Urban Area”, liable to wealth tax; prior to A.Y 2014-15, where exemption has been claimed by the assessee and additions being made in the Assessment Orders? • [2013] 36 taxmann.com 547 (Amritsar - Trib.) BawaYadwinder Singh • Is N.A. plot used for the purpose of agricultural activities (produce) will be liable to Wealth tax? • Whether a land on which unauthorized building was being constructed, the construction of which has been stopped by local authorities, can be excluded from “asset” for the purpose of wealth tax on the ground that the construction is not permitted on such land? • DCM Ltd. [2005] 147 TAXMAN 42 (DELHI)

Urban land - FAQ • Whether incomplete building on urban land will be an asset for Wealth Tax purpose? • CIT v. Smt. Neena Jain (2011) 330 ITR 157 (P & H) • [2010] 189 TAXMAN 225 (KER.) Apollo Tyres Ltd. • [2007] 107 ITD 451 (COCHIN) Federal Bank Ltd. • Whether a piece of Urban Land, on which temporary shed is being constructed and used for the purpose of business, will be subject to Wealth tax? • [2012] 19 taxmann.com 29 (Delhi) Sohna Forge (P.) Ltd.

Urban land - FAQ • An assessee transferred its immovable property before its valuation date but the same was not registered in favor of the buyer. Can the same be included in the net wealth of the assessee on the ground that he still is the legal owner of the property? • Whether holding development rights for the land amount to asset as per Wealth tax? • [2006] 7 SOT 101 (MUM.) Irani Foods & Investment Co. (P.) Ltd. • Whether the Right to Purchase an asset (land) given by the Court amount to asset as per Wealth Tax Act? • [2010] 326 ITR 451 (BOM.) ArdeshirBehramDubash

Cash in hand • Cash in hand, in excess of fifty thousand rupees, of individuals and Hindu undivided families • and in the case of other persons any amount not recorded in the books of account.

Cash in hand – Deemed Asset (sec 4) • (5A) Where a gift of money from one person to another is made by means of entries in the books of account maintained by the person making the gift • or by an individual or a Hindu undivided family or a firm or an association of persons or body of individuals with whom or which he has business or other relationship, • the value of such gift shall be liable to be included in computing the net wealth of the person making the gift • unless he proves to the satisfaction of the Assessing Officer that the money has actually been delivered to the other person at the time the entries were made.

Cash in hand - FAQ • Does advances given in cash as on Valuation Date, which is found out by A.O., not to be genuine, subject to Wealth Tax? • Whether cash in hand held for business purpose liable for wealth tax (whereby, a valid evidence is produced to substantiate that the cash is held for business purpose)? • [2010] 229 CTR 52 (KER.) Smt. K.R. Ushasree • [2007] 13 SOT 446 (COCHIN TRIB) A.A. Salam • Whether cash held in Foreign Currency will be subject to wealth tax?

Deemed Assets (section 4) • In case of Individual, assets held – • by the spouse of such individual to whom such assets have been transferred by the individual, directly or indirectly, otherwise than for adequate consideration or in connection with an agreement to live apart, or • by a minor child, not being a minor child suffering from any disability of the nature specified in section 80U of the Income-tax Act or a married daughter, of such individual, • by a person or association of persons to whom such assets have been transferred by the individual otherwise than under an irrevocable transfer, • by the son's wife, of such individual, to whom such assets have been transferred by the individual, directly or indirectly, otherwise than for adequate consideration,

Deemed Assets (section 4) • An assessee who is a partner in a firm or a member of an AOP, there shall be included, as belonging to that assessee, the value of his interest in the assets of the firm or AOP determined in the manner laid down in Schedule III • An individual being a member of a Hindu undivided family, any property having been the separate property of the individual has been converted by the individual into property belonging to the family or been transferred by the individual, directly or indirectly, to the family otherwise than for adequate consideration