WEALTH TAX

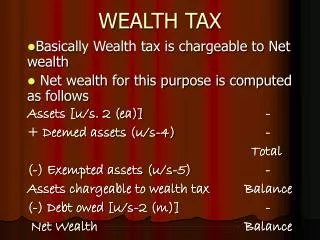

WEALTH TAX. Basically Wealth tax is chargeable to Net wealth Net wealth for this purpose is computed as follows Assets [u/s. 2 (ea)] - + Deemed assets (u/s-4) - Total (-) Exempted assets (u/s-5) - Assets chargeable to wealth tax Balance

WEALTH TAX

E N D

Presentation Transcript

WEALTH TAX Basically Wealth tax is chargeable to Net wealth Net wealth for this purpose is computed as follows Assets [u/s. 2 (ea)] - + Deemed assets (u/s-4) - Total (-) Exempted assets (u/s-5) - Assets chargeable to wealth tax Balance (-) Debt owed [u/s-2 (m)] - Net Wealth Balance

Net wealth is chargeable to wealth tax in the immediately following assessment year • Only an individual, HUF & a company is chargeable to wealth tax. • U/S-45, no wealth tax is chargeable in respect of Net wealth of ------ • Any co. registered u/s-25 of the companies act 1956 • Any co-operative society • Any social club • Any political party • A mutual fund specified u/s-10(23D) of the Income tax act

Net wealth in excess of Rs.15 lacs is charge- able to wealth tax @ 1%. • Companies registered u/s-25 of companies act, 1956 are known as Widely Held Companies • These are companies which are formed for the object of promoting • Commerce, art, science, religion, charity or • Any useful object, which apply such profits for promoting their objects & prohibit the payment of dividend to their members • All other companies are known as closely held co.

Assets [2(ea)] • Guest house, residential house or commercial building u/s 2 (ea) (i) • Any building or land whether used for commercial or residential purposes or for the purpose of guest house • A farm house situated within 25 k.m. from the local limits of any municipality or a cantonment board

Exceptions • If following conditions are satisfied • A house is not treated as “Assets”— • It is meant exclusively for residential purposes • It is allotted by a company to an employee or an officer or a director who is in full time employment • A house held as stock in trade • A house used for own business or profession

Motor Car-[u/s 2 (ea) ii] • For this purpose, “motor car” covers all motor vehicles other than heavy vehicles. Exceptions • Motor car used by the assessee in the business of running them on hire • Motor cars treated as stock in trade • In case of leasing company motor car is an asset Where an assessee had admittedly pur5chased a car, merely because in view of some dispute with seller it has not been registered in the assessee’s name, the assessee can’t plea that car is not includible in its taxable wealth

JEWELLERY, UTENSILSOF GOLD, SILVER etc. [u/s-2 (ea) (iii)] Any of such article made fully or partially of gold, silver, platinum or any other precious metal or Any alloy containing one or more of such precious metals are treated as “assets”

EXCEPTIONS • Stock in trade not an asset • Gold deposit bonds are not asset

BOATS and AIRCRAFTS[u/s-2 (ea) (iv)] Boats & Aircrafts are treated as Assets Other than those used by the assessee for commercial purpose

URBAN LAND [u/s-2 (ea) (v)] • An urban land is an asset whether it is agricultural land or non agricultural land. • It refers to a land situated in following areas: • Land situated within municipality area • Land situated outside municipality area (Not more than 8 k.m.)

EXCEPTIONS • On which construction of building is not permissible • On which construction is done with the approval of authority • Any unused land held by the assessee for industrial purposes for a period of 2 years from the date of its acquisition. • Any land held by the assessee as stock in trade for a period of 10 years from the date of its acquisition.

DEEMED ASSETS [u/s-4] • Assets transferred by one spouse to another [u/s-4(1)-(a)(i)] • Assets held by minor child • Assets transferred to a person or an association of persons. • Assets transferred under revocable transfers • Assets transferred to son’s wife

Continued….. • Assets transferred for the benefit of son’s wife • Interest of partner [u/s-4 (1) (b)] • Conversion by an individual of his self acquired property into joint property • Gifts by book entries • Property held by a member of housing society

ASSETS EXEMPT FROM TAX(u/s-5) • Property held under a trust • Interest in the property of HUF for a family member • Residential building of a former ruler • Former ruler’s jewellery • Assets belonging to the Indian repatriates Repatriate (send back to domestic country)

DEBT OWED (Due)[u/s/-2 (m)] • The following two conditions should be satisfied to get deduction of debt owed. • Only debt owed by the assessee on the valuation date is deductible. • Debts should have been incurred in relation to these assets which are included in net wealth of the assessee

VALUATION OF ASSETS[U/S-7] 1. Building (Part-B of schedule III)- Para 549.1 Step 1: Find out Gross maintainable rent i.e. • If property is let out • Annual rent received or receivable by the owner Or • Annual value of the property as assessed by local authority Whichever is higher

If property is not let out • Annual rent assessed by the local authority Or • (In case property is situated outside the jurisdiction of local authority) The amount which the owner can reasonably be expected to receive as annual rent had such property been let.

Step 2: Find out net maintainable rent • It is calculated by deducting following from step 1 • The amount of taxes charged by any local authority in respect of property And • A sum equal to 15% of gross maintainable rent

Step 3: CAPITALIZATION • Capitalization can be done by multiplying the net maintainable rent by a decided factor as per follows: • In case of construction on lease hold land factor should be 12.5 • In case of the lease period of such land is 50 years or more factor should be 10 • In case lease period is less than 50 years factor should be 8

Step 4:ADD PREMIUM • This step is to add premium to the step 3 • If the unbuilt area of the plot of land on which the property is built exceeds the specified area

For calculating premium following terms should be clear • Aggregate area: It refers to floor area (built/ unbuilt) • Unbuilt area: It refers to that part of aggregate on which no building has been constructed

Specified area: • Where the property situated at Mumbai, Kolkata, Delhi or Chennai 60% of the aggregate area • Where the property situated at Ahemdabad, Agra, Allahabad, Amritsar, Bangalore, Bhopal, Cochin, Hyderabad, Indore, Jabalpur, Jamshedpur, Kanpur, Lucknow, Ludhiana, Madurai, Nagpur, Patna, Pune, Salem, Sholapur, Surat, Tiruchirapalli, Trivandrum, Vadadora or varanasi 65% of the aggregate • For any other place 70% if the aggregate area

Calculation of Premium Excess of unbuilt area over specified area Premium Not more than 5% of aggregate area Nil 5% to 10% of aggregate area 20% 10% to 15% of aggregate area 30% 15% to 20% of aggregate area 40% More than 20% of aggregate area Rules of part-B Schedule III Not applicable

Step 5:DEDUCT UNEARNED INCREMENT • It is to deduct the amount of unearned increment payable • If property is built on leasehold land & any part of unearned increase in value is payable to the government or any authority at the time of transfer of the property, the value of such property will be reduced by the amount liable to be so paid.

2. Valuation of self occupied property -u/s-7 (2) • It is applicable if following conditions are satisfied. • The assessee owns a house, being an independent residential unit • It is used by the assessee exclusively for his residential purposes throughout 12 months If these conditions are satisfied, the assessee can adopt anyone of the following

Option 1 • He can take the value of a house as determined under part B of schedule III on the valuation date relevant for the current assessment year. Option 2 • Alternatively he take value of the house, as determined under part B of schedule III on the first valuation date on which he became the owner or the valuation relevant for the assessment year 1971-1972. which ever is later

3. Valuation of Assets of Business[Part D schedule III] • Value of assets disclosed in Balance Sheet Step 1:Find out following Assets Value Depreciable assets W.D.V. Non depreciable assets Book value (other than stock in trade) Closing stock Value adopted for the purpose of income tax

Step 2 • Add 20% the values given in above table Step 3 Find out the value of individual asset as per the provisions of schedule III Step 4 • If the value of step 3 > step 2 then the amount of step 3 will be taken as value • Else the value of step 1 will be taken.

Value of assets not disclosed in Balance Sheet • The value of an asset not disclosed in the balance sheet shall be taken to be the value determined in accordance with the provisions of schedule III as applicable to that asset.

4. VALUATION OF INTEREST IN FIRM OR ASSOCIATION OF PERSON • First of all determine the net wealth of the firm. (ignore the section-5) • This portion of net wealth, up-to the capital of the firm is allocated among the partners in the proportion of their contribution. • The rest is allocated among partners according to the agreement of the partnership for distribution of assets in dissolution or as per sharing ratio.

5. VALUE OF LIFE INTEREST(Part F, schedule III) Step 1: Find out “average net annual income” of the assessee desired for the life interest during 3 years ending on the valuation date. Step 2: Allow maximum 5% as collection charges.

Step 3: Average net annual income shall be multiplied by multiplier i.e. 1/(p+d)-1 Where, p = Annual premium for a whole life insurance without profit on the life of the life of tenant for unit sum assured. d = (i/1+i) as i being rate of interest which is 6.5% Thus the multiplier depends upon the premium for unit sum assured and age of the person having life interest. The multiplier i.e. [1/(p+d)-1], for different age may be checked through a pre calculated table

Numerical Problem • Mr. A aged 40 years. His father settled a house property in trust giving whole life interest to A. • The income form the property for the years 2005-06 to 2008-09 was 80000, 94000, 90000 and 96000 respectively • The expenses incurred each year were Rs. 4000, 6000, 7500, and 18000 respectively. • Calculate the value of life interest of A in the property so settled on the valuation date March 2009, on the assumption that the value of house as per schedule III is (a) 25 lakhs, (b) 8 lakhs • The multiplier at the age of 40 is 10.093

Solution • The average annual income for the period 2006-07 to 2008-09 Years 2006-07 2007-08 2008-09 Income 94000 90000 96000 (-) Exp (5%) 4700 4500 4800 Net Income 89300 85500 91200 Average annual income is 89300+85500+91200 = 266000 266000/3=88666.67 Thus the value of life interest 88666.67 X 10.093 = 894912.70

DECISION • Part (a) • The value of life interest of A in house will be taken as Rs. 894912.70 (as it is less than 16 lakh) • Part (b) • The value of life interest is Rs. 894912.70. • However the value of the house in respect of which A has interest is Rs 8 lakh. • Therefore value of life interest shall be taken as equal to Rs. 8 lakh (it cannot be more than value of the house)

6. VALUATION OF JEWELLERY • The value of jewellery shall be estimated to be the price which it would fetch if sold in the open market on the valuation date. The following points should be kept in view. • If value of jewellery less than Rs. 5 lakh • A statement in Form No. O-8A is required for return • If value of jewellery more than Rs. 5 lakh • A report of a registered valuer in Form No. O-8A is required to file a return.

7. VALUATION OF OTHER ASSETS • The valuation of an asset other than cash shall be estimated either by the assessing officer himself or by the valuation officer In both of these cases, the value shall be estimated to be the price which it would fetch if sold in open market, on the valuation date.

If the asset is not saleable in open market • The value shall be determined in accordance with guidelines or principles specified by the board from time to time by general or special order

Return of wealth and assessment • Every person is required to file with the wealth tax officer. • A return of net wealth in Form BA If his net wealth or net wealth of any other person in respect of which he is assessable under act on the valuation date is of such amount as to render him liable to wealth tax.

Return in response to a noticeu/s-17 • If any person, in the opinion of wealth tax officer, is assessable to tax, the wealth tax officer may, before the end of the relevant assessment year, issue a notice requiring him to furnish, a return of net wealth in prescribed form, within 30 days from the date of service of such notice.

Return showing wealth tax below taxable limit u/s-14 (2) • A return other than the return furnished in response to a notice u/s-17. • Which shows the net wealth below the taxable limit, therefore not chargeable to tax • It will be deemed never to have been furnished

Return after due date or amendment of return u/s-15 • If any person has not furnished a return within time allowed under section 14 (1) or 16 (4) (i) OR • Having furnished a return discovers any omission or any wrong statement. • He may furnished a return or revised return, as the case may-be. • Late return or revised return can be submitted within one year from the end of the assessment year or before completion of the assessment year whichever is earlier.

ASSESSMENT • Where wealth tax is payable on the basis of return to be furnished. • The assessee is required to pay the tax before filling of the return. • And such return is to be accompanied by the proof of such payment.

REGULARASSESSMENT • The Direct Tax Laws (amendment) Act, 1987 has amended the provisions regarding procedure for assessment. The new provisions have been brought on the lines of the income tax act.

RECTIFICATION • In case wealth tax authority commits any mistake while passing any kind of order, to rectify that mistake the wealth tax authorities have following powers: • Amendment of any order. • Any order to refund. • The valuation officer may amend its orders. • The joint Director, Commissioner, Commissioner (appeals), or Director may amend any of its order. • The appellate tribunal may amend any of its order.

APPEALS & REVISIONS • The appeal against the order of an assessing officer or revision of that order by commissioner of wealth tax is possible. • Filling of appeal to commissioner u/s-23A (1) / 2 Within 30 days from date of receipt of notice of demand or extended date. • Hearing & decision of the appeal by commissioner (appeals) u/s-23A (8A) Within a period of 1 year from the end of the financial year in which such appeal is filed, where it is possible.

Filling of appeal to tribunal u/s- 24 (1) / (2) Within 60 days from date of communication of order of deputy commissioner (appeals)/ commissioner (appeals) or within extended time. • Filling of cross objections with tribunal u/s- 24 (2A) Within 30 days from date of receipt of notice or within extended time. • Hearing & decision of the appeal by tribunal u/s- 24 (5A) Within a period of 4 years from the end of the financial year in which such appeal is filed, where it is possible

Filling application to commissioner for revision u/s- 25 (1) (c) Within 1 year from date of order sought to be revised. • Revision of order by commissioner u/s- 25 (1) (d) Within 1 year from date of order sought to be revised. • Revision by commissioner if considered pre-judicial to revenue u/s -25 (2) / (3) Within 2 years from the end of financial year in which order sought to be revised is passed.

Passing order by commissioner on application made by assessee for revision-u/s-25 (3A) Within 1 year from the end of the financial year in which application is made. • Application to tribunal from orders of enhancement by chief commissioner or director general u/s – 26 (1) Within 60 days from date of communication of order of Chief Commissioner or Director General.

Filling application to Tribunal for reference to High court u/s- 27 (1) / (2) Within 60 days from date of service of Tribunal’s order or within such further time no exceeding 30 days as allowed by Tribunal on sufficient cause • Filling appeal to High court by the assessee or Chief commissioner or commissioner u/s- 27 A Within 120 days of the day upon which he is served with notice of an order u/s-24 or 25 or 35 (1) (e)