Download

1 / 41

640 likes | 1.22k Views

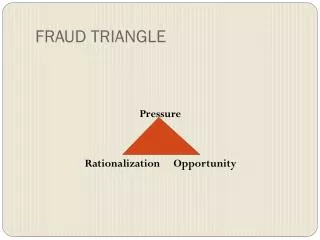

Internal Controls – The Fraud Triangle. Dennis Osuch, CPA - Partner Dennis Maschke, CPA - Manager. Objectives. What – Occupational Fraud . Occupational Fraud

E N D

Internal Controls – The Fraud Triangle Dennis Osuch, CPA - Partner Dennis Maschke, CPA - Manager

What – Occupational Fraud Occupational Fraud • The use of one’s occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization's resources or assets.

Asset Misappropriation Cash receipting

Fraud in State and Local Government “The auditor reported that the daily collections from the transfer station were not remitted to the county trustee for long periods, as long as 35 days, allowing the buildup of large sums. The auditor also found the receipts were not always issued in sequential order and there were numerous alterations made to the accounting records”

Solutions to Internal Segregation Difficulties Person A: Collect the cash, issue pre-numbered receipt to customer. Perform the month-end bank reconciliation Person B: Review and approve the cash collection form. Physically make the deposit.

Asset Misappropriation Payroll schemes

Payroll – Internal Control Recommendations (Continued) • Payroll reconciliations: • Comparison of paid checks to payroll registers • Payroll registers reviewed and approved before disbursement: • Names of employees • Hours worked • Wage Rates • Deductions • Unusual items • Payroll bank account should be reconciled by employee • Not involved in the preparation of payroll • Does not sign the checks • Does not handle the check distributions

Payroll – Internal Control Recommendations (Continued) • Distribution of payroll checks should be rotated periodically to different employees without prior notice • Distribution by employee other than department head or the person who prepares the payroll

Payroll Fraud • Annual Salary $68,307.82 • 2007 $122,888.62 • 2008 $195,440.58 • The accused took the money after he injured his back and became addicted to pain medication.

Asset Misappropriation Billing

Billing Scheme - Detection • Analytical Review • Inventory purchases in relationship to supply requests • Comparison with prior years and budget • Computer Assisted Analytical Review • Vendors & employees with same address • More the one vendor with the same address • Vendors with only PO box addresses • Vendor Complaints

The Impact of Hotlines

Dennis J Osuch, CPA • Partner • Dennis.Osuch@CliftonLarsonAllen.com • Dennis V Maschke, MBA, CPA • Assurance Manager • Dennis.Maschke@CliftonLarsonAllen.com