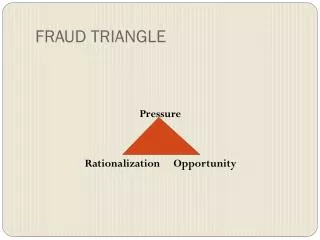

FRAUD TRIANGLE

FRAUD TRIANGLE. Pressure Rationalization Opportunity. FRAUD TRIANGLE. PRESSURES - :- Pressures that motivate individuals to perpetuate fraud on their own behalf can be divided into four types: Financial pressures Vices

FRAUD TRIANGLE

E N D

Presentation Transcript

FRAUD TRIANGLE Pressure Rationalization Opportunity

FRAUD TRIANGLE • PRESSURES - :- Pressures that motivate individuals to perpetuate fraud on their own behalf can be divided into four types: • Financial pressures • Vices • Work related pressures, and • Other pressures

Present scenario prevailing at Branches/offices of the Bank • Shortage of man-power • Heavy work load, compelled them to sit late hours for completion of the day-to-day affairs • High expectation of customer service • Pressure from customers, controllers • Political and VIPs pressure at Branches • Control by various departments • Business Pressure – Cross Selling • Too many meetings to be attended • Stress and strain experience at all levels • Inadequate time for Supervision and Follow-up • Lack of knowledge/Technical Skill in Computers and technology • Inadequate training, infrastructure etc.

PREVENTIVE VIGILANCE People can be classified in four distinct categories as follows:- • Honest and efficient • Honest but inefficient • Dishonest but efficient • Dishonest and inefficient

Legal Aspects of Bank Frauds (Dr. N.L. Mitra Committee) • In-house operations to legal compliance and certification process • Development of best practice code for observance of prescribed and professional code • In-house watchdog • Information networking between the member banks • Codification of standard audit practices on fraud and adults • Fraud defence networking • Special programmes for developing auditor’s consciousness on fraud and permissions and banks and financial institutions.

Role of Staff in Bank Frauds (Dr. N.L. Mitra Committee) The role of the staff can be divided and the three specific heads:- • Action taken with due diligence and in good faith • Action taken negligently without regard to due diligence, and • Transactions conducted in collusion

FRAUD PRONE AREAS - RBI • Deposit accounts • Issue/payment of the IOI and other transfer instruments • Discounting / purchase of bills • Letters of credit/guarantees and co-acceptances • Investments • Credit portfolio • Other common frauds

RECOMMENDATIONS OF STUDY GROUP B.D.NARANG COMMITTEE 1998 – LARGE VALUE BANK FRAUDS • Strictly adhere to KYC Guidelines • Bank credit policy focus on Review, Renewal and Enhancement of credit limits • Old borrowers account with large limits should be closely monitored • The status of the account and not the relationship with the customers should be the main criteria • Exchange of credit information on the customers with other banks in quantitative terms • Credit Information Bureau to be set up at the earliest • Each bank should have Fraud Management Policy • Management Audit should focus on Compliance of Systems and Procedures and effectiveness of Controllers in discharging control functions • Certain amendments to Criminal Procedure Code

KNOW YOUR CUSTOMERS • The Official has not taken care to ensure that KYC norms were complied with while authorizing opening 125 SB accounts for the employees of M/s.xxx Pvt. Ltd. and thus, he failed to avert perpetration of fraud • The Official failed to observe the following KYC norms while opening a new account at the branch in the name of M/s.ABC Limited’ • He did not verify/comply with KYC norms in respect of accounts in the List A • The official did not obtain KYC documents in respect of accounts listed in Annexure A. • You have not verified the PAN Card for its veracity

KNOW YOUR CUSTOMERS • You have opened the account No.X in the name of Shri.A on the basis of mere introduction by a third party. You failed to comply with the stipulated KYC requirements prior to opening of the account.

CRITICAL AREAS OF PREVENTIVE VIGILANCE VOUCHER VERIFICATION • Ensure generation of VVRs on daily basis • Ensure OVVR allotment and acknowledgement • Ensure checking of OVVR without fail. • Ensure the noting of vouchers missing in VVRs as well as Missing Voucher Register • Ensure the retrieval of missing vouchers or ensure preparation of duplicate voucher duly authorized by the official/staff concerned • Ensure second scrutiny of vouchers by the Branch Manger • Ensure safe keeping of vouchers at the Branch

CRITICAL AREAS OF PREVENTIVE VIGILANCE PASSWORD SECURITY • Minimum password length is SIX characters. Password to contain combination of one special character and one numeral among others. • Keep your password a secret. Do not divulge your password to any one at any time or period. • Change your password at regular intervals. • Change your password whenever User ID is “Reset”. • Ensure that there is no “THIRD EYE” watching your password and at any cost second person should not come to know about your Password. • Do not keep the same password to all the User IDs for Office/Personal Use.

CRITICAL AREAS OF PREVENTIVE VIGILANCE • Do not divulge your password to others for ECS uploading, Change of Vault Custodian and Clearing operations. • Ensure that your password is not used during your leave period / deputation to other Branches / Training etc., by others at your branch. • Please do not note your passwords in a dairy, piece of paper or store in mobile • Please advise your Controllers of any incidences of divulging your password which is beyond your control for confirmation purpose. • Password security has now become an area causing severe mental stress and creating an atmosphere of mutual suspicion in the work situation.

USER SYSTEM MANAGEMENT • Shri.XXX permitted Shri.YYY to work in a higher capacity with higher capability level in Core Banking system in contravention of the extant instructions without the approval of the Controllers. • He failed to reduce the rights of Shri.XXX, Single Window Operator, who was officiating as Cash Officer till then. • He failed to ensure that the User Control Register for change of powers given to various IDs was maintained by the Accountant as per laid down norms • You have failed to ensure the assignment of proper capability levels to the staff members as per user type and according to their work

SYSTEM SUSPENSE ACCOUNTS / RECONCILATION • The official did not ensure that the System Suspense-Rejected Trickle Feed Account was used only for transactions relating to Trickle Feed mechanism as this account was used indiscriminately for putting through various other transactions including a few cash transactions. The official did not ensure that the account was reconciled. • There was an unauthorized single side credit entry in System Suspense Rejected Trickle Feed Account for Rs. 6,50,000/- on 30.04.2008 purportedly posted by Shri XXX and checked by Shri.YYY The official did not verify the GLCOMP file generated on 30.04.2008. Had the official done this, the fraud would have come to light earlier.

SYSTEM SUSPENSE ACCOUNTS / RECONCILATION • He made a Debit of Rs.50,000.00 in Clearing Suspense Account and paid to a customer without any mandate and reversed only after 75 days when the amount was recovered from the borrower with OD interest • He utilized the Clearing Suspense Account for putting through the transactions in respect of loans sanctioned by him contrary to extant instructions. • The official has not ensured control of Branch System Suspense Account, Trickle Feed Account

SYSTEM SUSPENSE ACCOUNTS / RECONCILATION • You have not ensured zeroising System Suspense Accounts of on daily basis • He did not exercise any control over the reconciliation of all system related suspense accounts entries • He did not scrutinize the vouchers properly to identify the large debits to system suspense and office accounts.

DEPOSIT ACCOUNTS • He failed to stop the operation of the account once he came to know that the cheques book sent to the given address returned undelivered. • He arranged to issue the ATM card in the individual name of the proprietor when the base account is in a limited company’s name. • He allowed huge withdrawls of newly opened accounts with out making references through Cheque Referred Register • He has not made enquiries to the account holder regarding the first withdrawal of Rs. 5.00 lacs when the account holder was personally available at the branch • He failed to suspect the operations in the account as there were 11 with drawls of Rs. 1.00 lac and above in a short span of time in a newly opened account. • He authorized fraudulent transactions as mentioned in allegation 1 which resulted in the perpetration of fraud at the Branch

DEPOSIT ACCOUNTS • The Official neither obtained the Term Deposit receipts nor any letter from the holders of the receipt before authorizing premature payment of the TDRs • The Official failed to verify the signatures on the withdrawal forms, with the account opening forms or the signatures stored in the system, before passing the relevant withdrawal forms. • The Official failed to take adequate precautions like identifying the payee, enquiry about the source of large credits to a newly opened account, entering the debit in Cheque Referred and Returned Register for the first withdrawal of Rs 10 lacs on 01.02.10 from the Savings Banks Account No.xxx • The Official failed to verify the contents of the passbook submitted along with the withdrawal forms at the time of passing payment. • The Official failed to take adequate precautions while authorizing the payment of huge amount of Rs 10.26 lacs from TDR a/c on 30/01/2010 for credit of newly opened SB a/c to third party • You failed to enquire, record and report the high value credits and debits to the tune of Rs.27.36 lacs beyond the threshold limit in the account No.A

CASH DEPARTMENT • The Official has not verified the Cash Balance on a daily basis as laid down by the Bank. • The Official has failed to recount the cash sections of Rs.500/- and Rs.1,000/- denomination notes prepared by Sri.XXX, Special Assistant/ Cash officer (Offg), which has resulted in a cash shortage of Rs.41,000/- which was found out on 12.05.2004 • The Official has permitted withdrawal of large amounts from Safe at the time of opening of business on various dates particularly from April 2006 onwards, without any valid reasons or requirements. • He, as Joint Custodian has failed to conduct bi-monthly verification of cash balance.

CASH DEPARTMENT • He did not ensure that the cash held overnight by the SWOs did not exceed the overnight retention limit. • He did not take action when the caution display “NOT DONE” was seen on the screen when the cash held exceeded the day end retention limit fixed for the SWOs • He failed to conduct random verification of cash drawers of SWOs • He failed to conduct cash balancing on day-to-day basis for “Check Total” balancing. • He, as Joint Custodian has failed to conduct bi-monthly verification of cash balance. • Entries in the Cash jotting books, Cash Receipt Payment Register, Chest jotting books, were not authenticated by the joint custodians.

AUTOMATED TELLER MACHINE • Undelivered ATM cards and PIN Mailers are to be kept in two different individual custody. But both were held in the single custody of the officiating cash Officer at the Branch. He, as an Accountant failed to notice such irregularity and rectify it but allowed it to continue which made the task of the fraudster easy. • The Official’s gross negligence as Branch Manager/Joint custodian, in not following laid down systems and procedures relating to ATM led to a shortage of cash in ATM which resulted in a loss of Rs.55,38,900/- to the Bank.

AUTOMATED TELLER MACHINE • The Official did not ensure that the physical cash Balance in the ATM safe tallied with ATM admin balance on a daily basis and report the same to ATM switch centre. • The Official did not maintain the secrecy of the admin password that led to the loss to the Bank. • The Official did not ensure proper custody of the ATM Journal logs, which led to their loss in a fire that occurred at the Branch • The Official did not ensure preparation of vouchers for the cash replenishment transactions for ATM on all the dates ATM cash transaction took place.

AUTOMATED TELLER MACHINE • The Official did not maintain/update important control registers relating to ATM as required by the Bank. (Cash replenishment register, Back-up register) • He did not control and ensure that both the underlivered ATM Cards and Pin Mailer were in the custody of two different officials and allowed them to be in the single custody of Cash Officer, which is a violation of Bank’s laid down instructions, thereby he did not take steps to safeguard the interests of the Bank • Reconciliation of ATM Cash has not been done on a daily basis by the joint custodians as there was a difference in the ATM balance.

AUTOMATED TELLER MACHINE • ATM PIN Mailers were not properly handled / delivered by the official concerned • Slips containing Admin balance were not updated after 01.03.2009. • The PIN Mailer Register for ATM Pin Mailer and Returned ATM Pin Mailer was not properly maintained

CRITICAL AREAS OF PREVENTIVE VIGILANCE • ATMs - Joint Custodians ADMIN • Ensure security of the Admin Card and confidentiality of PIN. • Ensure PIN is changed periodically and whenever there is a change in incumbency. • Ensure Admin Function is carried out using the Admin Card whenever cash is replenished in ATM. • Ensure that photocopy of the Admin Balance enquiry slips are pasted in a register and are signed by both the joint custodians. • In case an official is holding multiple Admin Cards (for multiple ATMs), cards should be kept separately to avoid damage to the magnetic stripes. • Any "Cash Decrease" through "ADMIN Function" performed by the joint custodians should be approved by the Branch Manager and noted in the Cash Replenishment Register.

CRITICAL AREAS OF PREVENTIVE VIGILANCE CASH HANDLING • Ensure cash is placed in the ATMs as per "Opti-cash" recommendations received from the respective Management Centre. • Ensure that back-up register for cash replenishment is maintained. • Ensure that physical cash is verified, whenever cash is replenished and also, whenever complaint is received regarding non-dispensation or short dispensation of cash. • Account for cash found excess / short on the day it is detected. • Ensure that excess cash found in ATM is parked in Sundry Deposit account. • When a customer makes a claim, the amount can be refunded after proper enquiry. Such settlements should be done expeditiously. • Ensure that cash shortage located in ATM is parked in Suspense account on the same day and reconciled/reversed expeditiously. • Ensure that physical cash balance in the ATM tallies with the Admin Balance. • Report details of rectification entries put through in respect of the cash replenishment to controllers.

CRITICAL AREAS OF PREVENTIVE VIGILANCE • ATM Pin Mailer and ATM Returned Cards are handled by two different officials • PIN mailer is handed over to the Customer in person • ATM Pin Mailers Pending for 45 days are destroyed after proper approval • No person is allowed to handle the PIN Mailers other than the authorised person

CRITICAL AREAS OF PREVENTIVE VIGILANCE Advances • Is proper pre-sanction verification of the antecedents, information furnished by the applicant done to ensure the genuineness of the identity of the applicant and the purpose of the advance? • Are the opinion reports, brief or detailed as applicable, compiled on the applicant(s) and the proposed guarantor(s)? • Are the land records etc. examined by Bank’s Advocate to ensure defect-free title offered, accepting the particular landed property as security? • Is proper assessment/appraisal done to ensure financing of viable projects only as well as to check against over-financing? • Does the scheme financed come under an approved scheme of the Bank? • Are no-dues certificates from other credit institutions obtained to guard against multiple financing of the same person/project and multiple charges over the same assets?

CRITICAL AREAS OF PREVENTIVE VIGILANCE • Are phase-wise disbursements made as far as possible (within the overall sanctioned limit) depending upon the actual need at that stage? • Is it ensured that as far as possible cash disbursement is avoided and payments are made directly to the suppliers? • Are the purchase-receipts kept on record? • Is it ensured that the assets have been actually created? Is there an acknowledgement to this effect from the borrower? • Have the Bank’s charges been created in a valid manner? (For example, equitable mortgage is to be created only at the notified centres. • Is MOD Registered with Registrar of Assurances? • ROC Registration is completed? • The borrower is to give a declaration of ownership of stocks in respect of Special Hypothecation/Hypothecation/Pledge charges in addition to executing the Hypothecation Agreement. Certain charges are to be registered as per the Companies Act/ Transfer of property Act, etc.)

CRITICAL AREAS OF PREVENTIVE VIGILANCE • Are the Bank’s charge plates displayed prominently at all the important places of the factory/shop? In case of plant & machinery/vehicles, has the hypothecation charge been painted/engraved on the body of the equipment itself and registered with the R.T.O. for vehicles? • Are all the prescribed documents executed properly and kept on record? • Has the stock been insured to the extent of minimum 110% of the peak value of stock holding – to prevent the operation of the “Average Clause”. • Are the insurance/CGTMSE premia paid regularly? • Are correct rate/s of interest and other charges being levied?

CRITICAL AREAS OF PREVENTIVE VIGILANCE • Is it being ensured that the unit is not defaulting in payment of the Government dues like Sales tax, Income Tax/Customs/Excise duties, Electricity Bills, Land rentals etc.? • Are the stock statement and financial statements received as per the prescribed periodicity and veracity thereof checked properly during unit inspection? • Is proper care taken to verify the quality of the stock and the basis of its valuation? (For example, raw materials should be valued at landed cost or market price, whichever is lower; semi-finished/finished goods should be valued at not more than 95% of the market price). • Is the unit inspected as per the prescribed periodicity by the Field Staff and a record of the findings maintained? • Is it ensured that non-moving stocks, stocks purchased against Bank Guarantees etc. are segregated (excluded/ netted-off) while calculating Drawing Power to prevent double financing?

CRITICAL AREAS OF PREVENTIVE VIGILANCE • Are drawals allowed strictly as per the D.P. calculated on the basis of actual stock holding? • Is it ensured that undue enhancements in limits/overdrafts in personal account of the Proprietor/Partner/Director are not resorted to for regularisation of over-drawals? • Are the Control Returns submitted and the irregular features reported to the Controlling Office? • Are the documents revived in time? • Is circumspection exercised while passing cheques drawn on borrowal A/cs in favour of different parties to see the funds are not being diverted for other purposes? • Do the field staff keep a close watch over the borrowers’ activities in general to guard against diversion of funds or any other step by the borrower which will jeopardize the interests of the Bank?

CRITICAL AREAS OF PREVENTIVE VIGILANCE • Does the Branch Manager/Manager of Div. Inspect the units as per the prescribed periodicity to ensure that all advances have been made strictly as per the Bank’s laid down instructions and that no financing has been made to any fictitious person or for any non-existing unit? • Are review/renewals done in time? • Are notices sent and bad advances called up in time? • Is legal action initiated in time, pending suits followed up and execution proceedings effected in time for recovery of the Bank’s dues?

CRITICAL AREAS OF PREVENTIVE VIGILANCE Daily Reports to be verified by the AM/DM (Advances) • CC_OD Balance File • Loan Accounts Opened for the day Report • Overdue Loans • Review/Renewal Due Report • Insurance Expiry Report • Inspections Due Report • Failed Standing Instruction Report • Exception Report for Interest Rates • List of NPA Accounts • Probable NPA Accounts Report • List of Special Mention Accounts • Report on Agricultural Advances-CCOD.txt & DLTL.txt

AGRICULTURAL GOLD LOANS • The official has failed to adhere to the laid down system and procedures prescribed by the Bank in relation to the disbursement of the proceeds of agricultural gold loans. • The official has failed to observe the norms prescribed by the Bank by entertaining multiple agricultural gold loans to a single borrower for more than Rs.3.00 lacs • The official has failed to submit control forms for most of the Agricultural Gold Loans sanctioned • Delivery of gold ornaments without closure of accounts

AGRICULTURAL GOLD LOANS • He failed to verify Gold Loan sanction register/ledger pertaining to DBD and also failed to verify on random basis as Manager(DBD)that the gold loan accounts were properly authenticated by the joint custodians in the ledger, both at the time of opening and closing of gold loan accounts. • You have failed to maintain In & Out Register • You have failed to obtain a certificate from Gold Loan Appraiser of Approved panel as per the laid down instructions. • In his capacity as Manager of the Division, he failed to make and random verification for availability of gold loan documents. • He failed to interview all the gold loan borrowers before sanction of gold loans by him and also failed to ensure that the FO interviewed the gold loan customers before sanctioning of the gold loans by FO, for identification

AGRICULTURAL GOLD LOANS • He failed to ensure that the total number of gold loan bags, tallied with the loan accounts, by the joint custodians. • Periodical verification of securities not ensured as there was a shortage of Gold Loan bags • The System of joint custody of gold loan ornaments was not ensured. The Cash Officer was not subjected to the required checks. • Gold Loan ledgers were not scrutinized by the official as a surprise check. • He failed to ensure that the Joint custodian properly authenticated the gold loan accounts at the time of their opening and closing the details of a few accounts • The Cash Officer opened Gold Loan without proper sanction. He also passed debits manually as well as in CBS without the authorization of the other official.

ACC/KCC/ATL • He sanctioned and disbursed Agricultural loans in excess of the value as per the quotations submitted by the vendors • You have failed to create EM of collaterals offered • You have failed to inspect the land holdings offered as security for the loan limit • You have failed to obtain Chitta & Adangal for arriving the cultivable acreage of lands and the limit • You have sanctioned the KCC limits exceeding the Scale of Finance for the specified crops in respect of following accounts • You have arrived the KCC limits with out raising the crops in the aforesaid lands by the borrowers

ACC/KCC/ATL • You have failed to conduct a meaningful pre-sanction inspection for KCC/ACC loans sanctioned by you as per Annexure A • You have failed to verify the ownership of land holdings, Lease Holding etc. in respect of KCC/ACC loans sanctioned by you mentioned in Annexure A • You have disbursed the terms loans in cash against the laid down instructions in respect of ATL accounts mentioned in Annexure B • You have failed to obtain Bills/Receipts for the ATL limits sanctioned in respect of accounts mentioned in Annexure C • You have failed to verify the Chitta & Adangal with the VAO office as many ACC loans were sanctioned against the bogus Chitta & Adangal in respect of loans mentioned in Annexure B • You have failed to ensure the end use of funds and creation of assets purchased out of bank finance in respect of the ATL accounts mentioned in Annexure C

CAR LOANS • The official sanctioned 22 Car loans to borrowers when their existing loans were irregular/overdue. • Margin money for 4 car loan accounts has not been ensured • The official had not done Appraisal and sanctioned car loans in respect of the following loans which have been disbursed during August to December 2009 • Copy of RC Book evidencing RTO lien in favour of Bank was not obtained in the for 18 car loan accounts

MORTGAGE LOANS • You have sanctioned a mortgage loan for Rs.5.00 lacs the proposal which was earlier rejected by RACPC, Chennai. • He opened 9 Mortgage loans as Rent Plus or Gold Loans and repayments were fixed for principal only. • He sanctioned a Mortgage loan for Rs.5.00 lacs, against the property the value of which is Rs.3.00 lacs. • He had not conducted any pre/post sanction inspection in respect of 12 mortgage loans. • He failed to collect stamp duty and recital copies for Mortgage created at our ABC Branch for 12 Mortgage loans sanctioned by him at XYZ Branch. • He failed to insure the properties mortgaged to the Bank for 12 A/cs.

HOUSING LOANS • The Official processed and sanctioned six housing term loan accounts against bogus plan approval. • Housing loans were sanctioned / disbursed for purchase of house properties in far off places like Vellore, Gudiyattam where our branches are functioning. • The official committed serious irregularities without following Bank’s extant instructions governing various illustrated housing loans accounts sanctioned by him and thus failed to safeguard the interest of the Bank. • Loans were sanctioned without obtaining loan application signed by the borrowers • The official did not conducted proper inspection to verify the property financed by the Bank.

HOUSING LOANS • The official allowed various stage wise disbursements in the loan account without conducting proper inspection. • The purported guarantor of this HTL denied having executed the guarantee agreement • You have failed to obtain Supplementary legal opinion report • Required parental document was not obtained • Equitable Mortgage was not created • You have failed to adhere the instructions regarding Registration of Memorandum of Title Deeds

HOUSING LOANS • The official sanctioned the HTL for house construction. The estimate and work completion certificate evidenced that the loan was sanctioned for an existing house. • The official processed and sanctioned the loan proposals without obtaining ‘ No due certificate’. • The official processed and sanctioned the loan proposals without obtaining ‘ Post Dated Cheques’. • The official allowed debits and issued demand drafts without any specific • Mandate from the borrowers in HTL Accounts. • Housing Term Loan Limit of RS 50.00 lacs was sanctioned/disbursed to Shri.XXX who is not eligible for Housing Term Loan as his net income was Rs. 2,01,000/-. Further, EM was also not created. • Loan agreement and Arrangement Letters were kept blank in respect of the following 23 loan accounts

HOUSING LOANS • EMI/NMI ratio were not reckoned and loan amount in excess of their eligibility were sanctioned in the following 23 loan accounts • There were wide difference between Engineer’s certificate and actual construction levels in respect of the following 4 loan accounts • Loan amounts were fully disbursed without obtaining completion certificate in respect of the following 13 loan accounts. • He failed to obtain estimates for additional construction and approval from the appropriate authorities in respect of the accounts furnished in the Annexure B. • He sanctioned loans for the houses which are under construction, by takeover in respect of 3 accounts • He made assessment of the borrowers without obtaining details of existing loan accounts, status from banks/Financial Institutions during takeover of the HTL accounts • The official did not report to the controllers about the deviations in sanction of 61 housing loans mentioned in List A

CRITICAL AREAS OF PREVENTIVE VIGILANCE SERVICE CONDITIONS • Do not use your influence for securing any advantage for yourself or anyone related or known to you; it does not speak well of you. • Do not enter into any borrowing arrangement with any Bank except with the prescribed frame-work; it may amount to misuse of official position. • Do not make any false bills or make any attempt to falsify any account; it may cost your career. • Do not cultivate too close friendship with Bank’s contractors, suppliers etc; this may not be in your interest. • Do not take a decision in a case where you have interest or your relations are involved but let the files move without your intervention. • Avoid getting influenced by personal prejudices while disposing of files. • Do not relax while you are on invigilation or supervision duties.

CRITICAL AREAS OF PREVENTIVE VIGILANCE • Do not show any favouritism nor commit any irregularities in inviting tenders and awarding contracts; your reputation will be affected. • Avoid misuse of the Bank’s car or any other Bank’s property in your care. • Avoid taking or giving dowry in any circumstances, as this is against your conduct rules. • Never fail to seek prior permission for acquisition or disposal of immovable property of any amount; it may land you in difficulties • Never forget to report about the acquisition of movable properties within schedule time from the date of transaction, if the value exceeds Rs.25,000/-, or if the transaction is with a non regular dealer/ person obligated to the Bank.

For an effective role play of any assignment An officer must know • The work related to a particular assignment • The area/fields to be concentrated • The Systems and Procedures to be followed in respect of work related to assignment • The bottle necks and intricacies of the role; the ways and means to remove that • The Books/Registers to be maintained • Types of reports to be seen at periodical intervals and control aspects • How to maintain inter personal and intra personal relationship with their higher authorities/staff members • Art of good communication, correspondence etc.

PERCEPTION OF AN OFFICER Our Officers are generally regarded as • A good communicator • A good trainer • A good leader • A knowledgeable person • A well trained and experienced hand • A business achiever • A guide to the juniors • A helping hand to the higher authorities • Person rise above the level of expectation of the Bank at any time • Always maintain a good inter-personal and intra personal relationship with the staff members/members of various Government and Non-Govt. Agencies