Download

1 / 48

480 likes | 517 Views

Learn the importance of pricing, objectives, methods, costs, demand dynamics, and environmental factors in determining effective pricing strategies. Understand pricing elasticity, cost analysis, break-even points, and profit optimization. Enhance your knowledge of pricing in a practical business context.

E N D

Chapter Objectives • Explain the importance of pricing and how prices can take both monetary and nonmonetary forms • Understand the pricing objectives marketers typically have in planning pricing strategies • Describe how marketers use costs, demands, and revenue to make pricing decisions • Understand some of the environmental factors that affect pricing strategies

Chapter Objectives (cont’d) • Understand key pricing strategies • Explain pricing tactics for single and multiple products, and for pricing on the Internet • Understand the opportunities for Internet pricing strategies • Describe the psychological, legal, and ethical aspects of pricing

“Yes, but what does it cost?” • Price: the assignment of value, or the amount the consumer must exchange to receive the offering Money, goods, services, favors, votes, or anything else that has value to the other party

Step 1: Develop Pricing Objectives • Sales or market share objectives • Pricing strategy change to support a 5% increase in sales • Profit objectives • Prices should increase profit 8%..etc. important for Fad products. • Competitive effect objectives • Alter pricing to increase sales during competitors entering the market / maintain low-price to stop new entrants. • Customer satisfaction objectives • Match expectations/ simplify price structure to simplify decision making. • Image enhancement objectives • Reflect the increased emphasis on product’s quality image.

Step 2: Estimate Demand • Demand: customers’ desires for a product How much of a product are customers willing to buy as its price goes up or down?

Demand Curves • Law of demand: as price goes up, quantity demanded goes down. • For prestige products, a price increase may actually result in an increase in quantity demanded.

Shifts in Demand Curve Changes in marketing strategy (improved product, new advertising) or non-marketing activities can cause upward or downward shifts in demand. At a given price, demand is greater or less than before the shift.

Estimating Demand • Marketers predict total demand by estimating potential buyers for a product, then multiplying number of buyers times average amount of each buyer’s purchase. • Then they predict what the company’s share of the total market will be.

Price Elasticity of Demand • The percentage change in unit sales that results from a percentage change in price. Figure 11.5: Price Elastic and Inelastic Demand Curves

Elastic Demand • A change in price results in a substantial change in quantity demanded. - If price is increased, revenues decrease, and vice-versa. - Non-necessities (pizza) generate elastic demand. - Availability of close substitute products facilitates elastic demand.

Inelastic Demand • A change in price has little or no effect on quantity demanded. • If price is increased, revenues increase. • The demand for necessities (food and electricity) is generally inelastic.

Cross-elasticity of Demand • Changes in prices of other products affect a product’s demand. • Products are substitutes: increase in price of one will increase demand for other (bananas vs. strawberries). • One product is essential for use of second: increase in price of one decreases demand for other (increasing price of gas lowers demand for tires).

Step 3: Determine Costs • Variable costs: costs of production that are tied to and vary depending on the number of units produced. • Average variable costs may change as the number of products produced changes.

Figure 11.6: Variable Costs at Different Levels of Production

Step 3: Determine Costs (cont’d) • Fixed costs: costs of production that don’t change with number of units produced Rent, cost of owning/maintaining factory, utilities, equipment, fixed salaries of firm’s executives Average fixed cost: fixed cost per unit (total fixed costs divided by number of units produced) will decrease as number of units produced increases.

Step 3: Determine Costs (cont’d) • Total costs: total of fixed costs and variable costs for a set number of units produced.

Break-Even Analysis • A method for determining the number of units a firm must produce and sell at a given price to cover all its costs. • Break-even point: point at which a firm doesn’t lose any money and doesn’t make any profit.

Break-Even Analysis (cont’d) • Break-even point (in units) = (total fixed costs) divided by (contribution per unit) • Contribution per unit: the difference between the price the firm charges for a product and the variable costs • Break-even point (in dollars) = (total fixed costs) divided by [1 - (variable cost per unit divided by price)]

Marginal Analysis • A method that uses cost and demand to identify the price that will maximize profits. • Marginal cost: increase in total costs from producing one additional unit of a product • Marginal revenue: increase in total income or revenue from selling one additional unit of a product (decreases with each additional unit sold) • Profit is maximized where marginal cost is exactly equal to marginal revenue.

Marketing Math Activity • You and your friend have decided to go into business together manufacturing handbags. • --You know fixed costs will be $120,000 a year, and you expect variable costs to be $28 per bag. • --If you plan to sell the bags to retail stores for $35, how many must you sell to break even?

Step 4: Evaluate the Pricing Environment • The economy Broad economic trends Recessions, Inflation • The competition • Consumer trends

Step 5: Choose a Price Strategy • Pricing strategies based on cost Simple to calculate and relatively risk free Cost-plus pricing: total all product costs and add markup

PRICELINE.COM Step 5: Choose a Price Strategy (cont’d) • Pricing strategies based on demand • Based on estimate of quantity a firm can sell at different prices • Target costing: identify quality and functionality customers need and price they’re willing to pay before designing product. • Yield management pricing: charge different prices to different customers to manage capacity

Step 5: Choose a Price Strategy (cont’d) • Pricing strategies based on the competition • Pricing near, at, above, or below the competition • Price leadership strategy: industry giant announces price, and competitors get in line or drop out

Step 5: Choose a Price Strategy (cont’d) • Pricing strategies based on customers’ needs • Value pricing or everyday low pricing (EDLP): pricing strategy in which a firm sets prices that provide ultimate value to customers.

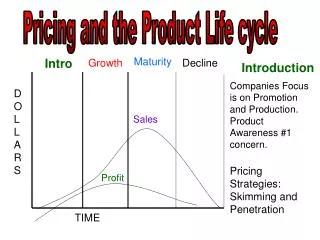

HP FINANCIAL CALCULATORS Step 5: Choose a Price Strategy (cont’d) • New-product pricing Skimming price: a very high premium price Penetration pricing: a very low price to encourage more customers to purchase Trial pricing: low price for a limited period of time

Discussion • In pricing new products, marketers may choose a skimming or a penetration pricing strategy. • --What is the advantage or disadvantage of this practice for consumers? • --For the industry as a whole?

Step 6: Develop Pricing Tactics • Pricing for individual products Two-part pricing: offering two separate types of payments to purchase the product Payment pricing: breaking total price into smaller amounts payable over time

Step 6: Develop Pricing Tactics (cont’d) • Pricing for multiple products Price bundling: selling two or more goods or services as a single package for one price Captive pricing: pricing two products that work only when used together

Step 6: Develop Pricing Tactics (cont’d) • Distribution-based pricing • F.O.B. (free on board) origin pricing • F.O.B delivered pricing • CIF (Cost, insurance, freight) • CFR (Cost & freight) • CIP (Carriage and insurance paid to) CPT (carriage paid to) • Basing-point pricing • Uniform delivered pricing • Freight absorption pricing

Step 6: Develop Pricing Tactics (cont’d) • Discounting for channel members • List price (suggested retail price): price that manufacturer sets as appropriate for end consumer to pay • Trade or functional discounts: set percentage discounts off list price for each channel level • Quantity discounts: reduced prices for purchases of larger quantities

Step 6: Develop Pricing Tactics (cont’d) • Discounting for channel members (continued) Cash discounts: enticements to customers to pay bills quickly (2% 10 days, net 30 days) Seasonal discounts: price reductions offered during certain times of year

CHEAPTICKETS.COM Pricing and Electronic Commerce • Dynamic pricing strategies: seller easily adjusts price to meet changes in marketplace. Cost of changing prices on Internet is practically zero. Firms can respond quickly and frequently to changes in costs, supply, and/or demand.

Pricing and Electronic Commerce (cont’d) • Online auctions (eBay.com) • E-commerce allows shoppers to purchase products through online bidding. • Pricing advantages for online shoppers • Consumers gain control. • Search engines and “shopbots” make customers more price-sensitive. • Consumers have more negotiating power.

Psychological Issues in Pricing • Buyer’s pricing expectation • Internal reference price: consumers use a price/price range to evaluate product’s cost. • Assimilation effect • Contrast effect • Price/quality inferences: consumers assume higher-priced product has higher quality.

Psychological Pricing Strategies • Odd-even pricing: prices ending in 99 rather than 00 lead to increased sales. • Price lining: items in a product line sell at different price points.

Legal and Ethical Considerations in Pricing • Deceptive pricing practices • Going-out-of-business sale • Bait-and-switch • Unfair sales acts • Loss-leader pricing • Unfair sales acts • Illegal business-to-business price discrimination

Discussion • In loss-leader pricing, retailers advertise and sell an item below cost to get customers into the store. • --Do you consider this an unethical practice? • --Who benefits and who is hurt by it? • --Should the practice be made illegal (some states have done so)? • --How is loss-leader pricing different from bait-and-switch pricing?

Legal and Ethical Considerations in Pricing (cont’d) • Price fixing: two or more companies conspire to keep prices at a certain level Horizontal price fixing Vertical price fixing • Predatory pricing: company sets a very low price for purpose of driving competitors out of business

Marketing Plan Exercise • A new seaside resort offers luxury rentals for a few days, a week, or longer. Consider possible pricing strategies -- cost-plus, yield management, everyday low pricing, skimming, and penetration and trial pricing. • --What pricing strategy do you recommend for the resort ? And why?! • --What pricing tactics do you suggest?