Download

1 / 45

450 likes | 574 Views

E N D

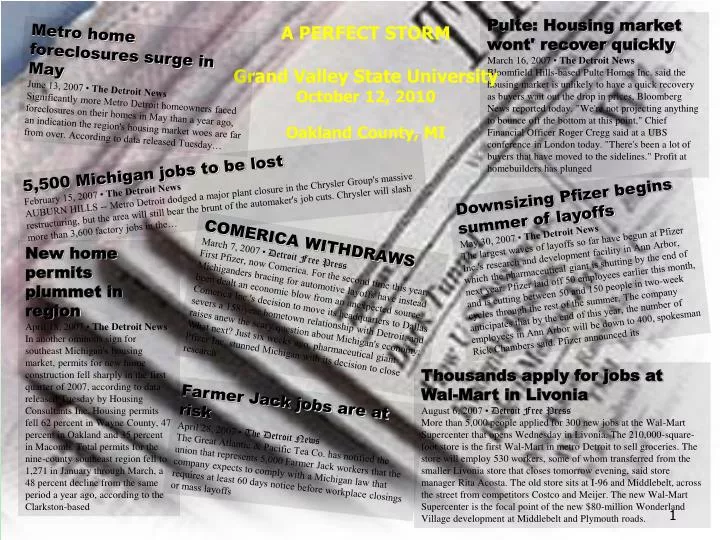

Pulte: Housing market wont' recover quicklyMarch 16, 2007 • The Detroit NewsBloomfield Hills-based Pulte Homes Inc. said the housing market is unlikely to have a quick recovery as buyers wait out the drop in prices, Bloomberg News reported today. "We're not projecting anything to bounce off the bottom at this point," Chief Financial Officer Roger Cregg said at a UBS conference in London today. "There's been a lot of buyers that have moved to the sidelines." Profit at homebuilders has plunged A PERFECT STORM Grand Valley State University October 12, 2010 Oakland County, MI Metro home foreclosures surge in MayJune 13, 2007 • The Detroit NewsSignificantly more Metro Detroit homeowners faced foreclosures on their homes in May than a year ago, an indication the region's housing market woes are far from over. According to data released Tuesday… 5,500 Michigan jobs to be lostFebruary 15, 2007 • The Detroit NewsAUBURN HILLS -- Metro Detroit dodged a major plant closure in the Chrysler Group's massive restructuring, but the area will still bear the brunt of the automaker's job cuts. Chrysler will slash more than 3,600 factory jobs in the… Downsizing Pfizer begins summer of layoffsMay 30, 2007 • The Detroit NewsThe largest waves of layoffs so far have begun at Pfizer Inc.'s research and development facility in Ann Arbor, which the pharmaceutical giant is shutting by the end of next year. Pfizer laid off 50 employees earlier this month, and is cutting between 50 and 150 people in two-week cycles through the rest of the summer. The company anticipates that by the end of this year, the number of employees in Ann Arbor will be down to 400, spokesman Rick Chambers said. Pfizer announced its COMERICA WITHDRAWSMarch 7, 2007 • Detroit Free PressFirst Pfizer, now Comerica. For the second time this year, Michiganders bracing for automotive layoffs have instead been dealt an economic blow from an unexpected source. Comerica Inc.'s decision to move its headquarters to Dallas severs a 158-year hometown relationship with Detroit, and raises anew the scary question about Michigan's economy: What next? Just six weeks ago, pharmaceutical giant Pfizer Inc. stunned Michigan with its decision to close research New home permits plummet in regionApril 18, 2007 • The Detroit NewsIn another ominous sign for southeast Michigan's housing market, permits for new home construction fell sharply in the first quarter of 2007, according to data released Tuesday by Housing Consultants Inc. Housing permits fell 62 percent in Wayne County, 47 percent in Oakland and 35 percent in Macomb. Total permits for the nine-county southeast region fell to 1,271 in January through March, a 48 percent decline from the same period a year ago, according to the Clarkston-based Thousands apply for jobs at Wal-Mart in Livonia August 6, 2007 • Detroit Free Press More than 5,000 people applied for 300 new jobs at the Wal-Mart Supercenter that opens Wednesday in Livonia. The 210,000-square-foot store is the first Wal-Mart in metro Detroit to sell groceries. The store will employ 530 workers, some of whom transferred from the smaller Livonia store that closes tomorrow evening, said store manager Rita Acosta. The old store sits at I-96 and Middlebelt, across the street from competitors Costco and Meijer. The new Wal-Mart Supercenter is the focal point of the new $80-million Wonderland Village development at Middlebelt and Plymouth roads. Farmer Jack jobs are at riskApril 28, 2007 • The Detroit NewsThe Great Atlantic & Pacific Tea Co. has notified the union that represents 5,000 Farmer Jack workers that the company expects to comply with a Michigan law that requires at least 60 days notice before workplace closings or mass layoffs

Presentation Overview – A Perfect Storm Take Aways. Financial Issues – State / Regional: Employment / Credit Crunch. Automobile Industry Issues. State Finances / Budget Issues. Foreclosures / Real Estate Market. Regional Financial Issues. Summary.

TAKE AWAYS • Credit market stressed (i.e. cash flow as in TANs); bond ratings troubled; competition by local units of government for limited operating cash for distressed communities is becoming increasingly difficult to obtain – and the regional economy remains weak. Cash flow weak points – March through April for State, cities, many counties, and school districts. • Federal government –feds cannot afford to solve states’ structural operating problems longer term. Michigan obtained $3.8 billion of federal stimulus funds for FY- 2009, 2010 and 2011 to balance budget. Feds added a ‘one-time’ $700M grants to State – alleviating the fiscal problem, temporarily. Had the feds not provided $4.5 billion, the State would have been compelled to increase taxes and / or reduce expenses – much of which flow to the local units of government. • Impacts on government revenues have yet to reflect GM, Chrysler and 54 supplier bankruptcies for 2008 / 2009 jobs losses, economic stagnation, and property value declines. Job losses take 2-plus years before they work their way through the real estate market. Oakland County just revised its job losses in 2009 to 60,000 lost – will impact 2012 property values. Somewhat mitigated with minor unemployment improvements in 2010.

TAKE AWAYS – (Cont.) • State leadership has not addressed fiscal issues or provided fiscal stability for local governments. State has no long-term fiscal plan. 2010 budget hole remains unresolved. 2011 budget unresolved. Fund equity declining fast. Cash flow needs substantial. Unfunded retirees’ healthcare obligations over $45 billion today (with no discussions as to how to resolve this obligation underway). Pension contributions, which have not been fully funded in the past decade, will be further impacted by recent investment declines. • Even as the 2011 operating budget is being finalized, the Senate Fiscal Agency as announced that there is a $1.6 billion operating shortfall for 2012, before considering retirees’ healthcare contributions and other matters. This shortfall is a ‘floor’ – it will be no less than this amount. Look to the January 2011 revenue estimation committee for further fiscal issues upon closing the accounting records for FY-2011. • Local governmental units receive 56.2% of State revenues collected in order to provide programs directly to the public. Largest State distributions are to school districts / ISDs.

TAKE AWAYS – (Cont.) • New programs / tax requests requiring tens of billions in competition with existing service levels that are being reduced. Priorities – keep existing core services solvent OR launch new programs (should not start “new” programs while the “old” programs are not stabilized): • Regional transit: $10 billion in capital expansion for rail system to be paid over a 25-year period with no complete capital and operating funding yet identified. SMART and DDOT financially stressed. • Road maintenance, bridges, highways, etc – billions in new gas taxes requested. • Water / drain projects – compliance with federal and State regulations. • Second USA / Canada bridge (DRIC) under consideration in Lansing - cost of $5 billion. Now, there is discussion of a new arena for the Detroit Pistons as well. • School system that is failing under Proposal A with declining property values and school districts heading into deficits (liabilities over assets to pay them). • Social program needs increasing – child care, domestic abuse, homeless, etc.

TAKE AWAYS – (Cont.) • New / existing programs requiring funding – continued: • Police /fire /EMS reductions. State revenue sharing reduced . Prisons being closed; felons released in State with high unemployment. State-wide – 2,035 fewer police in 2010 than in 2001. • Local governments fiscally troubled (e.g., going into deficit; struggling with cash flow issues; budget issues; etc.). • Uncertainty at the federal level on impacts of programs on businesses and citizens – healthcare; cap and trade; financial reforms; stimulus (what next when it runs out?); other. • Many fiscally-troubled local governments trying to borrow with low credit ratings and a banking industry reluctant to lend. • If the local governmental units cannot provide the services at levels that the public has become accustomed to, how can new programs be started (particularly when no new funding is likely) when they can’t even fund core services (police, fire, schools, etc.)?

NOTABLE NATIONAL EVENTS • March 2010, U.S. treasury and Berkshire Hathaway (e.g. Buffet) each went out for short-term notes. Warren Buffet received a better interest rate than USA. • FY-2010 Social Security operations will require the federal government to begin paying back the $2.5 trillion it owes for the first time in history. Projected amount needed by the Social Security for operations is $29 billion. The lock box is unlocked. Likely caused by unemployment and lower payroll taxes. • Moodys, a bond rating agency, has raised the specter of reviewing the bond ratings of the USA with the potential of lowering it from AAA. Particularly with European sovereigns imploding (Greece; Portugal; Spain; etc.). • California still facing $19.1B operating shortfall starting July 1, 2010 and has passed no budget (will banks lend to cover cash flow?). Pension plan - $500B in unfunded obligations – properly funding it would require half of that State’s budget. California (sans USA) is the 5th largest economy in world – will impact the nation’s ability to solve its fiscal issues. • Illinois in deep fiscal problems – can’t raise cash to operate. Vendors are going under as a result waiting for Illinois payments.

State Economy – Employment • If no job, can’t pay mortgage. Home foreclosed. Glut of homes. Economics 101 – increasing inventory, declining demand – prices fall. Property tax revenues have been the most stable local revenue – comprising 50% to 70% of local government revenues. • State unemployment: August 2010–13.1%. UM predicts 13.7% at end of 2011. • National unemployment roughly 10.0% (16M unemployed). Excludes 1.4M unemployed no longer seeking work and 9M who are under-employed. Productivity gains without rehiring results in a jobless recovery (no reason to hire if productivity is improving without employees). • Since 2000, Michigan lost 50% of the private sector jobs in the nation. Of all states, Michigan was last in GDP growth and not by a small margin. • Oakland County unemployment in Dec. 2009 – 13%. Detroit (June 2010) – 24%. Pontiac (June 2010) – 31%. New Orleans (post Katrina) – 11%. • Unemployment Trust Fund (UTF): Sept. 30, 2001, UTF had $3.0 billion in equity (assets in excess of liabilities). Sept. 30, 2009, $2.4B deficit (liabilities > assets). UTF outstanding borrowing from the federal government at Sept. 30, 2009 - $2.7 billion.

State Economy – Employment / Other • During 2009, State borrowed at a pace of $200M monthly (now at roughly $100 million per month pace). In September 2010, the amount borrowed was announced at $3.8 billion (half of the annual General Fund revenue budget). • Fall 2009, new payroll tax imposed: $21 / employee. $2.8B / $21 per employee x 3.85M employees = 33 years to resolve (before interest costs). Borrowing continues to increase the problem. Tax increases controlled by federal government. Similar increase expected in fall 2010. • Each year until paid, it will incrementally add roughly $21 / employee in new taxes or about $84M annually until resolved. Fall 2010, they will start collecting $168M; in 2012, $272M and so on. However, the interest due on the outstanding $3.8 billion will be around $150 million – meaning virtually none of the principal will even be repaid with the two tax increases (it will only cover interest owed to federal government). • Payroll taxes are barriers to employment growth particularly for lower paid employees. Payroll taxes will grow as the UTF borrowings increase. • Borrowing will stop when businesses start hiring again, but it will be a decade or so before the borrowed UTF debt is paid back to the federal government.

Auto Industry - Barriers • Operations – cash declines caused by operating losses weakened Detroit 3 and suppliers over past decade - $100 billion in operating losses since 2000. GM / Chrysler / Ford have lowered fixed and legacy costs and capacity. Toyota recalls help Detroit 3 auto companies in short term but profitable in 2010. Ford / GM– substantial profits for 2010 so far. • Legacy Costs (Pension / Retirees’ Healthcare) – unfunded retirees’ healthcare of Detroit 3 at December 31, 2005 - $113 billion. Current unfunded pensions, as estimated by PBGC, is $77 billion. Some retirees’ paid dearly in bankruptcy; some impacts still coming. Retirees’ healthcare liabilities are now part of equity for new GM / Chrysler. How does equity pay medical bills? New company value needs to grow and then stock sold for cash to pay benefits. • Mileage (Emission) Standards – tens of billions in required research and development over the next decade. Operating losses do not provide sufficient cash for R&D. R&D to be recovered when cars yet in production are brought to market (now offset by federal income tax credits). New federal mileage standards in March 2010 - requires design completion by 2014 and product launch no later than 2016 to comply on technology still being developed.

Auto Industry – Mileage Emission Standards • Mileage (Emission) Standards – will public buy more costly, fuel efficient cars. Remains an open question at increased prices to cover R&D costs: • Recent President’s fleet standards at 34.1 MPG by 2016 is estimated to cost $25 billion. Engineering needs to be completed NLT 2014 for 2016 production. • 138M vehicles owned in U.S.; now 12M replaced annually; will take generation to replace ‘gas guzzlers.’. Yet, only 2% of vehicles sold are considered ‘green vehicles’. • China rated number 1 polluter in the world; India number 5 – both rejected Sec. of State Clinton’s request to impose environmental standards. China now sells more vehicles in China than USA sells in USA (with lesser pollution standards on their vehicles). Do polar bears really care who pollutes? • No road taxes levied on electric vehicles – gas and weight taxes are imposed on gas / diesel and restricted for road maintenance. Shifts to more fuel efficient vehicles and those not having the tax will – in the short term – reduce road revenues and thereby, road repairs and maintenance. More efficient cars / trucks use less gas – less taxes – and electrical cars use NO taxed services for road maintenance. Taxing structure will have to change – see prior discussion on road maintenance caused by insufficiency of revenues.

Auto Industry – Other Barriers • Vehicle Production - production ‘pie’ is getting smaller (fewer units produced) at a time when the slices for Big 3 are getting smaller (market share reduced): • Calendar 2007: 16.1M light vehicles sold (8.1M by Detroit 3). • Calendar 2008: 13.2M vehicles sold (6.2M by Detroit 3). • Calendar 2009: 10.3M vehicles sold (4.5M by Detroit 3). • Calendar 2010: est. 11.6M vehicles to be sold (5.0M by Detroit 3). • Calendar 2011: est.12.7M vehicles to be sold (5.3M by Detroit 3). • Until 2008, lowest number of Detroit 3 vehicles sold was in 1981/82 – 7.6M vehicles. 2010 estimates are 2.6M lower than previous low. • Detroit 3 production will adversely impact Michigan’s personal income taxes; MBT; and sales taxes – sales taxes are a key component to local government revenue sharing and particularly school district distributions.

Auto Industry – Other Barriers (Cont.) • Federal Loans / Ownership: • Feds invested heavily in GM / Chrysler / parts suppliers through loans, now converted to equity. Federal government and UAW are principal owners. • Federal government regulates an industry (such as emissions standards) that it now owns. Fed now owns and regulates. Feds are now responsible to resolve the emission regulations impacts they have now imposed on companies they own (income tax credit). • Emission regulations could adversely impact UAW jobs. Puts current federal administration in an awkward position. UAW’s goal is to protect jobs and compensation. • Federal government has asserted a ‘hands off’ running auto companies. However, federal House passed legislation to reinstate dealerships. Rep. Barney Frank – closing of GM distribution center rescinded. GM chairman terminated by President. Pay rates for top 25 company officials set for 7 companies (including GM / Chrysler). Congress forced discussions on dealership closings. Political decisions versus business decisions in running auto companies. • Future subsidies / continued federal loans, if needed, to new GM / Chrysler – privately provided loans may be difficult to obtain given the recent reductions taken by secured creditors while unsecured creditors (UAW OPEB obligations) received a higher priority in the bankruptcy actions.

Auto Industry – Other Issues • The “old” Chrysler (i.e. company still in Chapter 11) has over $10 billion in identified liabilities but only $2 billion in potential assets. Some entity (banks?) likely has taken write-offs from these uncollectible receivables from Chrysler. • Bankruptcy – GM / Chrysler – all problems are not solved. For example, close-down of GM plants left in the ‘bad companies’ result in $530 million in environmental issues (President contributing $800M towards environmental clean-up). ‘Bad companies’ have limited assets. • One version of national healthcare provided $10 billion in subsidies towards funding of the UAW retirees’ healthcare obligations (uncertain as to whether it made in in the final version of the bill). Senate movement to secure $3 billion for Delphi retirees’ healthcare. • 54 of the top 150 auto suppliers have filed for bankruptcy. Job loss unknown, but still in flux.

Auto Industry – Other Barriers (Cont.) • Market Capitalization: • Wall Street deals can be larger than combined market capitalization of the above five companies. Microsoft offer to buy Yahoo was for $47.5 billion; Yahoo rejected. Anheiser Busch’s deal was roughly $50 billion – almost 5 times the five companies’ market value. • Toyota – market capitalization August 4, 2010 - $116 billion (even with the recent quality problems). Cash position on March 31, 2010 - $43 billion with favorable working capita of $26 billion. Operating profit for quarter ended June 30, 2010 - $2.2 billion. Recalls may have had a dent in operations, but nothing long term. • Toyota’s financial strength and early launch of ‘green’ cars will provide a significant advantage over the Detroit 3 in meeting the new mileage standards imposed by the federal government for 2016.

Michigan Fiscal and Budget Issues • Summary of Michigan’s critical fiscal issues: • General and School Aid Funds have very weak balance sheets and getting weaker. These Funds represent half of State operations. • Deficits (liabilities > assets, insolvent) in several State funds. • Unemployment borrowing from federal government (prior discussions). • Weak / inaccurate budget projections. Single year budgets. • No fiscal plans (short or long-term) to solve local governments’ budgets. • Continued program mandates on local governments in conflict with Constitution. • State accounting system fails to identify adverse operating trends on a timely basis. 2009 CAFR was delinquent. • Management cannot agree on fiscal policy direction with the result being delayed discussions in resolving significant future operating losses. • Pension and retirees’ healthcare issues. • Above ‘hidden’ through federal stimulus funds - $4.5 billion for FY-2009 to FY-2011 serving to avoid revenue increases and / or expenditure reductions. Left for next governor to sort out.

Michigan Fiscal and Budget Issues (Cont.) Notable balance sheet fiscal problems – prior schedules: • General Fund cash at September 30, 2009 - $7.5 MILLION; accounts payable of $1.93 BILLION to be paid from the $7.1 million in cash – how do you pay $1.93 BILLION in accounts payable with $7.5 MILLION in cash? • School Aid Fund (SAF) ‘borrowing’ of other State funds’ cash of $1.3 billion to $1.5 billion from other State funds over the past half dozen years. • General Fund receivable from SAF = $575.0 million. SAF has $1.3B to $1.5B cash deficit (would be an overdraft if in a separate bank account) and the General Fund providing operating subsidies to the SAF – how does the SAF ever repay General Fund? Is the $575.0 million receivable collectible from the SAF? General Fund receivable from the SAF of $575.0 million is 59% of General Fund equity and it is growing! • SAF amount owed to other funds of $722.5M in 2009 is almost all owed to the Transportation Funds – road construction and maintenance and transit, largely owed to the local units of government. What business does the SAF have with road construction / transit subsidies? • Even as General and SAF equities are questionable, a $208 million transfer from the SAF has been approved for transfer to the General Fund in fiscal 2010.

Michigan Fiscal and Budget Issues (Cont.) • Despite the State having a ‘balanced budget’ on paper, the State’s actual performance failed to balance the budget in 7 (red) of the past 9 fiscal years (e.g., they used equity to balance operations) – see next slide. • Too many ‘one-time’ budget gimmicks have been used, including: use of equity; sale of tobacco future revenues for $415M through 2054 (to pay for 2007 operations and similar securitizations will cost the State $2.8 billion); delaying payments to next accounting period; county ‘shift and shaft’ in 2005; and so many others nearly impossible to list. • Judge Giddings just placed an injunction on the State’s receipt of the 3% from teachers in the recent retirement incentive program that resulted in 17,000 retirements June 30, 2010. Potential exists that State will have to fund additional costs, with no employee paid offset against those costs. • Citizens Research Council has a study on ‘one-time’ budget gimmicks. Also has report on State’s cash flow problems – on CRC’s web site.

Michigan – “Tax Expenditures” / Revenues • Reductions of revenues otherwise collected rather than an expenditure that has been appropriated. Tax expenditures are largely ‘hidden’ from public discussion but are far from insignificant. Often provided to companies to entice them to locate in State. • Tax expenditures by year – projected by House Fiscal Agency (will be problem in balancing future budgets): • 2009 - $ 138.8M. • 2010 - $ 557.4M (Increase – Earned Inc. Tax Credit; Film Credits). • 2011 - $ 624.1M. • 2012 - $ 840.6M (MBT rate decline; battery credits). • 2013 - $1,262.7M (MBT rate decline; battery credits). • 2014 - $1,493.3M (MBT rate decline). • Battery credits in above - $40M in 2012; $268M in 2013; and $276M in 2014. • Personal income tax – recently 72% of the population submitted income tax returns with $100 or less income taxes paid.

Michigan Pensions / OPEB • Pensions: • FY-2002 to FY-2009, State shorted State and school pension payments from the actuaries’ pension recommendation - will be funded by future generations. • State and school pension plans were shorted $544 million and $853 million, respectively – total of $1.4 billion shorted in pension contributions from FY-2002 to 2009 (if paid, both the General and School Aid Funds would have had deficits at September 30, 2009). • Failure to fund pension by local governments is a trigger that could cause an appointment of emergency financial manager act – Act 72. • The September 30, 2008 school and state pension reports an unfunded actuarial accrued liability of $11.6 billion as reported in 2009 CAFR and School actuarial reports.

Michigan Pensions / OPEB • Pensions (continued): • In 2008 and 2009 the investment market declined. It takes several years before the value declines are reflected in pension contributions. The declines may increase State and school district pension contributions as early as 2011 and beyond – particularly if the market does not recover to the prior levels. • Governor’s budget recommendation freezes schools’ base foundation allowances, but increases their pension / OPEB burden by $243 million out of already reduced revenue base ($162 per pupil net reduction in State support to schools). Fringe benefit rate increased from 16.94% to 19.41%. Even with the increase, the State is still not covering the full pension / OPEB costs – leaving the costs to future generations. Passed school appropriations with only an $11 per pupil increase.

Oakland County’s Timeline of Retiree Healthcare Changes and Annual Cost of ARC Planned full funding of UAL with COPS Plan closed to new hires Cost differentiation by age Prescription co-pay increased VEBA Trust Created Vesting schedule lengthened Actuarial ARC payment begins Vesting schedule lengthened Increase to 100% of premium Benefit Begins, 50% of Premium

State Budget Problems – Pensions / OPEB (Cont.) • Retirees’ healthcare (OPEB): • $41.5 billion in unfunded liabilities (State plans - $15.5B; Schools - $26.0B) at September 30, 2008 and growing at a pace of roughly $2 billion annually as State is only funding medical bills when presented (e.g. “pay-as-you-go”). Likely $45B to $50B today. Amounts will be paid by future generations. • State does not pre-fund retirees’ healthcare – if they did, they would have to find another $1.7 billion to $2.0 billion in new revenues (or reduced expenditures)annually for each of the next 30 years from existing revenues . General Fund revenues may be $7B / School Aid - $12B – even as they struggle to resolve the operating shortfall for 2011. • Retirees’ healthcare left for new governor to resolve.

REAL ESTATE - GENERAL • The information contained herein is aggregate information on a county-wide basis. It does not represent the increases / decreases in assessed or taxable values by either community or by individual parcels of property. • Residential values are based on sales as compared to the values maintained in local assessing records. Sales price > assessed value = assessed values go up; Sales price < assessed value = assessed values go down. • Sales prices are determined during Oct. 1 to Sept. 30 period, for the Dec. 31 assessment roll 90 days thereafter. Taxable value at Dec. 31 is used for the following year’s tax levy (govt. revenue) with collections following. • Substantial time lag between residential sale and impact on taxable value – meaning even as the market prices may eventually trail back up, the actual impact on governmental revenues could lag up to two years thereafter.

Oakland County, MI Sheriff Deeds - Foreclosures Number of Foreclosures * 1 in 377 1 in 253 1 in 62 Ratio: 1 in 532 1 in 225 1 in 212 1 in 174 1 in 97 1 in 51 1 in 56 1 in 47 Sheriff Deed totals retrieved from the Oakland County Register of Deeds office. * 2010 Count is estimated using the first 5 months of actual sheriff deeds.

Oakland County, MI Percentage Change in Assessed and Taxable Values * * * * 2011 - 2013 Taxable and Assessed Percentages Estimated by the Oakland County Budget Task Force. 2001 - 2010 information from annual Equalization Reports

Real Estate Issues – State Impacts • Impact on the State budget could be hundreds of millions for: • State Education Tax (SET – 6.0 mils) – the taxable value declines projected by Oakland County, which will mirror other counties, will directly impact the SET for schools. State gets approximately $1.8 billion in revenues for the SAF. Senate Fiscal Agency predicts 3.4% growth in SET (e.g. taxable value). • Schools’ Base Foundation Allowance – declining local school property taxes will increase the State’s subsidy to cover the losses (or, reduce the base foundation allowance). Formula uses data of a year ago for school property taxes – meaning the impact of property value declines will be delayed one year. Student census declines may somewhat mitigate this matter. • State transfer tax revenue – fee based on values; given fewer properties being sold has declined significantly in the recent year. • Oakland Schools (ISD) impacted in three millages (General, Special and Vocation Education millages of 3.3690 mils in total) as it is fixed against declining taxable value. Special Education operation largest and hardest hit, negatively impacting payments to local school districts..

Real Estate Issues – Regional • Oakland County taxable value declines (e.g. county-wide) used in budgeting process at Dec. 31 assessment dates (for following period’s levy): • 2007 - .04% increase before MTT losses. • 2008 – 3.6% decrease before MTT losses. • 2009 – 12.25% (actual), including MTT loss provision of .5%. • 2010 – 12.0% in budget. No change from prior estimates in May 2010 before 2011 to 2013 budget submission to Board of Commissioners. Next review in detail is late October 2010. • 2011 – 5.0%. The 2011 declines are likely to increase depending how the currently unemployed impact property values – will take at least two years to work through the system. • 2012 – 2.5% (see above concerns). • Total – Dec. 31, 2007 to Dec. 31, 2012 = 35.31% decline in taxable value on the principal government revenue source.

Future Regional Real Estate Issues • Property tax declines of Oakland County mirror other counties: • Macomb County – projecting 13% and 10% declines for Dec. 31, 2010 and 2011 assessment rolls. • Wayne County – projecting 6% and 3% declines for Dec. 31, 2010 and 2011 assessment rolls. Wayne County is auctioning off 13,000 properties, including 5,300 still occupied by owners / renters. • Delinquent Tax Revolving Fund (DTRF) Chargebacks – delinquent taxes ‘sold’ by local units to county treasurers. If not collected owner, investor or paid by bank (foreclosure), then after several years the local units must repay the amounts advanced as the treasurer’s charge back the uncollected receivables to the local units. Has been minor in the past, but in some areas it is becoming critical.

Future Regional Real Estate Issues • Detroit charge backs from Wayne DTRF– 2008 CAFR disclosed a $57.6 million lost arising from the charge backs from Wayne County Treasurer on uncollected delinquent taxes several years earlier. Annual levy is only $220 million. The chargeback loss had grown to $68.6 million of the levy for fiscal 2009. Likely, 2010’s loss is even higher. • Question – banks failed to make their payments on the delinquent property taxes as the property was not worth the outstanding tax amount resulting in the City taking title to blighted properties. Why would banks invest in future residential sales in Detroit when incurring present losses? • School Districts - school districts stressed because of fiscal structure / relationship between the State and schools (pension / retirees’ healthcare issues), Proposal A, etc.. Funding structure very troubling, particularly with reductions in base foundation allowance and 20j veto by Governor.

Future Regional Real Estate Issues • State Lending Support: • Distressed governments (particularly schools) now have to borrow using their credit rating (municipal insurers all but gone). By summer 2011 (absent new revenues or substantial reductions in costs), half the school districts could be in deficit – “deficits” would mean that they would not have sufficient cash to operate, absent borrowing. • Schools, cities and counties have weakest cash flow at same time – March to June. Will be competing for cash resources from the credit market – which is still troubled. • If entities cannot secure direct short-term loans from banks, they will seek loans from the State. The State would then be required to bundle loans and sell combined loans, advancing the proceeds to local governments (State has authorities to do so) – State would intercept State support if local governments couldn’t pay debt service. • Given that half the school districts may be in deficit next year, for example, will the banks still loan funds to the State and local governments when the operating shortfalls are structural – meaning the successful operations of the schools is almost entirely dependent upon the base foundation allowance provided by the State?

Future Real Estate Issues (Cont.) • Future taxable values will not return to levels (absent millage increases) to Dec. 31, 2007 levels until circa 2020 – 2025. Construction will be minimal until at least mid-2015 or so. Pop-ups (increases from taxable value to SEV when property sold) won’t occur for the decade as most residential property is at SEV = TV now. (Limited to economic increases only – 35.3% decline / say 3% or 11.7 years with the start of recovery circa 2012-ish). • Governments will have to do without increases in property tax revenues for a half-generation – while expenditures have no limitations on economic increases. • Above assertions affirmed in Pew Report (Sept. 2009), Land Institute Report prepared by PriceWaterhouseCoopers (Oct. 2009) and Blue Canyon Partners Report (Aug. 2009).

Regional Fiscal Issues Impacting State • Debt issues - declining taxable value could jeopardize the fiscal solvency of TIFAs / DDAs / LDFAs which have issued debt in anticipation of taxable value increases. • Schools’ debt - use unlimited general obligation debt (voted by electorate). Declines in taxable value mean millage rates for school debt issues may increase to cover fixed debt service costs otherwise paid by a local school district General Fund. If mils are raised, public will be surprised July 1, 2010 in levy notices. • Millage increases - taxable value declines “solved” through millage increases will lead to voter tax fatigue. Schools cannot levy operating millages. • Banks halt foreclosures – will lead to next bubble. In short-term, prices will rise as inventory is cleared, but when the backed-up foreclosures are released, prices will drop precipitously. Will delay return to normalcy.

Regional Issues - State Finances (Cont.) • Detroit Public Schools: • June 30, 2009 CAFR reflects a General Fund unreserved deficit of $222.2 million and an entity-wide deficit of $537 million (liabilities in excess of assets). • General Fund operating loss for 2009 was $79.2 million – meaning the budget is yet to be balanced, let alone addressing the deficit accumulated through June 30, 2009. • In August 2009, the short-term note payable, in part, was refinanced with long-term debt bearing a tax-exempt interest rate of 9.5%. State has promised to intercept base foundation and other support in the event that DPS fails to make the debt service payment. • The net value remaining of facilities after depreciation and outstanding debt is just $38.3 million as of June 30, 2009. • Estimated deficit at June 30, 2010 (before audit / liabilities over assets) is $363 million – with the fiscal 2011 operating budget expected to increase that amount as well.

Regional Fiscal Issues Impacting State (Cont.) • City of Detroit: • As of June 30, 2009, the unreserved General Fund deficit is $331.9 million, with the entity-wide deficit (accrual-based presentation) of $956.9 million. • General Fund had an operating loss of $124 million in fiscal 2009. • In March 2010, the City issued $250 million in bonds that would provide cash and eliminate a portion of the deficit, but does not address the structural imbalance of the revenues and expenditures in the General Fund. Short-term ‘solution’ only to buy time for restructuring services. • With the City’s legal debt margin of $568 million at June 30, 2009 and issuance of $250M in debt in 2010, future issuances of long-term debt to solve the City’s fiscal issues is unlikely. • $4.8 billion in unfunded liabilities relating to retirees’ healthcare obligations – not funding the plan (only paying medical bills as presented).

Regional Fiscal Issues Impacting State (Cont.) • Detroit (continued) – real estate values / issues: • Median residential property value - $97,847 in 2000. Now, $12,439. • 102K vacant properties (CRC report); total residences – 365K. • 2009 net property tax revenues - $168 million; $80 million returned delinquent to Wayne County Treasurer (e.g. not paid by owners / banks). • 17K properties taken over by Detroit arising from unpaid taxes in 2009 alone – Mayor’s proposal in 2010 to tear down 3K properties will resolve the new 2009 properties by 2016.

Regional Fiscal Issues Impacting State (Cont.) • Wayne County - Equities as of Sept. 30, 2009: • General Fund - $68.9 million deficit. • Juvenile Justice …Fund - $20.6 million deficit. • Circuit Court Fund – $68.8 million. • Total $158.6 million in unresolved deficits. • Presently, lawsuit and disputes exist in bringing operations into line with expenditures – Circuit Court lawsuit (courts always win lawsuits); other county-wide elected officials. • Wayne County is attempting to resolve a $100 million operating shortfall for 2010 – which would increase the above deficits if it occurs. The County has announced a cumulative deficit (i.e. liabilities > assets) of $266 million anticipated for September 30, 2010.

Regional Issues Impacting State Finances (Cont.) • Pontiac – in Act 72 with emergency financial manager. Police department reduced from 170 FTEs to 65 FTEs. Pontiac school district struggling as well and just avoided payless paydays by days through a TAN. • Macomb County – recently ‘solved’ their 2009 operating shortfall with a tax increase to its authorized limit. Have recently announced additional fiscal issues. • SMART (bus services) has an unresolved 2012 operating shortfall of $9.6M and increasing thereafter – even after the passage of the operating millage on August 3, 2010. • Ecorse just went into Act 72 – emergency financial manager. Other local units of government struggling.

Summary • The solutions to resolve the budget beast facing State and local governmental units are many. There is no shortage of solutions – new taxes, service reductions and / or structural reforms – it seems a shortage of political will to undertake tough decisions before the crisis occurs. • Unfortunately, there will be numerous governmental units who will be unable to plan longer-term for the fiscal crisis ahead and likely will find themselves facing Act 72 – an emergency financial manager or worse. • Proper management principles, long-term planning, leadership and political will can solve the tough business issues facing Michigan governments.