Download

1 / 8

90 likes | 273 Views

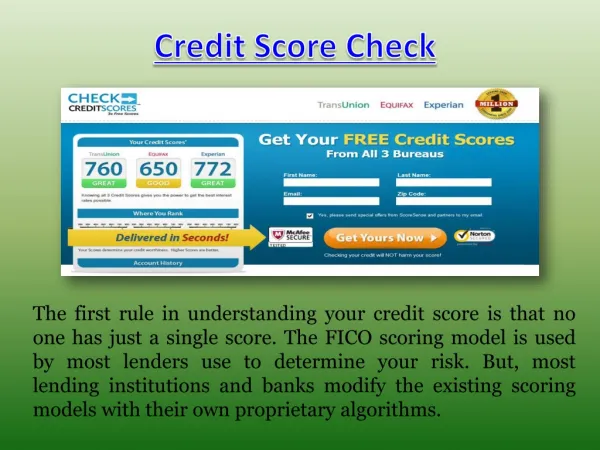

If a lender is checking your credit score, chances are they are checking it with FICO. Named Fair, Isaac, and Company in 1956, the company was later rebranded as the Fair Isaac Company in 2003 and finally “FICO” in 2009. Selling over 10 billion credit reports annual since 2013, FICO’s 3-score system displays credit score statistics from Equifax, TransUnion, and Experian. <br>

E N D

If a lender is checking your credit score, chances are they are checking it with FICO. Named Fair, Isaac, and Company in 1956, the company was later rebranded as the Fair Isaac Company in 2003 and finally “FICO” in 2009. Selling over 10 billion credit reports annual since 2013, FICO’s 3-score system displays credit score statistics from Equifax, TransUnion, and Experian. With products geared to the automotive and mortgage industries as well as retail, banking, and financial consultation services, FICO is the “big fish” when it comes to today’s credit reporting.

Quick Facts: Company: FICO Founded: 1956 Services: Consumer Credit Scores, Commercial Credit Solutions Countries: Worldwide Price Range: $19.95

What goes into a FICO credit report? FICO credit scores range from 300 to 850 points, and you are analyzed based on your payment history, the amount of debt you have, your length of credit history, and if your credit is new or not. According to the FICO metrics, to get a good credit score you should have: a long credit history, no serious delinquency, and recent credit card use. Factors that could potentially damage your credit score include: high credit usage, recent collection items, or bad payment history. Today, over 90% of US lenders use the FICO system to qualify you.

How often should you get your FICO score? In general, it is a good idea to keep a close eye on your credit which means ordering and reviewing your score annually – or, more frequently if are planning on improving credit. Keep in mind that each time you apply for new credit, another credit inquiry is added to your report. Each credit inquiry you add can potentially affect your ability to apply for products or services in the future, so keeping tabs makes sense. Another good reason to check your credit score often is that if you see a credit inquiry you didn’t apply for, or an open trade you didn’t ask for, your identity might have been compromised.

For those that do find unwanted or excessive inquiries, contact Inquiry Busters to have them removed for less.