Download

1 / 16

160 likes | 344 Views

Your Credit Score. You need to know the facts about credit scores in order to use them to achieve your financial goals. This workshop reviews the types of scoring models being used today and give you the game plan for using them to your advantage. What is a Credit Score?.

E N D

Your Credit Score You need to know the facts about credit scores in order to use them to achieve your financial goals. This workshop reviews the types of scoring models being used today and give you the game plan for using them to your advantage.

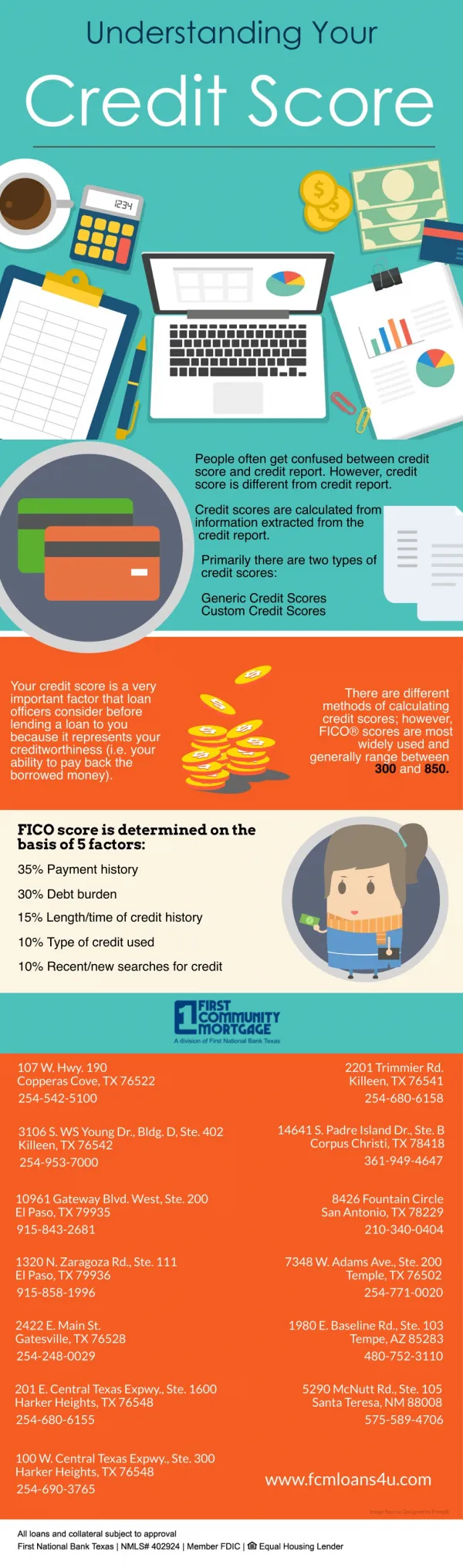

What is a Credit Score? • Numerical measure of credit worthiness • Based on information in credit report • Credit report tracks credit activity • Compiled by three bureaus: Equifax, Experian, TransUnion • Many creditors just look at score, not report

FICO Score • Most widely used scoring model • 300–850 • The higher, the better • Score from each bureau • Creditor may check all three or only one

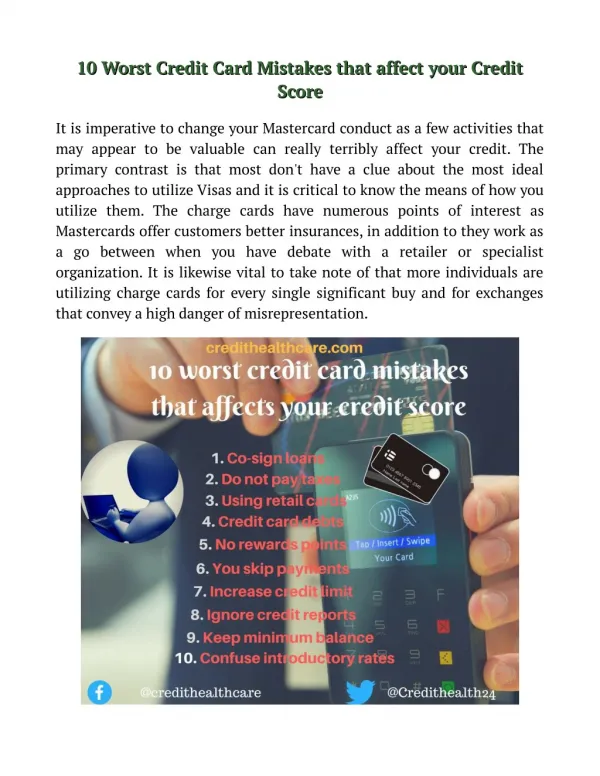

FICO Score Components • Payment history: 35% • On-time payments help, late payments hurt • Collection accounts and legal actions especially harmful • Amounts Owed: 30% • Hurts to have balance close to credit limit

FICO Score Components (continued) • Length of credit history: 15% • Longer history improves score • New credit: 10% • Number of new accounts • Inquiries • Types of credit used: 10% • Variety good

Having a Low Score Can Cost You • Score determines approval and interest rate • For loans, higher interest rate = higher monthly payment and higher total cost

How to Improve Your FICO Score • Keep your old accounts • Limit balance transfers • Avoid excess credit applications • Be patient • Always pay on time • Pay down existing debt • Diversify your credit • Check your reports for errors

Beware Credit Repair • Companies claim to repair credit for high fee • At best, charging you for something you can do for free • At worst, using dishonest or illegal tactics • Flooding credit bureaus with disputes • Issuing new identity

Rapid Rescoring • Offered by some mortgage lenders and brokers • Gets errors corrected or information updated quickly • Not used to disputed accurate negative information

VantageScore • Score (300 – 850) and grade • Able to rate newer credit • May ignore paid collections

Other Scores • Bankruptcy risk scores • Risk will file for bankruptcy • Internal scores • Created by creditors • Non-traditional scores • Look at non-credit information • May be better to establish traditional score

Obtaining Your Score • Can get score for free if adverse action taken against you • Must pay in most circumstances • See handout for contact information • Pay attention to what score you are purchasing

When to Ignore Your Score • Your score is already excellent • You will not be using it • You have more important financial issues to deal with