Download

1 / 14

180 likes | 584 Views

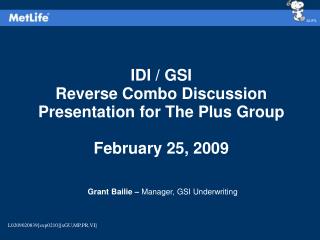

IDI / GSI Reverse Combo Discussion Presentation for The Plus Group February 25, 2009. Grant Bailie – Manager, GSI Underwriting. L0209020839[exp0210][xGU,MP,PR,VI]. Group LTD vs. Individual DI. Group LTD coverage may not be enough!. Definition of Disability

E N D

IDI / GSI Reverse Combo DiscussionPresentation for The Plus GroupFebruary 25, 2009 Grant Bailie – Manager, GSI Underwriting L0209020839[exp0210][xGU,MP,PR,VI]

Group LTD vs. Individual DI • Group LTD coverage may not be enough! • Definition of Disability • Many group LTD plans have a 1 or 2 year “own occupation” definition of disability, which then changes to “any occupation” • IDI offers “own occupation” coverage to age 65 in most cases • Premiums • Premiums for LTD plans are constantly changing, depending on the experience of the group, or even the experience of the carrier • IDI plans offer non-cancelable and/or guaranteed renewable rates • Portability • Many group LTD plans are not portable, meaning that coverage is tied to employment. If the insured leaves his/her employer, they often lose the group LTD coverage • IDI policies are individually-owned and portable

What is GSI (Guaranteed Standard Issue)? Guaranteed Standard Issue means that MetLife will issue an IDI policy with limited medical underwriting and no pre-existing condition limitation as long as you have been actively at work for the past 90 days and are actively at work on the effective date of the policy.* * GSI offers are contingent upon underwriting review of the case and are not available to all groups.

Plan Designs • Supplemental Buy-Up Plans • Reverse Combination Plan

Supplemental Buy-Up Plans Salary 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% To t a l Co m p e n s a t i o n 75% of Total Compensation minus LTD to $XX,000 Monthly Maximum 60% of Salary Income to $XX,000 Monthly Maximum 180 Days Age 65 Wage Continuation or STD Group LTD Individual DI Uninsured Income

Reverse Combination Plan Commonly known as “reverse combo”, this plan “reverses” the LTD and IDI coverage, so that the LTD coverage actually supplements the IDI plan.

Reverse Combination Plan Description • Base IDI with layer of group LTD on top to provide coverage for income not covered by the IDI base plan. • IDI plan must have 100% participation. • Both the IDI and group LTD should have the same definition of earnings. • The following formula is used for the group LTD: 0% of the first $xxx,xxx of covered earnings 60% of the next $yyy,yyy of covered earnings • Need to verify with group underwriting to be sure this type of plan is available

Reverse Combination Plan $300,000 $200,000 $100,000 I N C O M E Group LTD: 0% of first $100,000 of income 60% of the next $100,000 to a Maximum Monthly Benefit of an additional $5,000 30% of Salary Income Replacement to $XX,000 Monthly Maximum Individual Coverage 60% of Income Up to $100,000 $5,000 Monthly Maximum Age 65 180 Days Wage Continuation or STD Corporate Purchased IDI Group LTD Uninsured Income

Case Study – LTD Rates • 1999 LTD Rate = $0.4235/$100 covered payroll • 2000 LTD Rate = $0.4235/$100 covered payroll • 2001 LTD Rate = $0.4769/$100 covered payroll • 2002 – 2005 LTD Rate = $0.6490/$100 covered payroll

Plan Design Change – Reverse Combo • In 2005, the final plan design was developed to move the first $200k for highly compensated associates from the LTD plan to the IDI plan and new rates were developed • 2006 • LTD Rate = $0.581/$100 covered payroll – for those employees not eligible for the IDI plan • LTD Rate = $0.270/$100 covered payroll – for those employees eligible for the IDI plan for income amounts in excess of $200k

Overall Effect • LTD rate for execs in the reverse combo plan were lowered by over 58% • IDI premiums are non-cancelable, so rates are locked in at issue age • Over time, the entire plan may break even or actually be less expensive if LTD rate holds and younger group of IDI participants come on board • Combined plan design encourages persistency of both LTD and IDI

How to get started For more information contact your local Plus Group office To find a Plus Group office near you: Go to www.plusgroupus.com and click on the agency locator map or call (800)831-1018