Download

1 / 53

700 likes | 985 Views

Organizational structure and business transactions in SAP R/3. Structure of the SAP R/3 System in commercial terms. Accounting Area Financial Accounting (FI) Controlling (CO) Asset Accounting (FI AA) Human Resources HR Logistics Production Planning (PP) Materials Management (MM)

E N D

Organizational structure and business transactions in SAP R/3

Accounting Area • Financial Accounting (FI) • Controlling (CO) • Asset Accounting (FI AA) • Human Resources • HR • Logistics • Production Planning (PP) • Materials Management (MM) • Sales and Distribution (SD) • Quality Management (QM) • Service Management (SM) • Plant Maintenance (PM)

Organizational units in the Financial accounting module • Client • Company Code • Business Area • Company • Credit Control Area • Funds Management Area • Dunning Area • Chart of Accounts • Controlling Area

Client • Central organizational element • Top-level structural element of a company • Separate unit with its own separate master records and complete group of tables • To spesify the client in which the user want to work they have to enter a Client Code when they logs into the R/3 system

Company Code • Client can be subdividet into one or more Company Codes • Represent legally independent companies • Several Company Codes in each client allows you to manage accounting data for different independent companies at the same time

Business Area • One company code can be divided into several business areas • One business area may also be used in multiple company codes • Only used to provide in-house information in the SAP R/3 system

Company • The smallest organizational unit for which legal financial statements can be prepared • Can include one or more company codes • Each one of a company’s company codes must use the same Chart of Accounts

Credit Control Area • Organinzational unit in which all account receivable from a customer are totaled • Can be defined in such a way that it can be used in several Company Codes

Funds Management (FM) Area • Used to plan the deployments of Funds • Identical to the Company Code in broad terms • Controls budget management in an independent unit that draws up its own accounts • You can assign several Company Codes to one FM Area

Dunning Area • Dunning procedures are usually managed in the accounts receivable and accounts payable departments • If dunning is managed independently in several organizational units you must create Dunning Areas

Chart of Accounts • Contains all of a company’s General Ledger accounts • Used by both the Financial Accounting and the Controlling modules • 1-1 relationship between Chart of Accounts and Company Code or Controlling Area

Single-code system: • internal and external accounting form one unit • all the postings are accountable • you can only calculate a company’s net income after determining the neutral expenditure and the neutrale income • Dual-code system: • financial accounting and operating accounting are carried out in two separate settelment areas • each settelment is a closed unit • The information in a Chart of account controls how master records are created in the Company Code

Controlling Area • Organizational unit in the Controlling module • The information in Financial Accounting is directed towards interested parties from outside the company. • Controlling does not have to comply with the legal regulations for financial accounting.

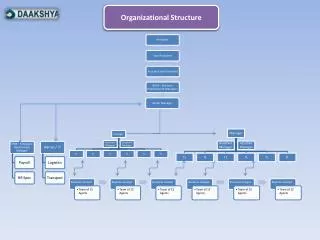

Organizational units in the Logistics modules • The Plant and Sales Organizations organizational elements within the Logistics modules are assigned to spesific Company Codes

Overview of the organizatinal structures of Logistics elements

Plant and Storage Locations • Company’s productions locations and branch offices are represented by Plants • One Company code may contain several Plants • The plant is the location at which goods are manufactured or a service is performed • A plant may consist of several physical Storage Locations

Sales Organization Distribution Channel and Line • Sales organization is the top organizational unit in the Sales and Distribution module • You can assign one or more Distribution Channels to the same Sales Organization • You can assign several Lines to the same Distribution channel • Lines represent various product groups

Organizational structure for Sales Organization, Distribution Channel and Line

The structure of the Financial Accounting module • The task of financial accounting department • is to record all business transactions systematically and comprehensively • enter all these transactions in the system, and document them

Financial Accounting is subdivided into • General Ledger • Extended ledger • Accounts payable • Accounts receivable • Asset accounting • Consolidation • Financial contolling • Investment • Funds monitoring • Travel management

Connecting to other SAP modules • The Financial accounting module is linked to almost all the others in SAP • Business transactions are recorded as they occur in the form of documents, and stored in a shared database

The document principle • All postings are always stored in the form of documents • Each document must be complete before it is posted • Each document must contain specific minimum information (document date, document type, posting key, account numbers, amounts) • Incomplete or inconsistent Documents cannot be posted

Real-Time posting • Ensures that all employees at different levels have continous access to a current and uniform dataset • SAP R/3 supports Real-Time processing by using a combination of batch processing and dialogue processing

Double-Entry Accounting • Ensures that all the business transactions recorded in subledgers are also posted to the relevant reconsiliation account in General Ledger accounting • You can post data in the Controlling application component at the same time

General Ledger Accounting • Provide a comprehensive picture of the external accounting process and the accounts involved in it • Provides the following functions: • Atomatic and simultanious posting of all subledger item to the coresponding ledger accounts • Simultaneous updating of the general ledger and controllig data • real-time evaluation and reporting of current posting data in the form of account displays and closing accounts with different financial statement versions

General ledger accounts • Contain the increases and decreases that correspond to the flows of goods and services used in the Logistics module • contains master records that controls how business transactions are recorded and posted to the account • The Master data record identifies whether an account is a reconsiliation account • Reconsiliation accounts groups together the value items from the accounts of individual subledgers

Documents in Financial Accounting • Document type is an importent control elememt in the SAP R/3 system • Document type is used to: • identify different business transactions • control how account types are posted • assign document numbers • determine whether a ’gross’ or ’posting’ is involved • Posting key controls how documents are recorded

Financial statements • Divided by time into daily, monthly and annualfinancial statements • Daily financial statements: • can be created immediately without any extra steps • is sorted chronologically in a posting journal • Monthly financial statements: • carry out a number of closing tasks to create it • Annual statments: • The annual accounts is designed to provide information for internal and external recipients • Business transactions need to be entered in chronological order

Structure of the Balance Sheet and the P&L account: • In SAP R/3 system you can create Balance Sheet and P&L statements in various language and currencies to meet the requirements of companies that operates internationally • you can select different classification schemes for communications, tax and international reports

Subledgers • Contain posting data information in detail • The following subledgers are part of the R/3 system’s ledger: • Account Receivable • Account Payable • Asset Accounting • Inventory Accounting • Personell Accounting • Bank Accounting

Account Receivable • Contains the accounting data for all the accounts receivable that are present in the system • Customer master data record: • contains all the data that describes the commercial relationship with a specific customer • used by the Financial accounting component • divided into a general section, a section for individual campany codes and a section for sales data

Outgoing invoices and credit memos: • the system will automatically post invoice and credit memos in the FI module when you create an invoice or credit memo in SD • Prcessing incoming payments: • by computerized direct debiting or manually, by check or bank order • Dunning letters: • to include a customer in the SAP R/3 system’s automatic dunning process, you must first enter a predefined dunning procedure in the customer master data record

Customizing background for defining the dunning program: • Which company codes must always be included in dunning • Which dunning procedure is to be used • Which dunning costs are to be charged • The net data on which a specific dunning stage is reached • Which dunning letter is to be sent to the customer

Account Payable • Manages all vendor accounting data • Vendor Master data record: • is created in the same way as the customer master data record • contains all the data required for handeling the business relationship • Incoming invoices: • For MM and FI modules you enter this data in the module’s Invoice Check Procedure function • The Invoice Check Procedure checks the data of an incoming invoice against the data of tha order and delivery

Payments: • SAP R/3 system can use the payment program to handle cash transactions automatically • Two-stage process • The system uses the information in the documents and master record to create a payment proposal list • Customizing backgrund for defining the payment program: • Which company codes always take part in cash transactions and which company codes are to handle payments • Which methods of payments are to be used in each case • From which bank account the payment is to be made • The form to be used for payment

Assets Accounts • administers and monitors a company’s fixed assets • The following functions are integrated in it: • Asset accounting and valuation • Leasing management • Consolidation preparation • information system • Linked to a great many other modules of the SAP R/3 system

Bills of exchange • a contractual security whereby the person issuing the bill places himself/herself or a therd party under an obligatin to pay a certain sum within a certain period • Payee: recipient of the payer • Drawee: person paying • Anyone who signs a bill of exchange is liable for the sum • A bill of exchange merely documents the legal aspects of payment claims

Bill of exchange strictness • A bill oexchange can be written on any sheet of paper, but only counts as a bill of exchange if it meets the legal requirements: • Must appear in the text of the document • in the language in which it is issued • it must consist of som other components (certain sum of money, name of drawee, expiery data, place of payment, to whom the payment is to made, day and place of issue, signature of the issuer) • The following variation can apply: • The issuer can also be the drawee • The issuer can also be the payee • The issuer places itself under obligation