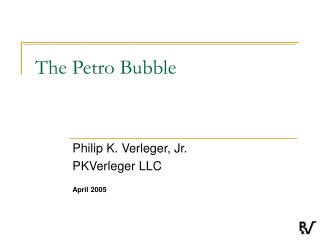

The Petro Bubble: Analyzing the Surge in Crude Oil Prices (1998-2005)

This paper explores the dynamics behind the significant rise in crude oil prices between January 1998 and April 2005. It highlights how pension funds increasingly view commodities as a reliable investment class, contributing to skyrocketing prices. The analysis presents a contrarian view against the prevailing narratives, arguing that the price surge is not driven by fundamentals but by speculative investments. It discusses the interplay of global factors, including wealth accumulation, supply adequacy, and the roles of key players like OPEC and Saudi Arabia in influencing market perceptions.

The Petro Bubble: Analyzing the Surge in Crude Oil Prices (1998-2005)

E N D

Presentation Transcript

The Petro Bubble Philip K. Verleger, Jr. PKVerleger LLC April 2005

Crude Oil Spot Prices, January 1998 to April 2005 Source: Platts.

Theme • After ten years, commodities have finally become a suitable investment class for pension funds. • The billions pushed into funds have contributed to the 12-month rise in crude prices. • OPEC’s focus on market backwardation kept returns good. • Money continues to chase oil assets even as prices rise to unheard of levels. • The rise may culminate in a “Super Spike.” • Or Saudi Arabia may deflate the bubble.

This price rise is not about fundamentals. • The press and analysts attribute the price rise to supply and demand factors. • Extraordinary growth in China and India • Lagging investment in E&P • Inadequate and unsuitable refining capacity • Others attribute the price rise to a belief that global reserves have been exhausted.

These explanations do not fit the facts. • There is plenty of oil today. Tanks are full. • The world is awash in cash and investors seek outlets. Commodities are a new outlet. • High prices today are the best cure in the long run for expectations of high prices. • Ultimately, Saudi Arabia and/or the United States have the power to cure the current level of high prices.

Current oil supplies are more than adequate. • US crude stocks are well above normal levels. • Global oil stocks have increased. • Returns to storage – the market indicator of supply availability – are at record levels, suggesting a growing surplus. • Discounts of cash to futures confirm the surplus.

U.S. Commercial Crude Oil Inventories, 1982 to 2005 Normal Range Source: API.

Usable Commercial Stocks in OECD Countries Normal Range Source: EIG; PKVerleger LLC.

WTI Returns to Storage, 2004, 2005, and Normal Range Normal Range 2005 2004 Source: PKVerleger LLC.

Brent Returns to Storage, 2004, 2005, and Normal Range Normal Range 2005 2004 Source: PKVerleger LLC.

Natural Gas Returns to Storage, 2004, 2005, andNormal Range 2004 2005 Normal Range Source: PKVerleger LLC.

Heating Oil Returns to Storage, 2004, 2005, andNormal Range 2004 2005 Normal Range Source: PKVerleger LLC.

Gasoline Returns to Storage, 2004, 2005, and Normal Range 2005 2004 Normal Range Source: PKVerleger LLC.

March 2005 Crude Oil Price – Settlement Price of First Futures vs. Spot Crude at Cushing Source: NYMEX; Platts.

Commodities as an Asset Class - 1 • Investment banks have pushed commodities as an investment class for 14 years. • Academic research shows returns on collateralized commodities match or exceed equities and bonds while being negatively correlated with these assets. • Research was ignored until recently. • No more than $5 billion invested until end of 2003 • Now probably more than $75 billion invested

Commodities as an Asset Class - 2 • Research was ignored until recently. • No more than $5 billion invested until end of 2003 • More than $75 billion invested by end of 2004 • At least $40 billion more invested in oil in the first quarter • Research shows investment in commodities boosts portfolio returns. • Returns from investment in energy easily overwhelmed returns on other assets in the first quarter.

New Research by Gorton and Rouwenhorst • Returns to futures exceed returns to spot commodities. • Commodity investments “outpace” inflation. • Return on futures matches S&P 500. • Commodity returns are negatively correlated with equities and long-term bonds. • Commodity futures have opposite exposure to inflation compared to equities and bonds. • Commodity futures provide a diversification against systematic risk. • Commodity returns outperform “matching equities” three to one.

Goldman Sachs Initiative • Goldman Sachs led in developing the idea. • Created a diversified index in 1991 • Introduced idea of “roll” and “spot” returns • Did not go far until 2003 and 2004 • At the end of 2004, perhaps $40 billion invested, 90 percent from pension funds.

Many Funds follow the Goldman Sachs Commodity Index Formula. *Percent of total allocation to commodities. Source: PKVerleger LLC.

Required Futures Contract Purchases to Match a $50 BillionInvestment Increase in Collateralized Futures*

Stock, Bond, and Individual Commodity Future Performance over the Business Cycle – July 1959 to March 2004 (Average Monthly Annualized Returns, Percent)

Open Interest in All Petroleum Futures Source: NYMEX.

OPEC and Oil Industry Offer Investors a One-Way Option through their Inventory Policy. • One-way option: a guarantee to investors that they will not lose money • Term originated in currency markets during fixed-exchange regimes. • Investors short currency of country with serious international imbalance. • Country can either raise interest rates or lower exchange rates. • Investors do not lose if interest rates raised but do profit with lower exchange rates. • OPEC creates the one-way option by managing inventories.

OPEC Policy to Keep Inventories Low • Policy originated in March 1999. • Goal is to keep stocks low and markets in backwardation. • Companies have supported the effort by cutting stocks. • Result is backwardation.

Theoretical Supply of Storage — Relationship between Inventories and Price Spreads Source: Jeffrey C. Williams, The Economic Function of FuturesMarkets (Cambridge, England:Cambridge University Press, 1986.)

Mid-continent U.S. Inventories vs. Cash/Futures Price Spread, 1990 to 2004 Source: PKVerleger LLC.

Oil Industry Assists OPEC by not Selling Production Forward. • Producers increasingly prefer options to swaps or futures. • Some purchase puts. • Other firms enter collar arrangements. • The trend to options reduces the supply of oil offered to investors. • The cut in supply at a time of increased demand results in higher prices.

The Impact of OPEC’s One-Way Option • OPEC keeps inventories low – causing backwardation. • Cash flows into commodities – lifting forward prices. • Low inventories cause cash prices to rise relative to forward prices. • More cash flows in, causing prices to rise. • In theory, the cycle is never ending. • The result is a bubble.

Bubbles Can Last a Long Time. • Greenspan warning of “irrational exuberance” was made in December 1996. • Market collapse did not come until March 2000. • Some bubbles deflate slowly – or are superseded by later events. • A market disruption could prolong the oil bubble and lead to a super spike.

Governments Can Intervene to Break Bubbles. • The Federal Reserve Board broke the silver bubble in 1980. • Governments may be forced to break the current energy bubble if prices rise to excessive levels. However, tools are limited. • Swaps of strategic reserves • Recession induced by higher interest rates • Imposition of regulation on hedge funds • Central banks will act if oil prices are seen to boost inflationary expectations.

Saudi Arabia could also break the bubble. • Key officals worry that current high prices will destroy too much future demand. • Saudi Arabia has ended the one-way option. • Saudis have tools to break bubble. • Enter swaps with U.S. Strategic Reserves • Increase production • Remove destination limits on Saudi oil • Enter financial swaps to offer funds what they want

The Key Question is Will the Intervention be Smooth. • Almost any type of market intervention carries the risk of causing a collapse. • Buyers from pension funds will withdraw. Hedge funds may short the market. • Other producers may rush to sell. • Firms that have written puts to producers would have to sell to remain delta neutral. • The copper collapse carries a hint of things to come.

Spot Copper Price, January to December 1996 Source: Norman’s Historical Data.

NASDAQ 1000 Closing vs. Two-Year-Forward Price for WTI WTI NASDAQ Note: WTI price shifted back 66 months. Source: NASDAQ; NYMEX; PKVerleger LLC.