Download

1 / 32

340 likes | 612 Views

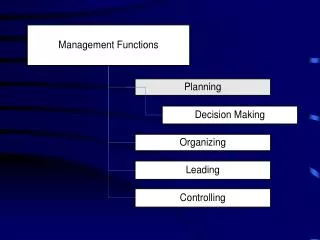

Producer decision Making. City University 200 7. Producer Decision Making. The firm. Production Function Q = F(L,K, N). Economic and Accounting Costs. Costs vs. expenditures Opportunity cost Explicit and implicit cost Accounting cost vs. economic cost Sunk cost Depreciation

E N D

Producer decision Making City University 2007

Producer Decision Making The firm Production Function Q = F(L,K, N)

Economic and Accounting Costs • Costs vs. expenditures • Opportunity cost • Explicit and implicit cost • Accounting cost vs. economic cost • Sunk cost • Depreciation • Accounting profit = TR –accounting cost • Economic profit = TR –economic cost

Analysis of the Production Function in the Short Runtechnological choice • Technology – a way of putting resources together • Efficient technology

Technological choice and consumer choice Consumer choice MUa/Pa = MUb/Pb The firm as a consumer: MUL/PL = MUK/Pk Technological choice MPL/PL = MPK/Pk

Analysis of the production functionshort run short run • There is at least one fixed factor • Firm’s decisions are constrained by the fixed factor • Is the demand changes, the firm can respond only by changing the quantity of output, not the scale of production

short runThe Law of Diminishing Returnstotal, average and marginal product

short runThe Law of Diminishing Returnstotal, average and marginal product

Analysis of the Production Functionlong run Long run • All factors are variable • The firm can change its production capacity – the scale of production

Short-Run vs.Long-Run Costs • Short run – Diminishing marginal returns results from adding successive quantities of variable factors to a fixed factor • Long run – Increases in capacity can lead to increasing, decreasing or constant returns to scale

Returns to Scale Rs = % change in the output : % change in production factors • Economies of Scale Rs > 1 • Constant Returns to Scale Rs = 1 • Diseconomies of Scale Rs < 1

Short-Run Costs Short-Run Costs Short run – there is at least one fixed factor Fixed cost – does not vary with the output Variable cost – directlyrelated to variations in output The Law of diminishing marginal returns

Short-Run Costs • Total Cost -the sum of all costs incurred in production • TC = FC + VC • Average Cost – the cost per unit of output • AC = TC/Output • Marginal Cost – the cost of one more or one fewer units of production • MC= TCn – TCn-1 units

Short Run CostsMarginal Costs Marginal costs МС –Extra cost involved in the production of an extra unit of output

The Revenues of the Firm • Total Revenue TR = P x Q • Average Revenue AR = P • Marginal Revenue MR = Δ TR/Δ Q

Short Run Maximum Profit MC = MR P > AC Minimum Loss MC = MR P > AVC Long Run Maximum Profit MC = MR P > AC The Profit of the Firm

The Theory of the Firm City University 2007

Theories of the Firm Neoclassical theory – profit maximization Assumptions: • Single-minded purpose • Rationality • Operational rules: MC = MR

Transaction Costs Transaction costs – “the costs of providing for some good or service through the market rather than having it provided from within the firm” – Ronald Coase • Search and information costs • Bargaining and decision costs • Policing and enforcement costs

Transaction costs • Three dimensions along which transactions may vary: • asset specificity • uncertainty • frequency

The three main characteristics of the firm • Collectivity of people in an organization • Action by superior-subordinate direction • Continuity over time

The firm’s benefits specialization in teams transaction-cost savings corporate capital formation morale The firm’s costs shirking agent misdirection rent seeking Firms vs. Markets

The Problem of X-inefficiency X-inefficiency - the difference between efficient behaviour of firms assumed or implied by economic theory and their observed behaviour in practice. - the cost that is higher than it needs to be because the firm is operating inefficiently

Internal Factors Poor contracts between principals and agents Large firms may be difficult to control External Factors Diffuse share ownership Limited threat of takeover Degree of competition Barriers to entry Factors causing X-inefficiency

The Principal – Agent Problem • the principal-agent problem - the difficulties that arise under conditions of incomplete and asymmetric information when a principal hires an agent • the agent’s actions affect the principal's payoff, but they are not directly observable by the principal, or they are not verifiable to outsiders. • The central dilemma - how to get the employee or contractor (agent) to act in the best interests of the principal (the employer) when the employee or contractor has an informational advantage over the principal and has different interests from the principal.

Theories of the Firm • Theory of Managerial Utility – Oliver Williamson • Sales Revenue Maximization Model – William Baumol • Maximizing Present Value of the Firm’s Future Stream of Sales Revenues – William Baumol

Theories of the Firm Maximizing Growth – Robin Marris • - the managerial utility depends on the firm’s rate of growth • Supply led growth vs. Demand led growth, or • profitability vs. diversification • The principal-agent problem

The Theory of the Firm The Integrative Model – Oliver Williamson • Integrates the growth maximization model and the profit/sales maximization models and the maximization of the present value of future sales • Max growth = max sales

Theories of the Firm Behavioral theories - Herbert Simon, Richard Cyert and James March • Firms – multi-goal, multi-decision, organizational coalitions • Imperfect knowledge and bounded rationality • Managers cannot meet the aspiration levels of all stakeholders • Managers cannot maximize, instead they have to satisfice

Stakeholders in the Firm • Owners/investors • Employees • Customers • Suppliers • Distributors • Creditors/banks • The government • Public at large